API security is crucial for protecting sensitive data, especially in credit card integration within open banking platforms. As financial services increasingly rely on open banking API security and REST API security, safeguarding transactions and customer information becomes a top priority. This blog explores essential API security best practices and effective API security solutions to ensure safe and seamless credit card payment integration.

We’ll also dive into key authentication methods like OAuth 2.0, two-factor authentication, and multi factor authentication to strengthen security in the evolving open banking ecosystem.

What’s next? Keep scrolling to find out:

🚀 API Security in Credit Card Integration: What API security means and why it matters in open banking ecosystems.

🚀 End-to-End API Security Implementation: Step-by-step process for securing credit card APIs in open banking platforms.

🚀 API Protection & Emerging Threats: Importance of API protection and common security threats in financial integrations.

🚀 Traditional vs Open Banking Security: A clear comparison between standard API security and open banking API practices.

🚀 Encryption, Tokenization & Compliance: How encryption, tokenization, and regulatory compliance strengthen API security.

What is API security in credit card integration?

API security in credit card integration involves protecting APIs used for credit card payment integration within open banking platforms. As open banking continues to grow, securing the connection between financial institutions and third-party providers is crucial to prevent unauthorized access and data breaches.

- Understanding API Security Risks: Credit card API integration faces risks like injection attacks, data leaks, and weak authentication. Addressing these API security risks early helps protect sensitive financial information in open banking.

- The Role of API Security Testing: Regular API security testing strengthens REST API security by identifying vulnerabilities in credit card processing integration and ensuring APIs comply with security standards.

- Implementing API Gateway Security: API gateway security acts as a control point for open banking integration, managing access, enforcing policies, and monitoring API traffic to boost open banking API security.

- Importance of Authentication Methods: Using strong authentication methods such as two-factor authentication, multi-factor authentication, and passwordless authentication is critical to secure API access and prevent unauthorized usage.

- Using OAuth 2.0 for Secure Access: OAuth 2.0 authentication, including client credentials and authorization code flows, provides secure and controlled access to credit card APIs within open banking platforms.

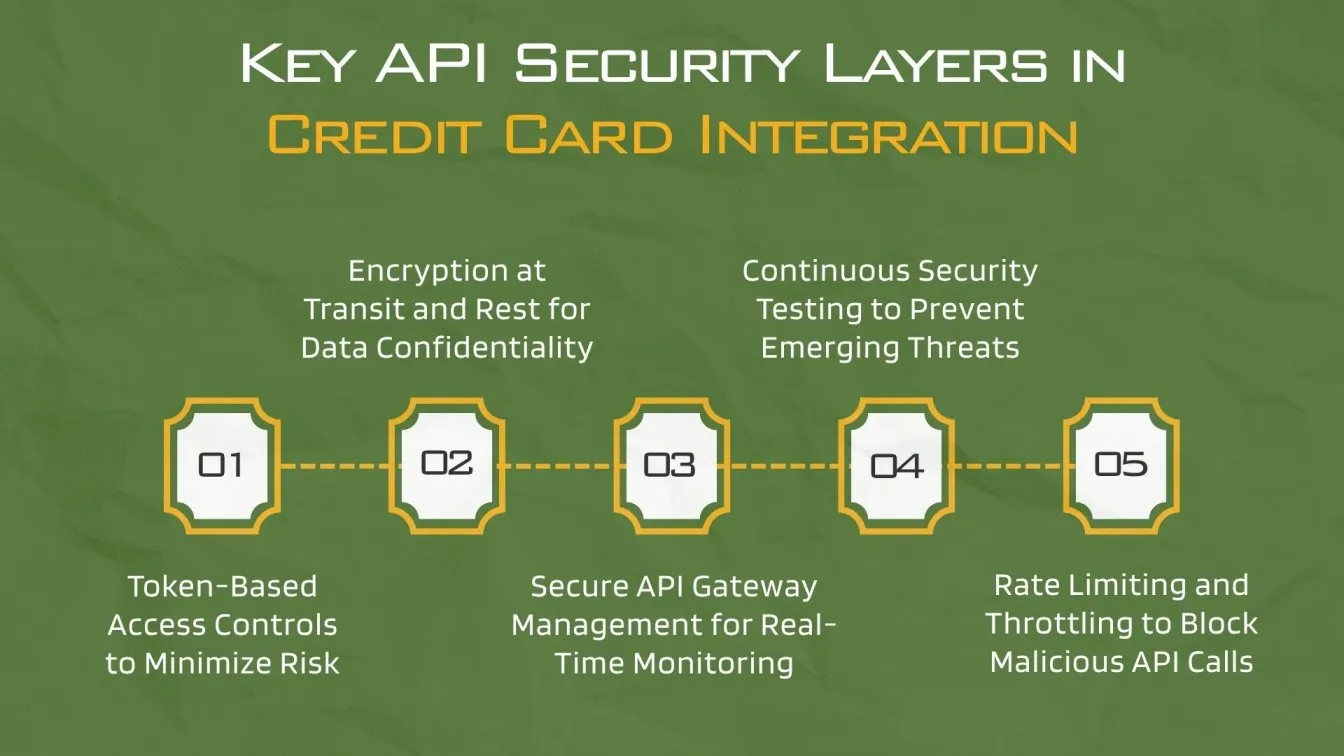

Steps to Implement End-to-End API Security in Credit Card Integration for Open Banking

Implementing end-to-end API security in credit card integration for open banking is critical to protect financial data, prevent fraud, and ensure compliance. As open banking platforms grow, securing every layer of API interaction becomes vital to safeguard customer trust and sensitive payment data. Below are essential steps to achieve comprehensive API security across credit card APIs within open banking solutions:

- Secure with OAuth 2.0 authorization flows: Use the OAuth 2.0 authorization code flow and OAuth 2.0 client credentials flow to authorize API access securely, especially in multi-party payment systems.

- Protect endpoints using API gateway security tools: Implement API security tools at the gateway level to monitor traffic, rate-limit requests, and prevent abuse in real time during credit card API integration.

- Enable multi-factor authentication (MFA): Strengthen user access controls by requiring MFA authentication, including 2FA authentication and passwordless authentication methods.

- Perform continuous API security testing: Conduct automated and manual API security testing to identify vulnerabilities such as injection flaws or broken authentication flows in open banking APIs.

- Monitor token usage and expiration: Track OAuth 2.0 token lifecycle and enforce strict controls on OAuth 2.0 access token expiration and renewal to prevent unauthorized reuse.

Why API protection is important for open banking platforms?

As open banking platforms reshape the financial services industry, protecting APIs becomes a non-negotiable part of securing sensitive data and maintaining trust. Since APIs act as gateways between banking institutions and third-party applications, a lack of security can expose vulnerabilities that lead to reputational damage, data loss, and regulatory penalties. Strong API protection ensures safe integration of financial solutions while enabling secure data sharing across a broader range of digital experiences.

- Safeguards financial transactions: Ensures that bank cards, savings accounts, and other financial accounts are shielded from malicious activity.

- Enhances user experience: By preventing security breaches, platforms can deliver seamless and secure banking services to individual customers.

- Protects third-party applications: As third-party developers and fintech startups build innovative services, API security maintains the integrity of these digital offerings.

- Meets regulatory requirements: Aligns with evolving banking regulations and legal frameworks to ensure compliance checks are passed.

- Supports operational efficiency: Prevents system disruptions that could hinder real-time data flow, real-time insights, or real-time access to bank services.

- Strengthens the security posture: Through regular security audits and penetration testing, platforms reinforce their ability to handle complex financial tools and maintain a healthy financial ecosystem.

Common threats in credit card API integrations

Credit card API integration plays a pivotal role in enabling seamless digital banking and real-time payments. However, these APIs are also frequent targets for cyberattacks due to the sensitive nature of financial transactions and user data. Understanding the common threats is essential for financial service providers aiming to build secure, efficient, and compliant credit card payment integration systems across the banking sector.

- Token theft and misuse: Attackers may exploit poorly secured OAuth 2.0 tokens to gain unauthorized access to bank accounts and financial tools.

- Man-in-the-middle (MITM) attacks: Intercepted communication between third-party service providers and banking platforms can expose personal and financial data.

- Improper authentication methods: Weak or outdated authentication systems lacking multi-factor authentication (MFA) increase the risk of unauthorized access to mobile banking apps and credit card APIs.

- Injection attacks: APIs without input validation may allow attackers to inject malicious code, compromising banking infrastructure and digital experiences.

- Broken authorization controls: Flawed access rules can give attackers elevated permissions, impacting financial applications and secure data sharing.

- Insufficient API security testing: Lack of thorough testing makes it difficult to identify vulnerabilities, leading to compliance failures and poor protection of financial health.

- Excessive data exposure: APIs that expose too much real-time data create opportunities for misuse, especially in high-risk financial services sectors.

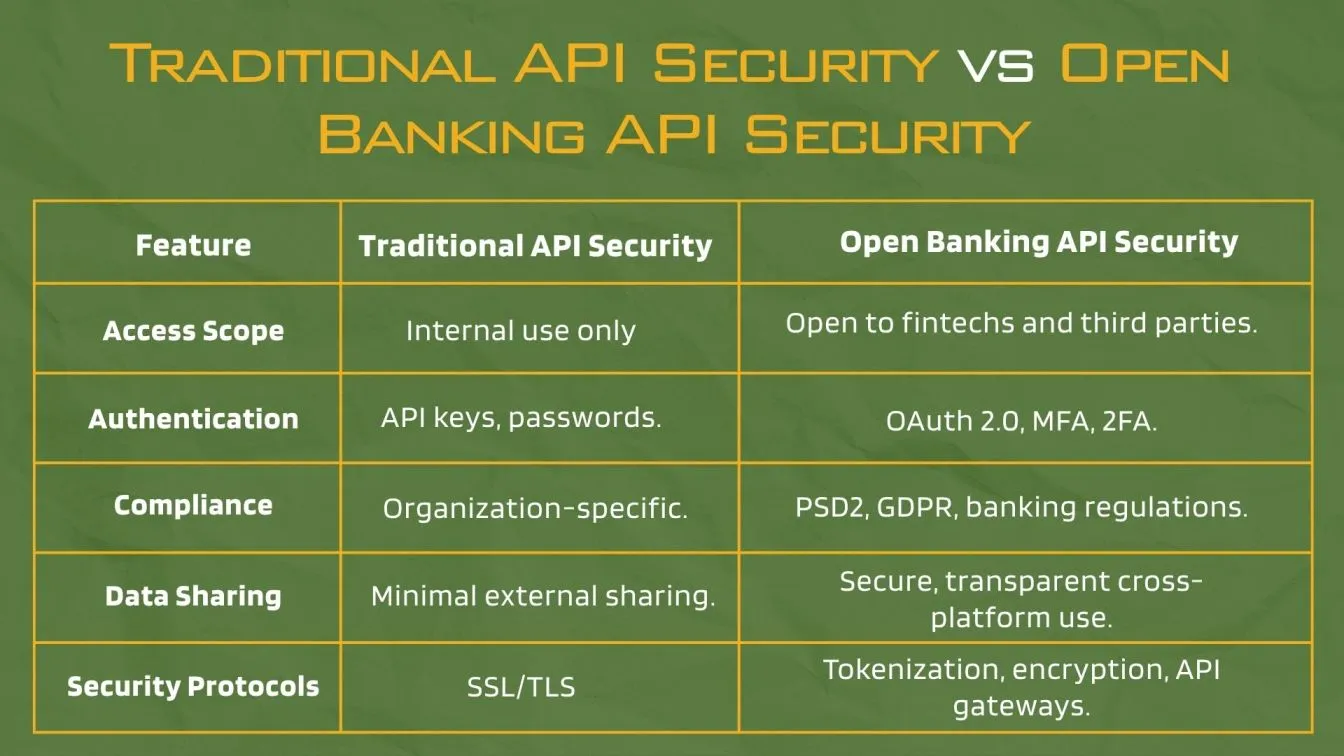

Difference between traditional API security and open banking API security

Traditional API security mainly focuses on protecting internal systems with limited external access, while open banking API security ensures secure and regulated data sharing across a diverse financial ecosystem. This shift introduces new challenges and security protocols essential for safeguarding credit card integration and enhancing user experience within open banking platforms.

Role of encryption and tokenization in credit card API security

Encryption and tokenization are core data protection strategies that play a crucial role in secure credit card API integration within open banking platforms. Encryption involves converting sensitive information into unreadable code, ensuring confidentiality during transmission. Tokenization replaces real card data with randomly generated tokens, minimizing the risk of exposing actual credit card details.

- Data Protection:

Encryption converts sensitive credit card data into unreadable code during transmission, preventing data breaches in the financial sector and enhancing the security posture of banking institutions. - Tokenization:

Tokenization replaces actual credit card details with unique tokens, reducing the exposure of real data during credit card payment integration and banking transactions. - Compliance:

Both encryption and tokenization help meet regulatory requirements such as PSD2 and banking regulations, supporting a proactive approach to security policies within the financial services landscape. - API Gateway Security:

Encryption safeguards data at the API gateway level, ensuring secure data sharing between third-party service providers, fintech companies, and traditional banks in the banking industry. - User Trust:

These methods improve customer experiences and build customer trust by maintaining privacy and reducing fraud risks, enhancing digital banking and financial management platform security. - Operational Efficiency:

Secure data handling reduces reputational damage and operational disruptions caused by security breaches, while supporting real-time monitoring and compliance checks for a wide range of financial products and services.

Regulatory compliance for secure credit card APIs in open banking

Regulatory compliance is essential for secure credit card APIs within open banking platforms. Adhering to industry standards and legal frameworks ensures that financial service providers protect sensitive data while fostering a collaborative ecosystem between banks, fintech companies, and third-party developers. This compliance builds trust and promotes innovative solutions in the evolving financial landscape.

- Adherence to Industry Standards: Open banking integration must follow regulatory requirements like PSD2 and GDPR to secure credit card processing integration and protect bank statements and customer data.

- Strong Customer Authentication: Protocols such as OAuth 2.0 and OpenID Connect support multi-factor authentication, addressing security concerns and enhancing API security best practices.

- Continuous Monitoring: Regular security audits and real-time monitoring help identify API security risks, supporting a proactive approach to secure credit card API integration.

- Financial Inclusion: Regulatory compliance promotes access to a wider range of services for underserved populations, supporting financial inclusion and enabling informed decisions.

- Ledger Technology: Emerging technologies like distributed ledger technology improve transparency and accountability in open banking payments and credit card API integration.

- Secure Data Sharing: Clear security policies ensure confidential and safe exchange of financial data, maintaining customer trust and supporting a secure open banking platform.

Final Thoughts

Securing credit card APIs in open banking ecosystems is vital for protecting sensitive financial data and ensuring seamless, trustworthy digital banking experiences. By adopting robust API security solutions, strong authentication methods, and complying with regulatory standards, financial institutions and fintech companies can drive innovation while safeguarding customer trust. Staying proactive with security tools and best practices empowers the future of open banking, delivering safe, efficient, and customer-centric financial services.

Frugal Testing stands out among top software testing companies in USA, offering QA testing services for enterprises and functional testing solutions tailored for open banking platforms. With expertise in bug testing services, RPA testing services, and AI-driven test automation services, Frugaltesting.com helps secure API ecosystems. Their cloud-based test automation services and manual software testing companies’ experience ensure robust protection for credit card APIs in a fast-evolving financial landscape.

People Also Ask

What is the difference between API and API integration?

An API defines how systems communicate, while API integration connects and automates interactions between those systems for seamless data flow.

Does Monzo offer secure credit card integration via API?

Monzo offers secure APIs, mainly for current accounts, but it does not directly support third-party credit card integration through APIs.

Does Revolut support credit card integration through open banking APIs?

Revolut supports open banking APIs for account access but offers limited support for external credit card integration features.

What is the Open Finance API, and how does it affect credit card integration?

Open Finance APIs expand on open banking by offering broader data access, enabling deeper credit card integration, and financial personalization.

What kind of APIs do banks use for credit card processing?

Banks typically use REST APIs secured with OAuth 2.0 for handling credit card transactions, authentication, and fraud prevention workflows.