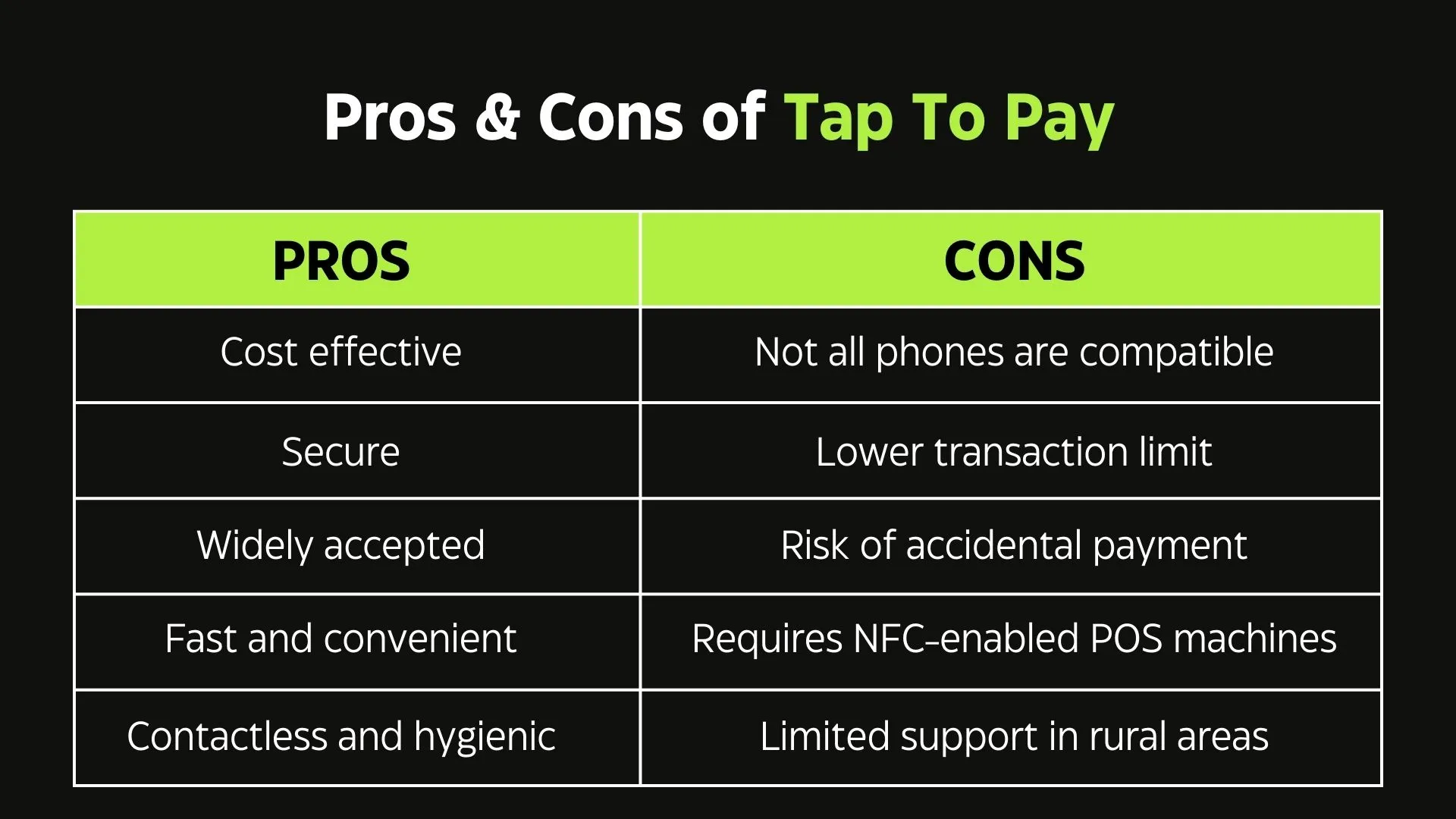

Tap and Pay, powered by NFC contactless technology, is reshaping how users interact with mobile payments. Despite its speed and convenience, adoption still faces technical, regulatory, and user-trust hurdles, especially across diverse devices, regions, and user segments. From biometric authentication to PCI DSS compliance, this blog explores how to secure and scale contactless payment systems for Android, iPhone, and digital wallet users.

💡 Here’s what you’ll learn

📌 How tap and pay works across Android, iPhone, and NFC-enabled devices.

📌 Major security risks like skimming, payment fraud, and token misuse.

📌 Key regulatory compliance needs: KYC, AML, and PCI DSS.

📌 How biometric authentication and tokenization boost mobile payments security.

📌 Core adoption barriers across regions, devices, and user behaviors.

How Tap and Pay Technology Works: Understanding Mobile Contactless Payments

Tap and Pay is a mobile payment technology that enables users to make contactless transactions using smartphones, smartwatches, or tap-enabled cards. This system relies on NFC (Near Field Communication), allowing communication between a payment terminal and a user’s device within a short range.

When users tap their Android Tap and Pay or Tap and Pay Iphone devices on a compatible terminal, encrypted payment data is exchanged, allowing secure processing. Samsung Pay, Apple Pay, and Google Tap and Pay are well-known Tap and Pay applications. Businesses using platforms like Square Mobile Payments also accept NFC contactless payments, helping improve transaction speed and customer convenience.

Tap and Pay also integrates seamlessly with digital wallets, enabling users to store multiple cards and credentials for swift use. The process is quick, intuitive, and increasingly supported across global retailers.

Key Adoption Challenges in Tap and Pay Across Devices, Users, and Regions

While phone tap and pay are transforming how we approach transactions, their widespread adoption is limited by technical and infrastructural challenges, primarily compatibility issues between POS terminals and user devices. These issues hinder the seamless use of NFC contactless payments across diverse environments, especially for small businesses or users in semi-urban and rural areas.

While mobile wallets like Google Pay and Apple Pay Later are driving innovation, many mobile devices still lack consistent support for contactless payment technology. In regions with limited POS access, QR codes often serve as a practical backup option with security encryption ensuring safe transactions.

Challenges in Tap and Pay across devices, Users and Regions:

- Device Compatibility: Not all Android or iOS devices support NFC Tap and Pay. Older models may lack the necessary hardware.

- POS Terminal Readiness: Many regions still lack NFC-enabled point-of-sale terminals, especially in rural or underdeveloped areas.

- User Awareness: Many users are unaware of how to use Tap and Pay or hesitate due to security misconceptions.

- Platform Fragmentation: Variability in Tap and Pay apps, operating systems, and interfaces can confuse users, slowing widespread adoption.

- Financial Inclusion Gaps: People without access to bank accounts or modern smartphones may be excluded from using Tap and Pay cards or mobile platforms.

These challenges are more pronounced in markets with limited digital infrastructure and varying levels of fintech software development services.

Major Security Concerns in Tap and Pay Transactions

As tap and pay adoption increases across mobile wallets, NFC contactless cards, and digital payment apps, so do concerns around transaction security. The absence of strong biometric authentication, inconsistent use of tokenization protocols, and vulnerability to NFC-based skimming attacks pose significant risks. These issues make tap and pay transactions attractive targets for fraudsters and raise questions about platform reliability.

Many users remain unaware of these threats, which undermines trust in contactless payment systems. Without robust payment fraud detection tools and standardized regulatory compliance practices, the tap and pay ecosystem may struggle to scale securely. Addressing these gaps is essential for fintech companies, payment providers, and banks to ensure safe, seamless, and widespread use of digital tap-to-pay solutions.

Fraud Risks, Skimming, and Contactless Exploits

With the rise in contactless card payments, concerns around online payment fraud and skimming are growing. Attackers may attempt to intercept NFC signals using malicious devices. Other threats include cloning cards or exploiting weak encryption protocols.

- NFC Skimming: Hackers can use rogue devices to steal tap-and-pay data wirelessly.

- Card Cloning: Weak encryption can lead to duplicate cards from stolen data.

- Unsecured POS Systems: Outdated or unprotected terminals are easy targets for attackers.

- Unencrypted Transactions: Lack of proper encryption exposes card details during payment.

- Low User Awareness: Many users don’t know the risks or how to secure their devices.

- Device Security Gaps: Older phones or apps with weak settings increase fraud risks.

Authentication Gaps and Biometric Limitations

Many Tap and Pay apps rely on biometric authentication technology, such as fingerprint or facial recognition. However, if not enforced by default or bypassed through exploits, the system becomes vulnerable. Some older Android Tap and Pay devices may lack robust biometric hardware, leaving authentication gaps.

- Optional Biometric Use: Some tap and pay apps don’t enforce biometrics by default, weakening security.

- Bypass Risks: Exploits in older devices or outdated apps may allow bypassing biometric checks.

- Inconsistent Implementation: Varying biometric standards across devices affect reliability.

- Hardware Limitations: Older smartphones may lack secure fingerprint or facial recognition modules.

- User Negligence: Some users disable biometric prompts, increasing fraud risks.

Regulatory and Compliance Requirements for Tap and Pay Systems

As tap and pay technologies evolve, so do the regulatory and compliance obligations surrounding them. For fintech companies and digital wallet providers, meeting standards related to KYC (Know Your Customer), AML (Anti-Money Laundering), and PCI DSS (Payment Card Industry Data Security Standard) is essential for ensuring trust, preventing fraud, and maintaining operational legitimacy.

The challenge lies in implementing these frameworks in a dynamic, contactless ecosystem where transactions are fast, digital, and often cross-border. Moreover, the use of tokenization, biometric authentication, and cloud-based infrastructure adds complexity to regulatory compliance management.

KYC and AML Regulations in Mobile Payments

Know Your Customer (KYC) and Anti-Money Laundering (AML) practices are essential to prevent financial misuse. Users onboarding with Tap and Pay Android apps or digital wallets must undergo identity verification, especially when linking credit or debit cards.

- Mandatory Identity Checks: Tap and Pay users must complete KYC to verify identity.

- Fraud Prevention: KYC and AML reduce the risk of financial fraud and misuse.

- Linked Accounts: KYC is required when linking cards or bank accounts to digital wallets.

- Regulatory Compliance: Fintech apps must align with RBI and global AML standards.

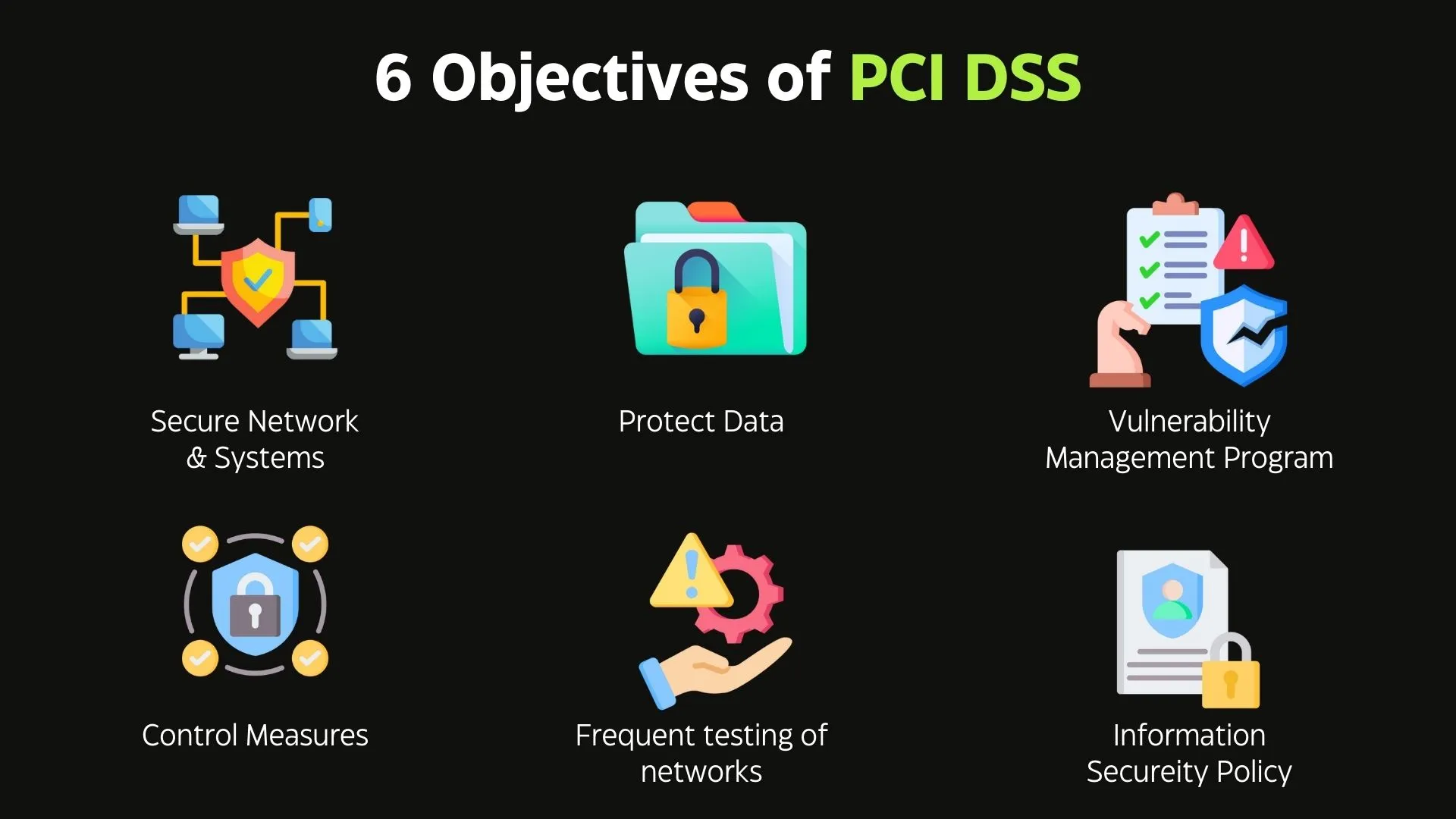

PCI DSS Compliance for Contactless Transactions

All Tap and Pay systems must adhere to PCI DSS (Payment Card Industry Data Security Standard) to ensure secure storage and transmission of payment data. This includes encryption, access controls, and regular vulnerability testing.

- Data Encryption: Tap and Pay systems encrypt payment data to prevent breaches.

- Secure Transmission: PCI DSS ensures payment info is securely transmitted at every point.

- Access Controls: Only authorized systems and personnel can access payment data.

- Ongoing Audits: Regular vulnerability scans and audits are required for compliance.

- Tokenization Support: PCI DSS encourages tokenized payments to protect cardholder data.

Role of Local and Global Regulatory Bodies

From India’s RBI to the EU GDPR, various regulators mandate regulatory compliance services in mobile and fintech ecosystems. Adopting regulatory compliance software and maintaining regulatory compliance management practices is key to sustaining trust.

- Regulatory Oversight: Bodies like India’s RBI and the EU GDPR set compliance rules.

- Mandatory Compliance: Fintech and tap and pay platforms must follow local and global laws.

- Compliance Software: Adoption of regulatory compliance software ensures continuous monitoring.

- Trust Building: Meeting regulations boosts consumer confidence in mobile payments.

- Data Privacy: Regulators enforce strict data protection in fintech ecosystems.

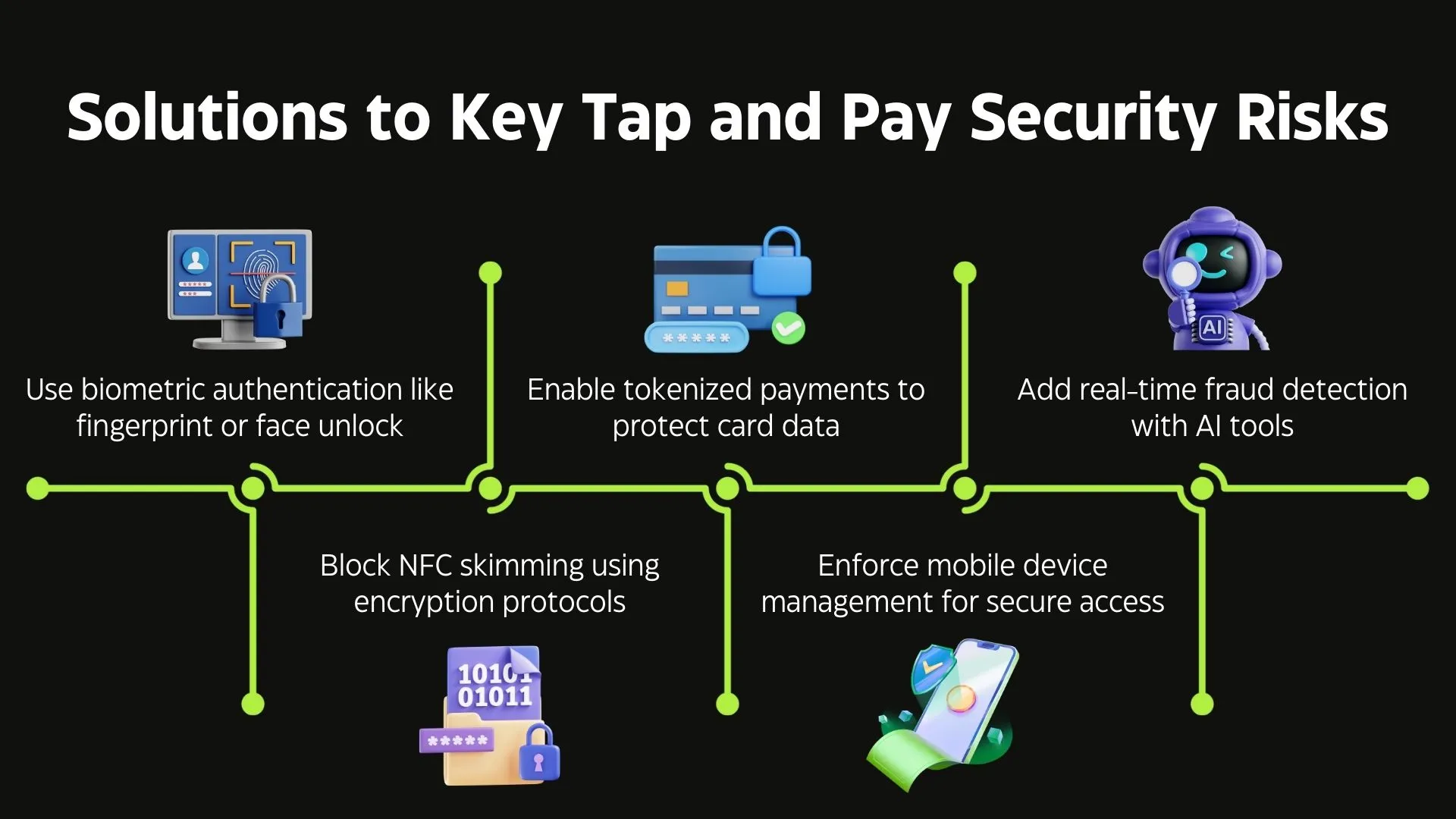

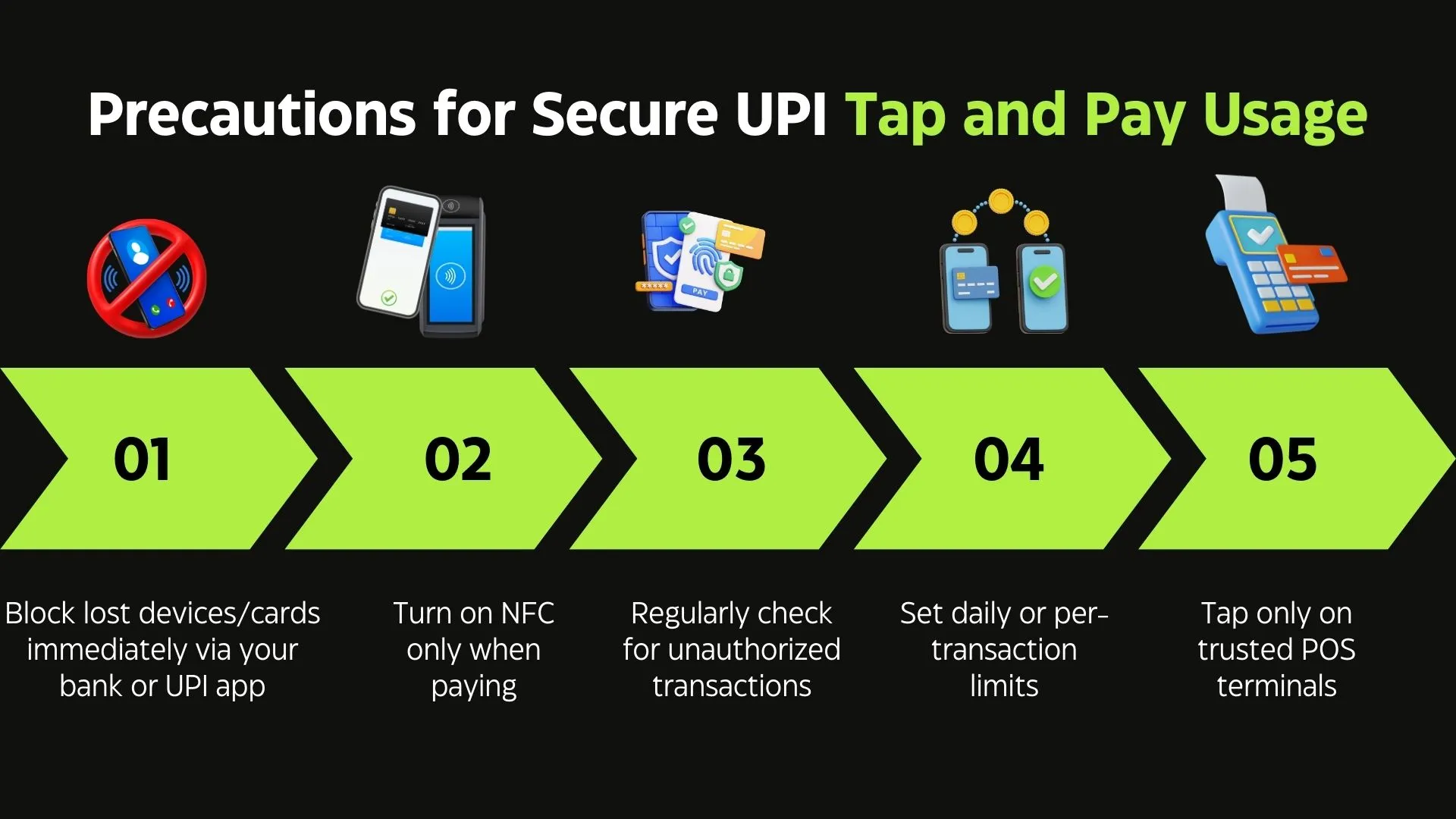

Best Practices to Improve Security and Drive Adoption of Tap and Pay

Implementing strong biometric authentication, payment tokenization, and real-time fraud detection is key to enhancing tap and pay security. Educating users and upgrading POS infrastructure further drive widespread adoption and trust in contactless payments. Boosting tap and pay adoption starts with securing multistep transactions using contactless digital technology and smart mobile device management. Insights from online data collection and platforms like Payments Dive help improve security and the overall customer experience.

Ways to Boost Tap and Pay Security:

- Biometric Authentication: Mandate fingerprint or facial recognition before authorizing any tap transaction.

- Payment Tokenization: Use dynamic tokenization of data to replace sensitive card information with temporary tokens, making credit card tokenization more secure.

- AI-Powered Fraud Detection: Leverage payment fraud detection systems using AI to analyze behavior patterns and block anomalies.

- Transaction Limits and Alerts: Allow users to set low transaction caps and receive instant alerts, mitigating unauthorized usage.

- User Education Campaigns: Educate users on how to use Tap and Pay securely and the benefits of contactless payments to increase trust.

These practices improve consumer confidence, reduce risk, and enhance user experience in fintech software development landscapes.

Conclusion: Overcoming Adoption Barriers to Build a Secure and Trusted Tap and Pay Ecosystem

To mainstream Tap and Pay, stakeholders must focus on digital transformation, mobile apps, and consumer perception. Expanding support for contactless-enabled cards, EMV cards, and smart cards across contactless POS machines and POS payments technology is crucial, especially in smart cities and transportation services.

Upgrading payment platform infrastructure and improving POS integration will boost mobile payment acceptance and enhance customer service. Payment tokenization, biometric authentication, and voice-activated payments powered by artificial intelligence and data analysis can help reduce fraud and support secure digital payment processing software.

Building trust also requires a proactive security team, regular security audits, a clear security statement, and strong chargeback management. Fintechs must align payment rails with user behavior, considering the social context and preferences of digital natives. With the right approach, Tap and Pay can become a secure, inclusive, and widely accepted mode of POS and mobile payments.

People Also Ask

👉 How does tap and pay technology support offline transactions without internet?

Tap and pay uses NFC to exchange encrypted data with POS terminals offline. Transactions are authorized later when online, enabling smooth payments without an immediate internet connection.

👉 What role do banks and payment gateways play in securing tap and pay systems?

Banks and gateways secure transactions with fraud detection, tokenization, and biometric authentication, and ensure PCI DSS compliance to prevent payment fraud.

👉 Can tap and pay work on wearable devices and how secure are they?

Yes, many wearable devices like smartwatches support tap and pay via NFC. These devices use the same security layers as smartphones, including biometric locks, tokenization, and encrypted data transmission, making wearable payments both convenient and secure.

👉 How do cultural and demographic factors influence the adoption of tap and pay?

Adoption depends on smartphone access, digital trust, and awareness. Younger, tech-savvy users adopt faster, while others may face security fears or lack education.

👉 What emerging technologies are improving the security of contactless payments?

AI fraud detection, biometric enhancements, dynamic tokenization, and blockchain technology are strengthening tap and pay security.