.webp)

India's push toward a cashless society is accelerating, and UPILite is redefining the way offline payments happen in the country. Backed by NPCI India and integrated into platforms like the BHIM UPI app, UPILite bridges the gap in digital payments by enabling seamless transactions without internet access.

As the digital economy India evolves, innovations like NFC mobile payments, digital wallet payments, and NFC based payment systems are empowering users in low-connectivity zones. With the growing adoption of fintech companies in India, UPILite is shaping the future of digital payments, making the digital payments industry more inclusive, efficient, and prepared for real-time financial needs.

What’s next? Keep scrolling to find out:

🚀 Introduction to UPILite: Driving offline payments and financial inclusion in India.

🚀 How UPILite Works & Key Features: Simplifying transactions with limited internet access.

🚀 Transforming Digital Payments: Bridging the digital divide and empowering small businesses.

🚀 UPI vs UPILite: Understanding transaction limits and offline capabilities.

🚀 RBI’s Push & Future Scope: Supporting India’s cashless economy and digital payment adoption.

What is UPILite and how does it work

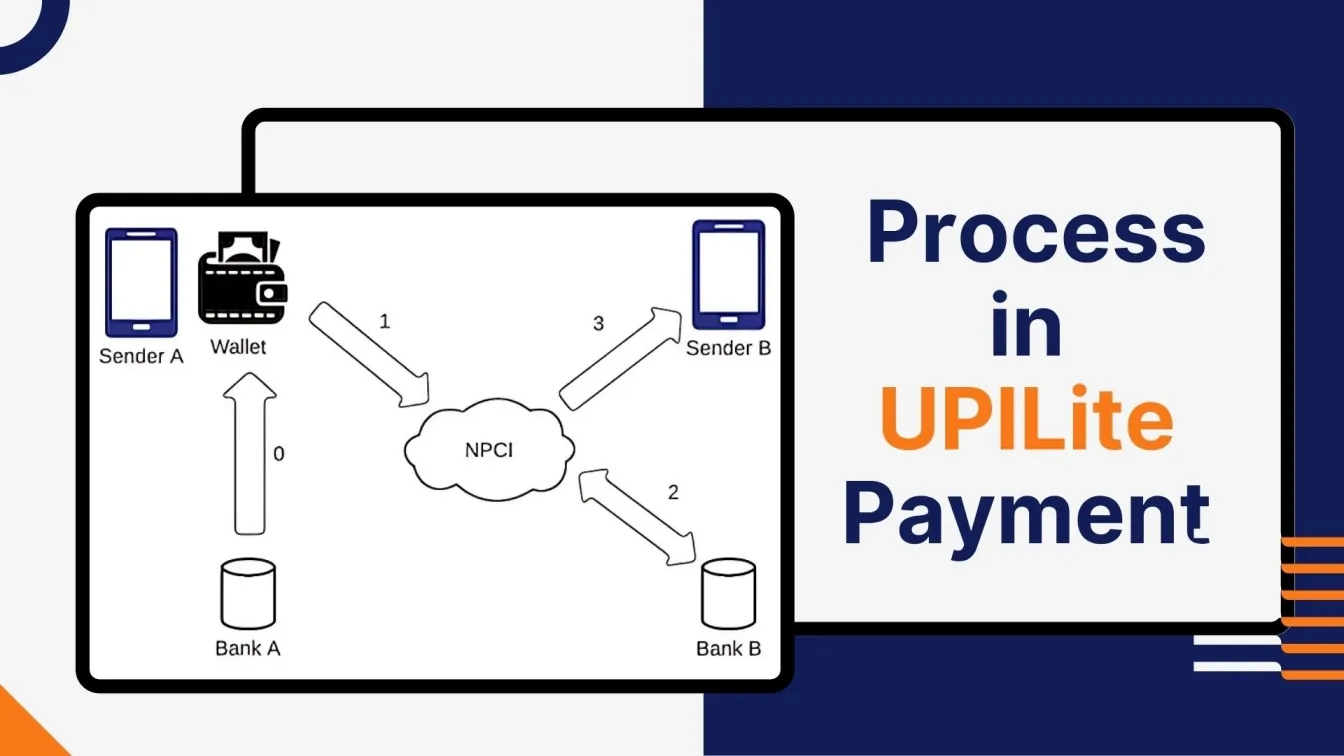

UPILite is an innovative extension of the Unified Payments Interface (UPI) designed specifically to enable seamless digital payments even in areas with poor or no internet connectivity. Developed by NPCI India, UPILite allows users to carry out small-value offline transactions by leveraging an on-device digital wallet. This means funds are stored locally on the user’s device, making payments possible without a live connection to bank servers, which is especially useful for daily low-value purchases.

Key factors of how UPILite works include:

- Users can transact up to ₹500 per transaction, with a maximum wallet balance capped at ₹2,000 for added security and control.

- UPILite is integrated into popular platforms such as the BHIM UPI app, supported by leading fintech companies in India to boost financial inclusion.

- It reduces the dependency on real-time network connections by processing and settling multiple transactions in batches once the device reconnects to the internet.

- This approach helps ease the load on digital payments platforms and banking infrastructure, ensuring smoother operations and higher transaction success rates.

- UPILite is aligned with emerging fintech trends in India, including offline capabilities similar to Stripe offline payments and PayPal offline payments, but tailored for the Indian market.

- Future versions may incorporate NFC mobile payments technology to enhance ease of use through contactless transactions.

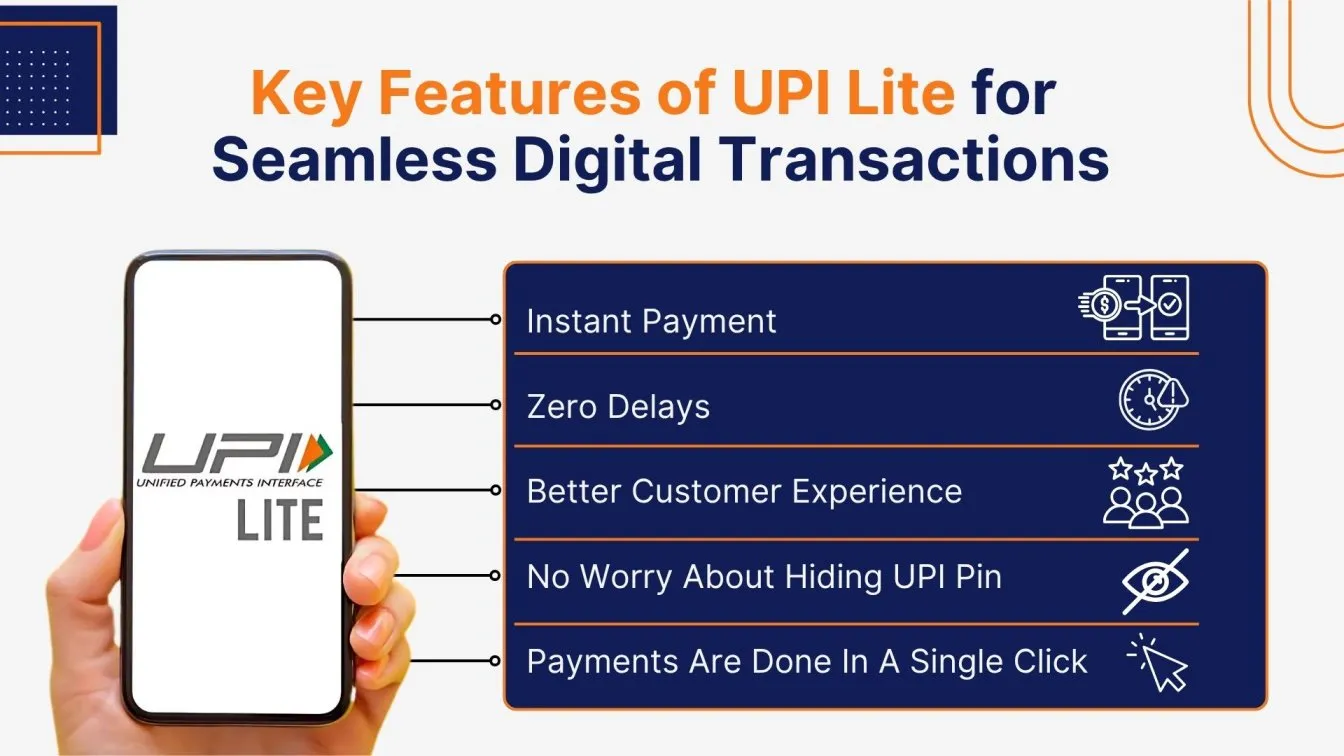

Key features of UPILite for offline transactions

UPILite is transforming the digital payments platform in India by enabling smooth offline transactions, especially in low-connectivity areas. Here are its key features:

- NFC-enabled payments: Utilizes NFC digital wallet and NFC mobile payments to allow contactless offline transactions between devices.

- Integration with BHIM UPI app: Works seamlessly with the trusted BHIM UPI app, leveraging NPCI’s secure infrastructure.

- Offline transaction processing: Supports local storage of payment data, enabling users to transact without internet and settle transactions later.

- Supports low-value transactions: Designed for everyday purchases typically up to ₹200, making it ideal for rural and small business use.

- Reduced dependency on bank servers: Minimizes load on NPCI India and banking systems, ensuring faster transaction approval and higher success rates.

- Compatibility with fintech companies in India: Works alongside leading fintech platforms to broaden acceptance and usability across merchant networks.

- Secure and interoperable: Built on NPCI UPI standards, ensuring high security and interoperability across banks and payment apps.

- Promotes financial inclusion: Empowers unbanked and underbanked populations, driving the growth of the digital economy India.

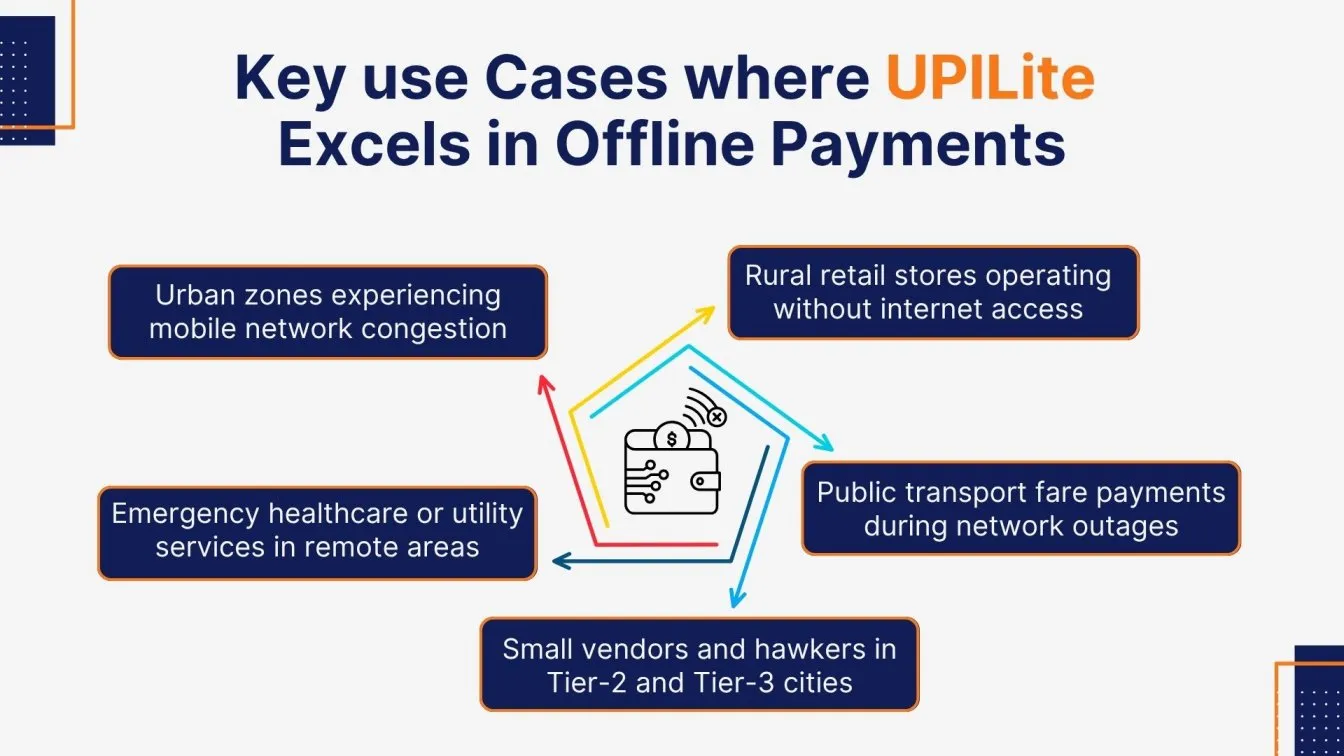

How UPILite is Transforming Offline Payments Across India

UPILite is reshaping the way India transacts by making digital solutions accessible beyond metro areas. It enhances financial participation across different population segments while supporting the larger goal of a robust digital payments ecosystem.

- Offline access without tech hurdles: UPILite empowers users to make financial transactions without the need for an active internet connection, especially benefiting those in regions with limited internet connectivity.

- Simplifies payments at street-level vendors: Using a UPI-enabled app, users can make fast payments in areas with poor connectivity, reducing dependence on cash payments in remote and semi-urban zones.

- Supports digital transformation vision: By enabling low-value payments via offline mode, UPILite supports the broader shift toward a cashless economy and reduces friction in digital payment transactions.

- Lightens system load efficiently: With no real-time requirement to ping bank servers, UPILite reduces load on banks, making the digital payment experience smoother for users and more scalable for financial institutions.

- Connects rural India to retail infrastructure: UPILite helps bring digital transactions into everyday retail payments, forming the backbone of a future-ready digital payment method and reinforcing the momentum of the digital payments landscape.

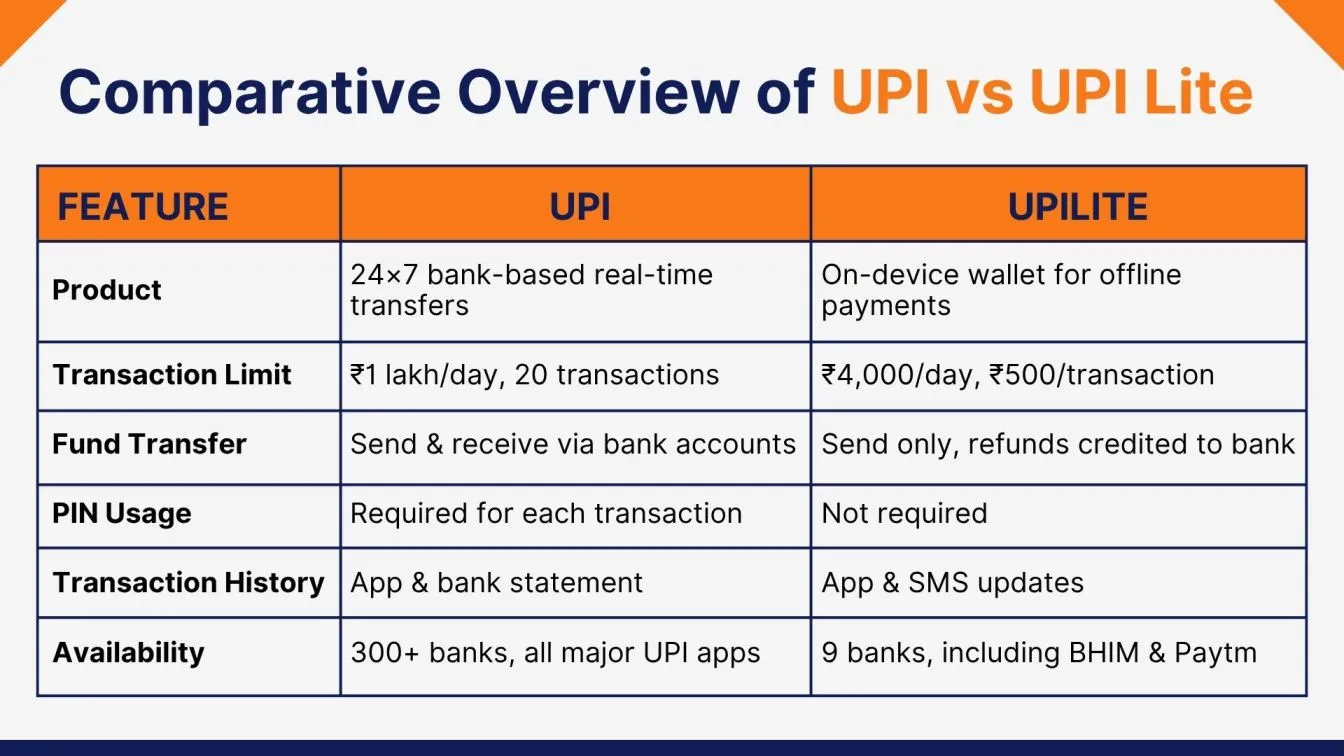

Differences between UPI and UPILite

UPI and UPILite both transform digital transactions in India but differ significantly in functionality and usage, especially for offline payments and low-value transactions. The table below highlights their key distinctions, helping users understand their roles within the digital payment ecosystem.

RBI’s push for offline payment solutions in India

To strengthen the digital payment infrastructure and bridge the digital divide, the Reserve Bank of India (RBI) has actively promoted offline payment solutions. These efforts aim to boost digital payment penetration in rural and low-connectivity regions while enhancing the reliability of cashless payment systems across the country.

- Supporting digital payments in rural zones: The BHIM app now enables seamless offline functionality, expanding its usability in areas with limited internet and encouraging wider adoption of digital payment solutions.

- Promoting NFC-enabled infrastructure: RBI encourages NFC for payments by supporting NFC transactions and NFC phone payment models, delivering a secure and contactless payment experience without needing an active connection.

- Aligning with digital economy goals: These initiatives are part of broader digital economy trends, aligned with the Digital Economy Act, and informed by insights from the Digital Economy Report.

- Boosting fintech collaboration: By engaging with top fintech companies in India and every emerging fintech company in India, the RBI is fueling innovation in fintech in India and advancing nationwide financial inclusion.

- Spreading awareness and adoption: RBI's campaigns highlight the advantages of digital payments and introduce the public to various types of digital payments, accelerating digital payment adoption and minimizing reliance on traditional payment methods.

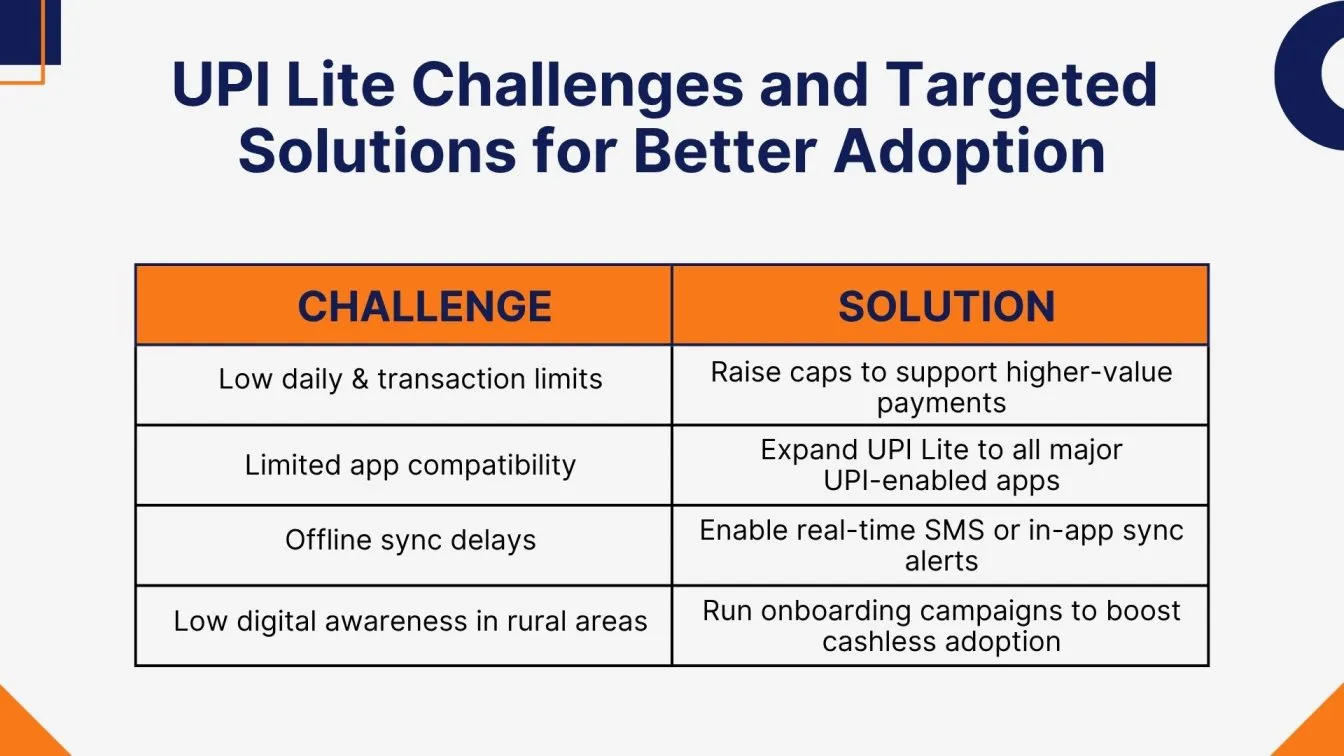

Challenges and future scope of UPILite in digital payments

Challenges of UPI Lite in Digital Payments:

UPI Lite, despite its simplicity and offline utility, faces several challenges that impact large-scale adoption and user trust. These hurdles are primarily linked to ecosystem limitations and feature constraints.

- Restrictive daily and transaction limits: With a low daily limit and a capped maximum limit for each single transaction, UPI Lite struggles to replace debit cards or regular online payments for many users.

- Limited compatibility with apps: UPI Lite works only with selected UPI-enabled apps, like the BHIM App, reducing its reach compared to other digital payment solutions.

- Offline sync delays: While it supports instant payments, transactions conducted without the internet may not reflect immediately in bank accounts, leading to confusion and reduced transparency.

- Digital divide and user awareness: In regions with weak infrastructure, the digital divide affects adoption. Many users are still unfamiliar with mobile wallets and require support to adopt cashless payment tools confidently.

Future Scope of UPI Lite in Digital Payments:

As India advances its digital economy goals, UPI Lite holds great potential to lead micro-payment innovation and expand financial inclusion with smart enhancements.

- Expansion of UPI Lite X: The upcoming UPI Lite X aims to support offline debit transactions between two devices, broadening use cases for peer-to-peer transfers in areas with poor connectivity.

- NFC-based integrations: Adoption of NFC based payment, including NFC card payment and NFC phone payment, could enable seamless NFC transactions for small purchases, transforming India’s offline payments Square landscape.

- Bridging gaps in rural commerce: UPI Lite can empower underserved merchants by enhancing consumer spending with frictionless low-value payments.

- Boost to digital payment penetration: The rising focus on digital payments in India and supportive government initiatives will fuel digital payment adoption, especially where traditional payment methods fall short.

- Evolving trends in digital payments: With the shift toward real-time, low-bandwidth solutions, UPI Lite aligns perfectly with current trends in digital payments and the larger digital payments ecosystem.

Final Thoughts

UPI Lite is redefining how India handles everyday payments by making digital transactions accessible, even without the internet. As the digital payment landscape evolves, its role in enabling seamless, secure, and offline-ready experiences will only grow. With continued support from fintech in India and innovations like UPI Lite X, the future of digital payments is faster, smarter, and more inclusive, bridging gaps and powering the nation toward a truly cashless economy.

UPI Lite is redefining how India handles everyday payments by making digital transactions accessible, even without the internet. As the digital payment landscape evolves, its role in enabling seamless, secure, and offline-ready experiences will only grow. Just as frugal testing, AI-driven test automation services, and functional testing solutions support robust fintech ecosystems, services like SaaS application testing company, bug testing services, software load assessment services, and Frugal Technologies Pvt Ltd ensure smooth UPI integration, enhancing trust and scalability in India’s digital economy.

People Also Ask

What are the major differences between UPI and CBDC?

UPI enables real-time bank transfers via digital infrastructure, while CBDC is a centralized, government-issued digital currency regulated by the RBI.

What are the regulatory frameworks guiding the rollout and operation of UPILite?

UPILite follows RBI’s offline payment guidelines, including KYC compliance, security protocols, and transaction limits for safer digital access.

What are the macroeconomic implications of mass-scale UPI adoption in India?

UPI promotes cashless transactions, increases formal economy participation, and enhances digital transparency across consumer and business sectors.

How does UPILite align with the Reserve Bank of India’s financial inclusion objectives?

UPILite supports RBI’s inclusion goals by offering seamless offline payments to users in areas with poor or limited internet connectivity.

How has the UPI ecosystem reshaped customer behavior and expectations in digital transactions?

It has set new norms for speed, convenience, and trust, leading to a rapid shift from cash-based to digital-first transaction behavior.