Credit card rewards, whether from a travel rewards card, a cash-back card, or the best hotel rewards card, have become essential for attracting users of a credit card with rewards. Behind the allure of Membership Rewards and loyalty perks lies a strategic model built by credit card issuers and processing companies. Through interchange fees and partnerships with high-value transfer partners, issuers fund generous programs while maintaining profitability. As shown in any Card Report, these rewards also help issuers report credit card income more favorably, despite the rising cost of funds. Discover how the best credit card rewards are structured to benefit both cardholders and issuers.

What’s Next? Keep reading to discover:

🚀 How credit card issuers use interchange fees to fund rewards programs.

🚀 Strategies behind the best credit card rewards and loyalty reward programs.

🚀 Who pays for those generous credit card rewards you enjoy?

🚀 Risks credit card companies face with reward programs for customers and how they manage them.

🚀 The future of credit card rewards and how issuers continue to benefit.

What Are Credit Card Rewards and How Do They Work?

Credit card rewards are benefits offered by credit card issuers to motivate cardholders to use their credit cards more frequently. These customer reward programs enable users to earn value, whether in cash, points, or travel perks, for every eligible transaction they make. These programs are a core offering of credit card companies and are a significant part of the strategy used by major credit card issuers to increase engagement, spending, and retention.

How Do Credit Card Rewards Work?

- Transaction Initiation

When a cardholder makes a purchase, the credit card issuer processes it through major credit card companies. - Processing & Interchange Fees

The issuer sends payment to the merchant, deducting interchange fees for credit cards, also known as card interchange fees or bank interchange fees. These fees reduce the amount merchants receive. - Reward Allocation

A part of the credit card interchange fees funds customer reward programs like cashback, points, or miles. These are key features of credit card reward programs and customer loyalty reward programs. - Ongoing Engagement

These rewards encourage more spending, supporting loyalty and repeat use while helping issuers earn through interchange fees from credit card systems.

Step-by-Step Breakdown:

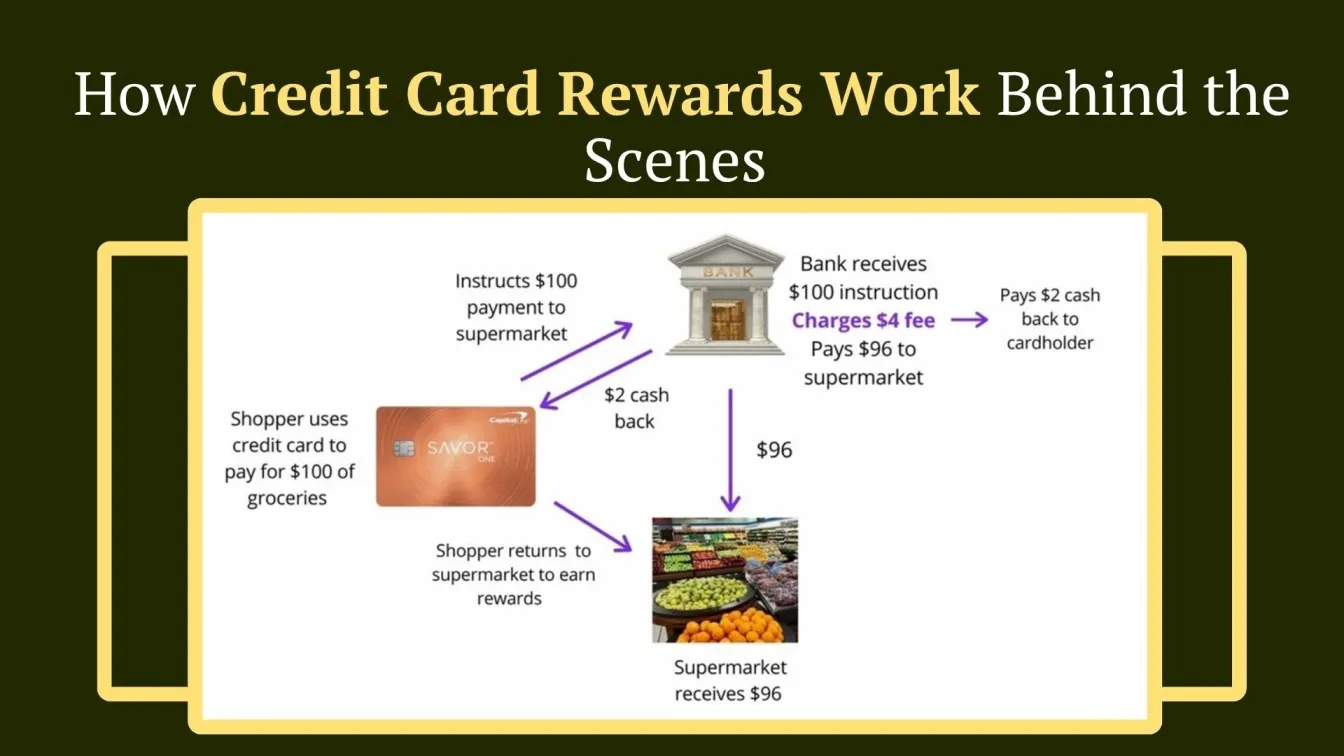

- Cardholder makes a purchase: A shopper uses a rewards credit card to pay $100 at a supermarket.

- Bank receives the payment request: The shopper’s credit card issuer processes the payment and instructs their bank to send $100 to the supermarket.

- Interchange fees are applied: The bank charges a $4 interchange fee (also called merchant interchange fees) and transfers only $96 to the merchant.

- Cardholder receives rewards: From that fee, the bank pays $2 as cashback to the customer, fulfilling the promise of the credit card rewards program.

- Merchant gains repeat business: The shopper is incentivized to return to the supermarket to earn more rewards, increasing customer loyalty.

Why Rewards Encourage People to Spend More

Reward programs aren't just designed to thank customers, they're structured to influence habits. Here's why they drive increased spending:

- Perceived Value from Everyday Spending: Many best credit card reward programs offer signup bonuses or tiered rewards after reaching certain spend thresholds, nudging users to increase purchases.

- Reward Milestones Drive Behavior: Many best credit card reward programs offer signup bonuses or tiered rewards after reaching certain spend thresholds, nudging users to increase purchases.

- Emotional Satisfaction: Users often chase specific rewards, such as a free hotel night or flight, pushing them to keep using their travel rewards credit card regularly.

- Goal-Based Redemption: Users often chase specific rewards, such as a free hotel night or flight, pushing them to keep using their travel rewards credit card regularly.

Example: A shopper uses their best rewards credit card for everyday purchases like coffee and fuel to quickly earn 5,000 points for a free hotel stay. This boosts their card spending, helping issuers earn more interchange fees while keeping the shopper loyal to the card.

Credit Card Rewards: User Benefits vs Issuer Profits:

How Do Credit Card Issuers Make Money from Rewards?

Credit card rewards programs may seem like consumer perks, but they’re also a smart revenue strategy for issuers, designed to attract users, boost retention, and drive consistent profit.

Key Ways Credit Card Issuers Earn from Rewards:

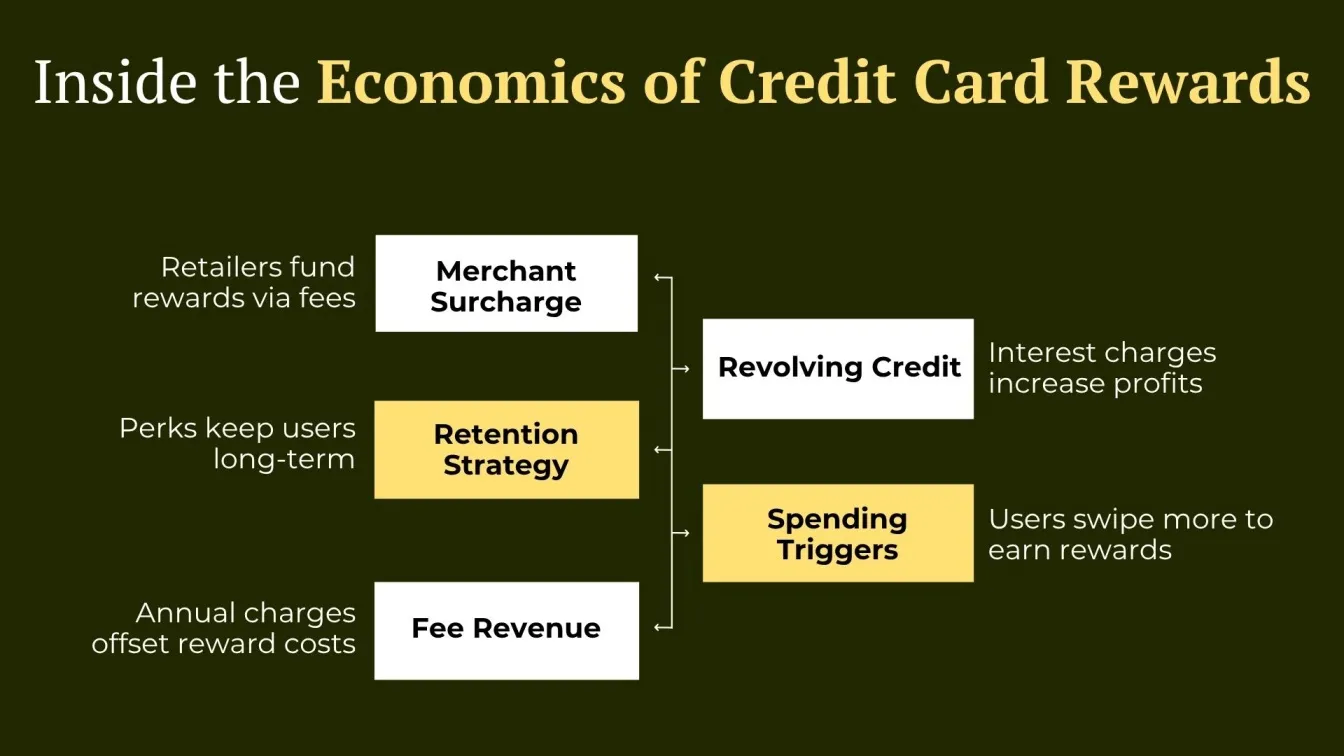

Although credit card rewards programs offer users cashback, miles, or points, they’re also a highly profitable strategy for credit card issuers. Here’s how the economics work behind the scenes:

1. Merchant Fees (Interchange Fees):

When a customer uses a rewards credit card, the merchant pays a transaction fee, known as the interchange fee, typically between 1.5% to 3% of the purchase value. This merchant interchange fee goes directly to the issuer. For instance, if a user spends ₹1,000 and the fee is 2%, the issuer earns ₹20.

2. Lower Reward Payout Than Revenue Earned:

Only a small part of the dollar of purchases, like ₹5 out of ₹20, is returned via rewards cards. The rest becomes profit for the merchant bank and issuer. This model supports a business credit card rewards model that reports strong credit card income.

3. Interest on Unpaid Balances:

When credit card holders use revolving credit or delay balance transfers, issuers earn high interest. This interest from a percentage of accounts is a major revenue source. It increases the impact on consumers who carry balances for a long period.

4. Annual and Renewal Fees:

Many bank credit cards charge annual or renewal fees to fund rewards. These fees add thousands of dollars to credit card operations. Programs like Bilt Rewards benefit from such consistent income streams.

5. Card Usage Due to Rewards:

Rewards encourage more credit card purchases at gas stations, retail banking partner stores, and major merchants. Higher usage means more interchange income and cash advance fees. This increase in credit card transactions boosts Credit Card Profitability.

6. Long-Term Loyalty and Retention:

Strong reward programs retain credit card holders over long periods. This boosts the share of accounts with ongoing activity and revenue. It also reflects in the analysis of market share and share by outstanding.

Who Pays for All Those Generous Credit-Card Rewards?

Though credit card rewards programs appear to be free perks, offering cashback, points, or miles, the actual cost isn’t covered by the issuers alone. Instead, it’s a cost shared across the ecosystem in ways most consumers don’t realize. Here’s how it plays out:

1. The Real Cost Begins with Merchants:

Every time a consumer uses a rewards credit card, the merchant pays a percentage of the transaction, known as an interchange fee, to the credit card processing companies.

Impact:

This fee typically ranges between 1.5% to 3% and is higher for premium cards such as travel rewards credit cards or best hotel rewards credit cards. These fees significantly affect merchant profits.

Result:

To recover losses, many merchants raise product prices, especially small businesses with lower margins. This makes all customers indirectly contribute to the cost of reward programs.

2. Everyone Pays- Even If They Don’t Use Rewards:

To absorb the impact of interchange fees, merchants often increase the price of goods and services for everyone, not just credit card users.

Impact:

This means even customers who pay with cash or debit cards end up covering part of the cost of credit card rewards, even though they receive no benefits themselves.

Result:

This system unintentionally penalizes non-reward users, particularly lower-income shoppers, by charging them higher prices to support perks for others.

3. Cardholders Pay in Fees and Interest:

Many best rewards credit cards charge annual or renewal fees, and if users don’t pay off their balances, they are charged interest, sometimes up to 42% APR.

Impact:

The total cost of interest and fees can often be greater than the value of the rewards earned, especially for users who carry forward balances. For cardholders, this makes it important to compare rewards against annual fees, interest rates, and regular spending habits before choosing a card. Personal finance resources such as JBayer Wealth can add useful context when weighing whether a rewards program truly fits a person’s broader financial goals.

Result:

This makes interest income and fee revenue a major profit center for credit card issuers, helping them support extensive loyalty reward programs.

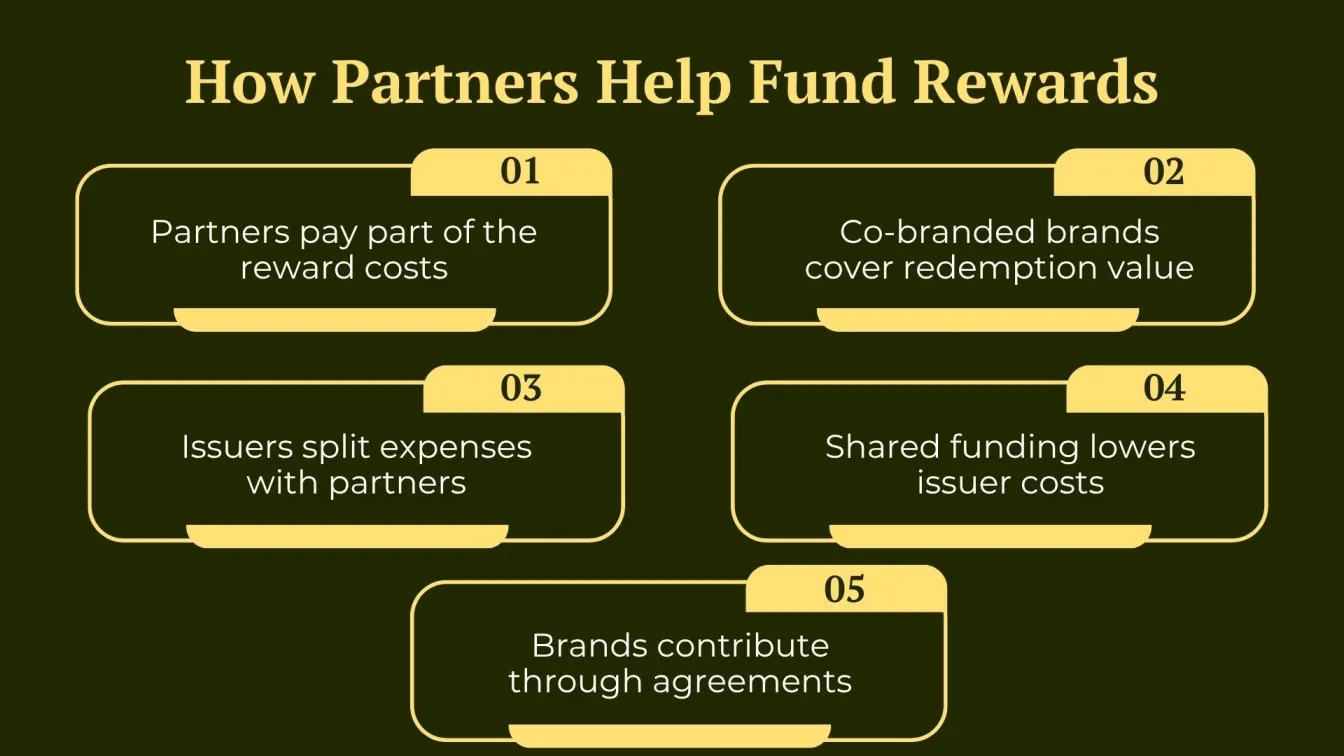

4. Issuers Don’t Pay Alone- Partners Help:

In co-branded partnerships (e.g., hotel chains or airlines), credit card issuers share the cost of reward programs with the brand partner.

Impact:

These brands co-fund the rewards in exchange for customer loyalty, consumer data, and brand exposure.

Result:

This cost-sharing strategy allows issuers to offer high-value rewards without absorbing all expenses, while partners benefit from deeper customer engagement.

5. Non-Rewards Users Often Bear Hidden Costs:

Research, including studies from the Kellogg School of Management, shows that non-reward cardholders, often lower-income users, end up indirectly supporting reward programs.

Impact:

They still pay the inflated prices resulting from merchant fees, even though they don’t earn cashback, points, or miles.

Result:

The system creates a regressive effect, where those who benefit least from rewards are often the ones funding them the most, raising concerns about fairness in the credit ecosystem.

What Strategies Make Credit Card Reward Programs Successful?

Every successful credit card rewards program is built on a strategy that balances profits, customer loyalty, and market edge. Top issuers design rewards to attract users, boost spending, and build lasting brand loyalty.

1. Tiered Reward Structures to Encourage More Spending

Tiered rewards cards offer more credit card rewards points for categories like various stations and retail partners. This increases credit card purchases and the share of purchases across a period. It supports Credit Card Profitability and efficient credit card operations.

2. Co-Branded Partnerships for Niche Loyalty

Co-branded cards with hotel or airline brands support frequent flyer programs and deepen loyalty. They boost the share by outstanding and increase credit card assets. Issuers like American Express benefit from these partnerships with major merchants.

3. Introductory Bonuses and Limited-Time Offers

Sign-up bonuses during a sample period drive thousands of dollars in credit card transactions. These offers grow the percentage of credit card accounts opened. Business Insider notes this as a key growth tactic in the retail card market.

4. Seamless Redemption Experience

Flexible redemption options like travel, cashback, or gift cards improve the function of credit cards. Easy use increases cardholder satisfaction and reduces churn. This is crucial for retaining the majority of credit card holders.

5. Gamification and Digital Integration

Gamified rewards apps like Bilt Rewards engage users with spending insights and alerts. This improves payment option usage and supports loan loss provisions. It adds value to the functions of credit cards in daily life.

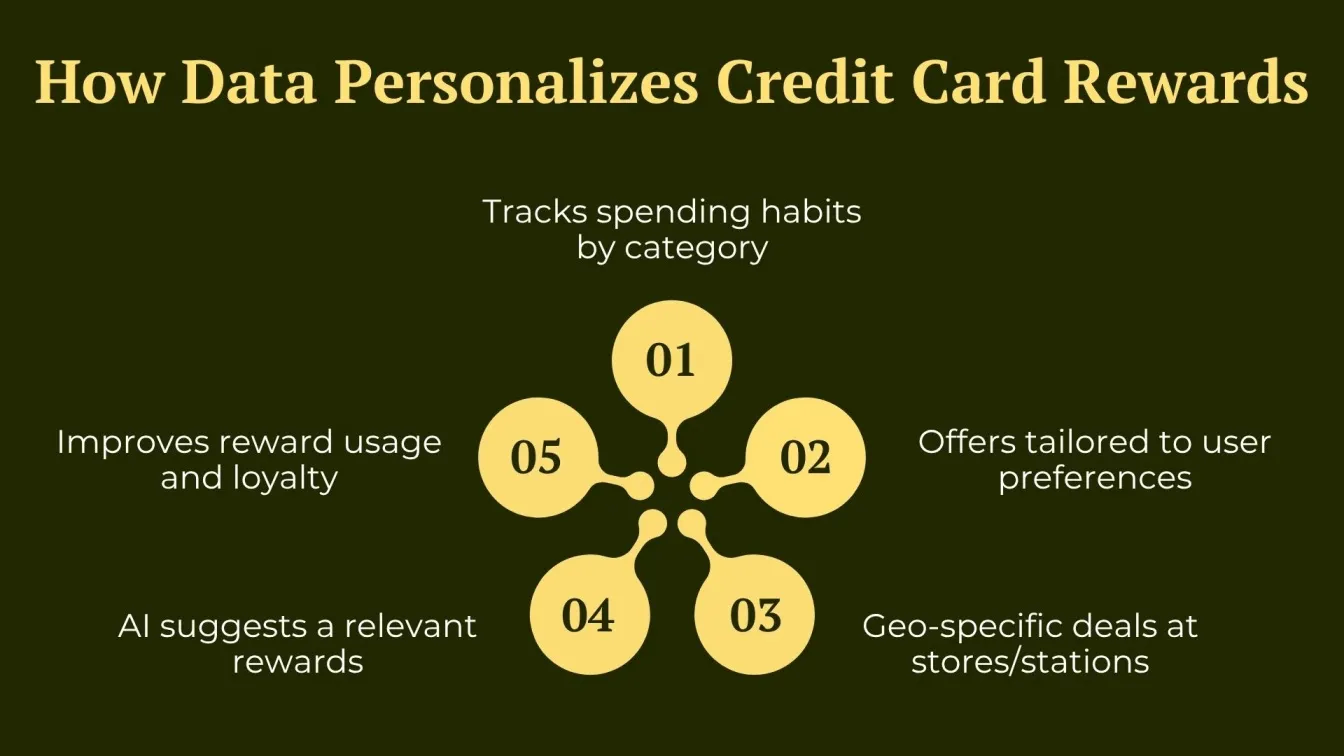

6. Data-Driven Personalization

Issuers analyze credit card transactions to offer personalized rewards at various stations or with major retailers. This increases the percentage of accounts actively using the card. It also boosts the share of balances and credit card revenue.

7. Linking Reward Programs with Financial Habits

Programs reward on-time, secure payments, limit cash advances, and charge late fees. This reduces loan loss provisioning and supports healthy credit card behavior. It improves return on credit card assets and benefits the cardholder agreement.

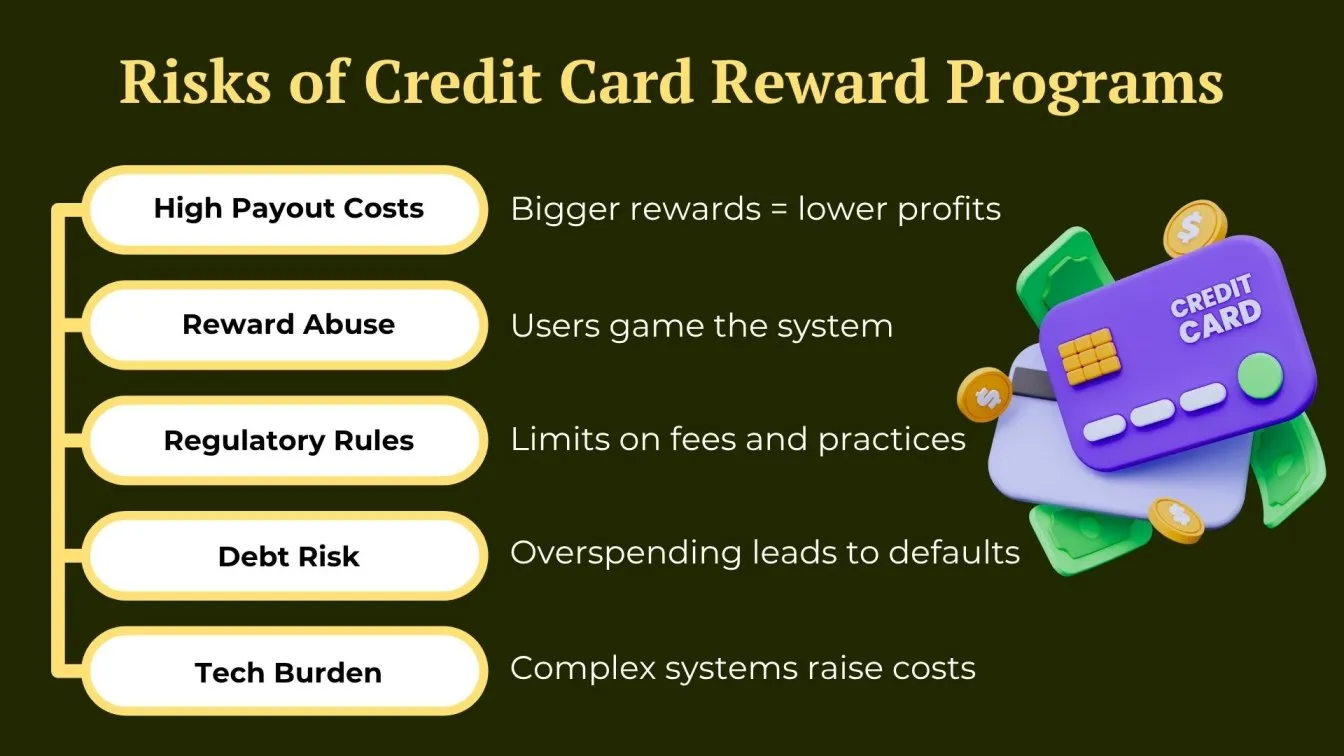

What Are the Risks for Issuers with Reward Programs?

While credit card rewards programs help boost credit card spending and build loyalty, they come with financial and operational risks that issuers must manage carefully to protect credit card profitability.

1. Rising Costs of Rewards Payouts

As competition grows, major issuers increase percent cash offers, miles, or points. Travel rewards and hotel partners drive up interchange expenses, especially with premium cards. If interchange income or interest doesn’t cover this, credit card revenue shrinks.

2. Reward Abuse and Gaming the System

Users exploit balance transfers, cash advances, or transfer partners like Chase Ultimate Rewards to gain rewards without real credit card purchases. This weakens return on credit card programs and leads to higher loan loss provisioning.

3. Regulatory and Compliance Pressure

Rules from the Board of Governors and other regulators may restrict interchange rate levels or fee practices. Oversight affects revenue from credit card fees and may require changes to credit card program agreements.

4. Reward Inflation and Devaluation

To reduce costs, issuers may lower the value of credit card rewards points or increase thresholds for redemption. This frustrates users and risks churn in the retail credit card market.

5. Credit Risk from High-Spending Users

Rewards often increase spending, but some users fall into credit card debt, especially during the promotional period. Rising share of balances carried month-to-month increases defaults and reduces the return on credit card portfolios.

6. Operational Complexity and Technology Costs

Running complex store-branded cardholders or private label accounts with major retailers requires strong tech systems and fraud risk management controls. These add to overhead, especially when managing millions of dollars in daily balances.

Conclusion: The Future of Credit Card Rewards and Issuer Benefits

Credit card rewards programs are now a key strategy for credit card issuers to attract and retain users. Whether it's a cash rewards credit card, a travel rewards credit card, or the best hotel rewards credit card, these perks drive spending and loyalty.Going forward, programs will become more digital, personalized, and integrated with platforms used by e-wallet service providers, enhancing seamless transactions, reward points, and redemption. Issuers will use data to tailor credit card perks and manage costs more efficiently. However, they must watch rising interchange fees, changing regulations, credit card debt, and the risk of overspending.The best credit card issuers will balance innovation with sustainability, offering valuable rewards while staying profitable through smart payment method strategies.

Frugal Testing, a leading SaaS application testing company, is renowned for its specialized AI-driven test automation services tailored to meet the evolving needs of modern businesses. Among the comprehensive services offered by Frugal Testing are advanced Fintech Software Testing Services, designed to ensure security, performance, and compliance in financial applications. The company also provides cloud-based test automation services, enabling scalable, efficient, and cost-effective testing solutions for fast-paced digital environments.

People Also Ask

How is rewards data used by credit card companies?

Credit card companies analyze rewards data to understand customer spending habits. This helps them create personalized offers and improve retention strategies.

Are credit card rewards taxable?

Generally, rewards earned through spending are not taxable, but bonuses or rewards given without a purchase may be considered taxable income.

How do digital wallets integrate with rewards programs?

Digital wallets like Apple Pay or Google Pay often support rewards cards, allowing users to earn and redeem points seamlessly during mobile transactions.

How do co-branded credit cards differ from standard reward cards?

Co-branded cards are issued in partnership with airlines, hotels, or retailers and offer brand-specific perks, unlike standard cards that provide general rewards.

Which algorithms personalize rewards based on spending?

Credit card companies use machine learning algorithms like clustering and recommendation systems to analyze spending patterns. This helps them offer customized rewards that align with individual user behavior and preferences.