India's digital payments ecosystem is evolving rapidly, and UPI 3.0 is at the forefront of this transformation. With advancements in UPI payments, users can now enjoy smoother, safer, and more versatile UPI transactions than ever before. From UPI registration to real-time transfers via Google Pay, Paytm, BHIM app, and Amazon Pay, the shift to digital payments in India is undeniable.

As fintech companies in India lead the innovation curve, the future of digital payments looks increasingly secure. Whether it's UPI login, digital wallet payments, or enhanced security testing, UPI 3.0 is redefining how India handles money. Let’s explore the key features, benefits, and what this means for the digital payments industry going forward.

What’s next? Keep scrolling to find out:

🚀 Understanding UPI 3.0: How it works and what sets it apart from previous versions.

🚀 Key Features of UPI 3.0: One-time mandates, invoice verification, enhanced security, and offline payments.

🚀 Comparing UPI 2.0 vs UPI 3.0: Major improvements in user experience and payment flexibility.

🚀 Benefits for Users and Merchants: Faster payments, transparency, and stronger security measures.

🚀 Top UPI 3.0 Apps in India & Future Impact: Features of Google Pay, PhonePe, Paytm, BHIM, Amazon Pay, Mobikwik, WhatsApp Pay, and UPI’s role in India’s cashless future.

What Is UPI 3.0 and How It Works

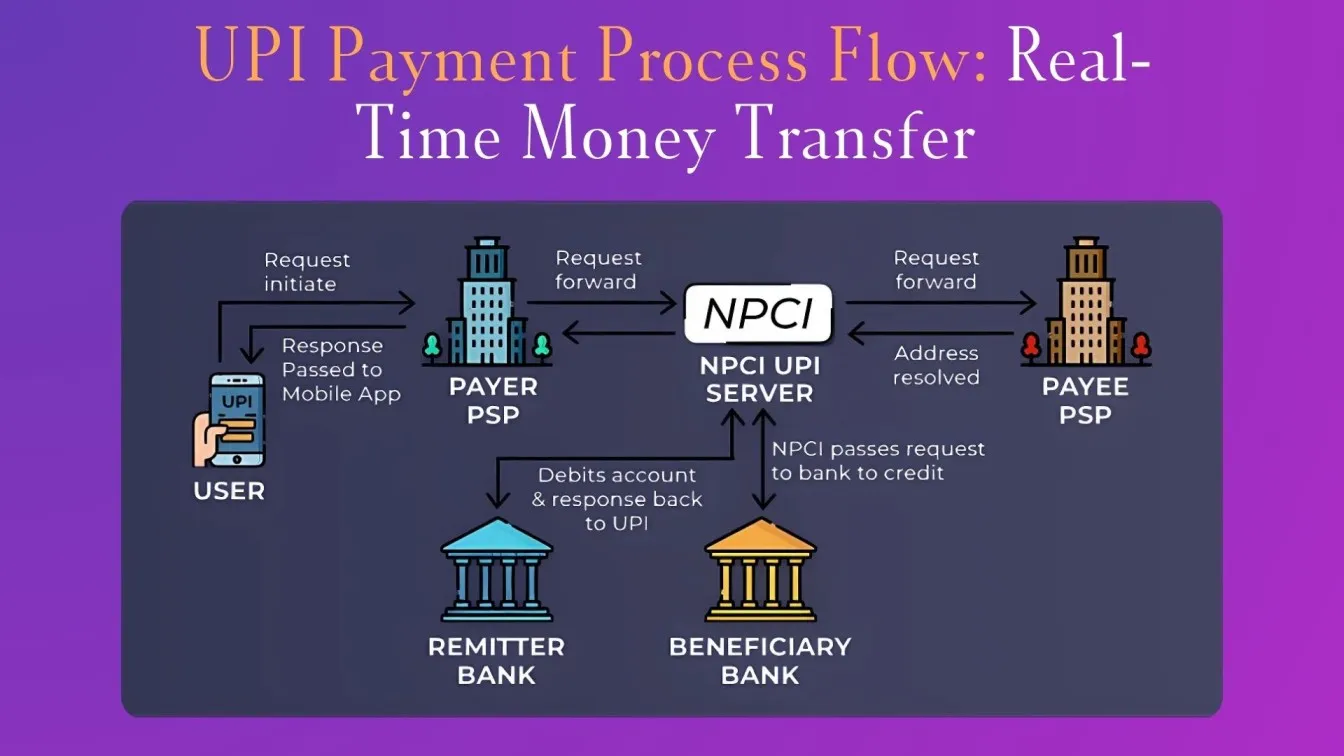

UPI 3.0, developed by the National Payments Corporation of India (NPCI), is the latest upgrade to the Unified Payments Interface that builds on earlier versions by introducing advanced security, flexibility, and user-centric features. Unlike previous versions, UPI 3.0 not only allows instant bank-to-bank transfers but also integrates future-ready capabilities that streamline recurring payments and improve transaction transparency.

How UPI 3.0 Works:

- Transaction Initiation: Users initiate payments via their UPI-enabled app, selecting payees or scanning QR codes. With UPI 3.0, these QR codes are digitally signed, ensuring authenticity and reducing fraud risks.

- One-Time Mandates: For recurring payments like subscriptions or EMIs, users can set up one-time mandates, authorizing future transactions without needing manual approval each time. This is a significant step up from earlier UPI versions that required manual payment approval for every transaction.

- Invoice Verification: Before approving a payment, users receive detailed invoices or transaction summaries within the app, enhancing transparency and trust, unlike earlier versions that lacked this integrated invoice view.

- Biometric Authentication: UPI 3.0 supports biometric verification such as facial recognition and fingerprint scanning, making payments more secure compared to the PIN-only approach used previously.

- Offline Transaction Capability: Payments can be authorized even without active internet connectivity, thanks to offline transaction support, expanding usability in areas with limited network access.

- Overdraft Facility: Users can now link overdraft accounts for payments, offering more flexibility beyond regular bank accounts.

Key Features Introduced in UPI 3.0

UPI 3.0 brings significant backend advancements and technical upgrades that enhance system robustness, security, and future scalability. These improvements are critical in supporting India’s expanding digital payment ecosystem and meeting the growing demand for secure, seamless transactions across various platforms.

- Advanced API Security Testing: UPI 3.0 employs comprehensive API security testing protocols, ensuring that all data exchanges between apps and banks are protected from vulnerabilities and cyber threats, boosting software quality and reliability.

- Digitally Signed QR Codes: Each QR code is cryptographically signed, which prevents phishing attacks and fraudulent redirection, reinforcing trust among users and merchants during transactions.

- Increased Transaction Limits: UPI 3.0 supports higher daily transaction volumes, enabling large-value payments and enhancing sales potential for businesses with substantial digital transactions.

- Automated Payment Scheduling via One-Time Mandates: This feature streamlines recurring payments like subscriptions and EMIs, reducing manual intervention and improving customer satisfaction with hassle-free billing.

- Overdraft Facility Integration: The inclusion of overdraft accounts expands the financial ecosystem, giving users more flexible payment options beyond regular savings or current accounts.

- Cross-Border Transaction Readiness: UPI 3.0 lays the technical foundation for international payment interoperability, paving the way for cross-border commerce and a global digital economy.

- Enhanced Data Encryption: Employing end-to-end encryption techniques safeguards sensitive user information, supporting compliance with strict data security standards and strengthening customer trust.

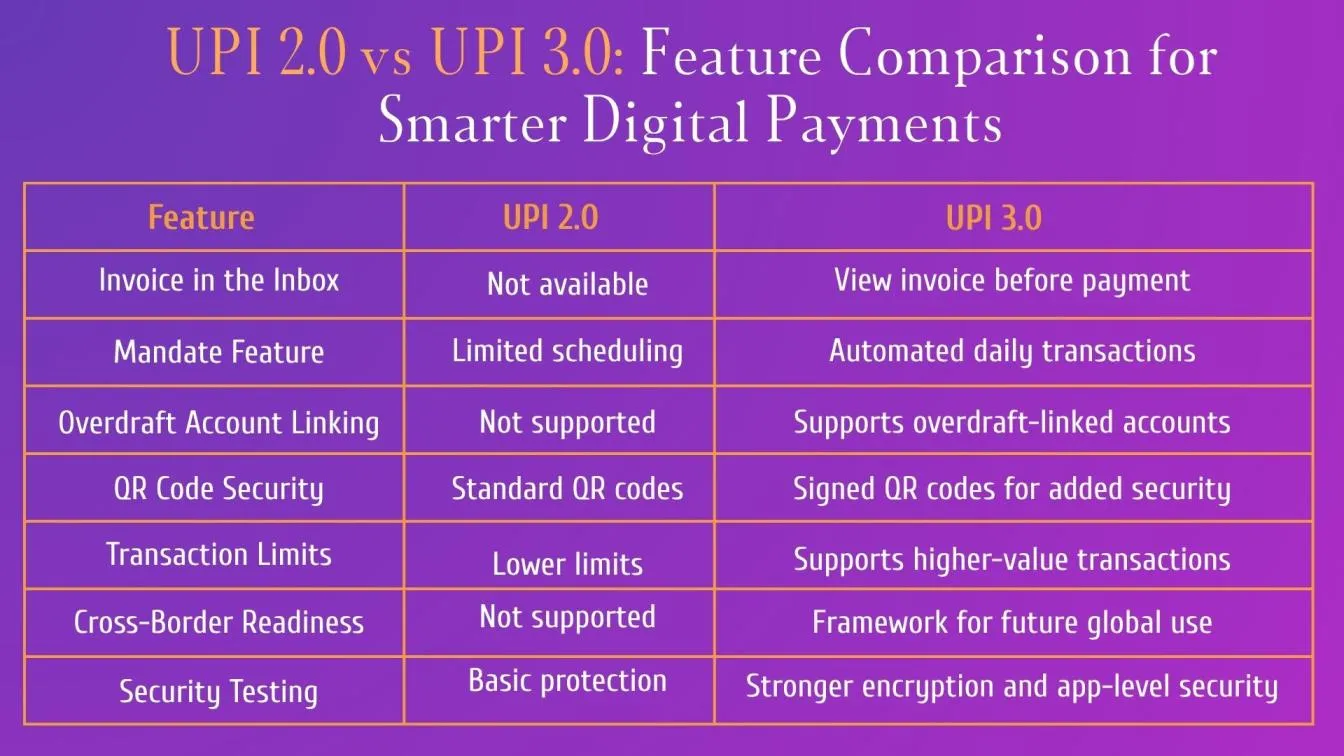

Difference Between UPI 2.0 and UPI 3.0

The evolution from UPI 2.0 to UPI 3.0 marks a significant shift in India’s journey toward a fully digital and cashless economy. Both versions have contributed to revolutionizing digital payments, but UPI 3.0 introduces enhanced features that improve customer experience, security, and inclusivity in mobile payments.

Here's a quick comparison to understand how the Unified Payments Interface has progressed to meet changing consumer and financial services demands.

Benefits of UPI 3.0 for Users and Merchants

UPI 3.0 brings advanced capabilities that redefine the digital payment ecosystem in India. With an emphasis on mobile wallets, contactless payments, and better security, this version supports both users and merchants in making smoother, safer, and faster cashless transactions. It also enhances the customer experience by integrating intelligent features tailored to modern financial needs.

- Enhanced Trust and Transparency: Merchants can share signed invoices directly to the user’s payment app, allowing them to review before making UPI payments, increasing transparency.

- Recurring and Scheduled Payments: Through the mandate feature, users can automate bill payments, subscriptions, and rent transfers, improving financial inclusion and ease of use.

- Improved Customer Satisfaction: Reduced errors in digital transactions and faster dispute resolution enhance overall customer satisfaction.

- Support for Offline Payments: UPI 3.0 enables offline payments, essential for rural areas with poor connectivity, aiding secondary users and expanding digital payment solutions.

- Biometric Payments Integration: The introduction of facial recognition and fingerprint-based verification boosts security during mobile payments.

- Reduced Transaction Fees: Helps merchants accept a wide range of payments without high transaction fees, supporting cashless payment systems.

- Increased Accessibility: Features like UPI registration and seamless UPI login make it easier for new users to adopt digital payment methods.

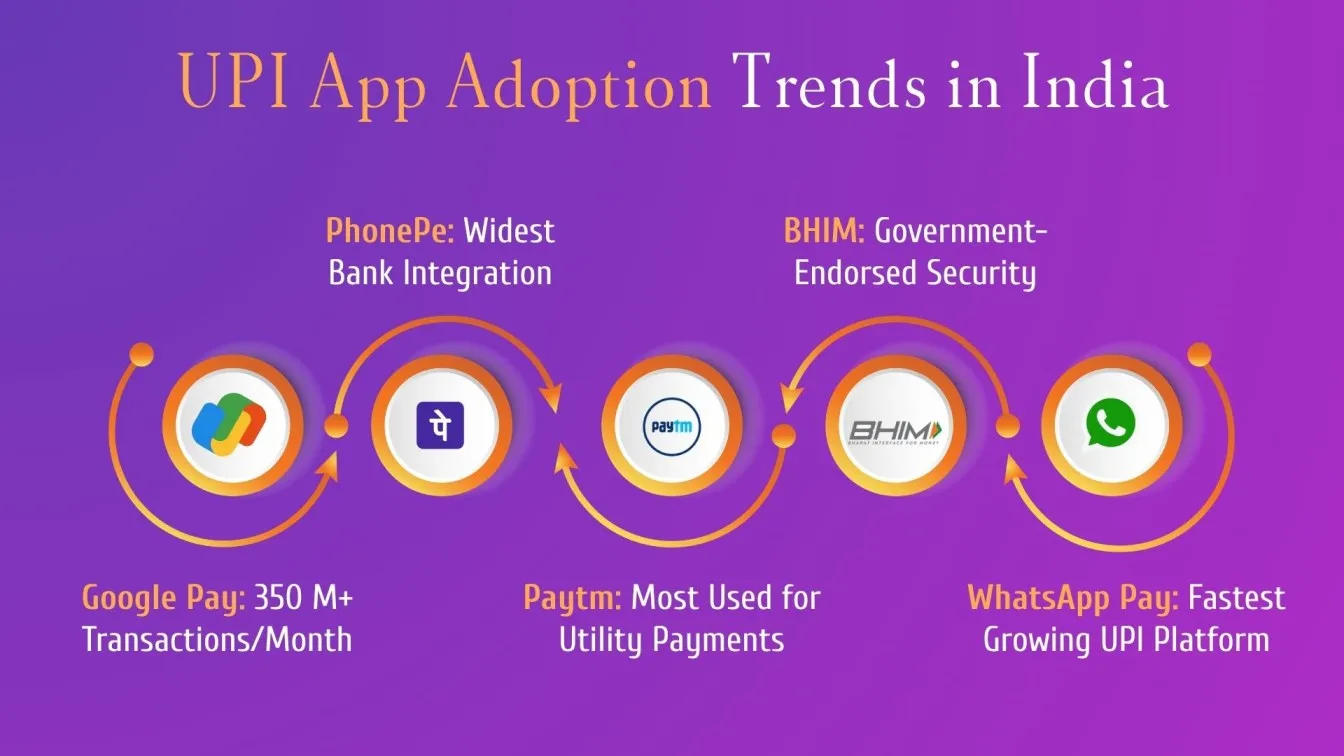

Popular UPI Apps Supporting UPI 3.0 in India

India’s digital payment landscape has rapidly expanded, with major mobile payment apps integrating Unified Payments Interface (UPI) 3.0 to enhance cashless transactions and streamline the payment process.

- Google Pay App: Popular for its user-friendly interface, Google Pay now supports UPI 3.0 features, including UPI login, digital currency support, and real-time mobile payments using a virtual card.

- Paytm App: Known for Paytm Payments Bank and the Paytm wallet, it supports UPI payments, recurring mandates, and digital payment systems suited for both users and merchants.

- Amazon Pay: With options like Amazon Pay Later and Amazon Pay Bill, it provides seamless UPI transactions, ideal for quick online purchases and daily transactions.

- BHIM UPI App: A government initiative supporting full UPI 3.0 compatibility, the BHIM App ensures secure bank digital connectivity and supports offline payments.

- PhonePe: One of the top mobile app choices for cashless payment options, enabling quick financial transactions and utility payments.

- WhatsApp Pay: Built into WhatsApp, it enables direct digital transactions via UPI, allowing users to send money from chats while maintaining customer satisfaction and simplicity.

Google Pay

Google Pay leverages UPI 3.0 to deliver a highly intuitive and secure payment experience, widely trusted by millions across India. It stands out with its deep merchant partnerships and smart notifications that simplify payment tracking.

Google Pay’s UPI 3.0 Highlights:

- Smart One-Time Mandates: Enables seamless recurring payments with intelligent reminders for upcoming dues, improving user convenience in Google Pay account management.

- Invoice Transparency: Users receive detailed bills to validate payments before approval, reducing errors during Google Pay online transactions.

- Advanced Biometric & Behavioral Security: Combines facial recognition with AI-based fraud detection to protect the Google Pay wallet from unauthorized access.

- Broad QR Code Acceptance: Compatible with diverse merchant QR formats nationwide, making Google Pay send money widely usable across platforms.

- Offline Mode with Auto-Sync: Supports offline transactions that automatically sync when connectivity is restored, enhancing reliability for both users and merchants using Google Pay for business.

- Virtual Card Support: Integrates Google Pay virtual card to add an extra layer of payment security and ease for digital purchases.

PhonePe

PhonePe excels by combining UPI 3.0 features with a comprehensive digital ecosystem that integrates bill payments, mutual funds, and insurance, offering more than just payments. As one of the top fintech companies in India, it leads innovation in digital finance.

PhonePe Features with UPI 3.0:

- Mandate Setup for Financial Products: Supports recurring payments for insurance premiums and mutual fund SIPs, reflecting emerging fintech trends in India.

- Invoice Validation with Payment Options: Provides bill clarity while suggesting convenient payment modes, enhancing the UPI India payment experience.

- Multi-Biometric Authentication: Employs fingerprint, face, and voice recognition backed by rigorous mobile app security testing and cyber security testing to safeguard users.

- Offline Payment Accessibility: Ensures uninterrupted payments in low-network zones, reinforcing UPI payment India reliability.

- Unified Wallet Integration: PhonePe wallet seamlessly merges with UPI, offering flexible digital payments and strengthening its position as a leading fintech company in India.

BHIM App

As the official government-backed UPI app, BHIM focuses on simplicity, security, and financial inclusivity, making UPI 3.0 features accessible to all user segments. Its multilingual interface and seamless government service integration promote wider digital payment adoption.

BHIM App’s Unique UPI 3.0 Advantages:

- One-Time Mandates for Utility Payments: Enables easy scheduling for recurring bill payments and government services.

- Multilingual Invoice Display: Enhances transparency by supporting multiple Indian languages.

- Robust Security Protocols: Government-grade biometric authentication combined with advanced security measures protects user data.

- Flexible QR Interoperability: Compatible with any UPI QR code, expanding nationwide merchant acceptance.

- Low Bandwidth Offline Payments: Optimized for rural areas with unreliable internet, enabling seamless transactions.

Amazon Pay

Amazon Pay seamlessly integrates UPI 3.0 within its extensive e-commerce platform, offering users a fast and reliable digital payment option that supports the cashless future of India. It enhances the form of payment by enabling smooth transactions, making the future of payments more accessible and secure for millions of shoppers.

Amazon Pay’s UPI 3.0 Strengths:

- Scheduled Payments for E-Commerce: Automatically manages EMIs, subscription renewals, and other recurring payments, streamlining user convenience.

- Invoice in Purchase History: Provides detailed digital invoices linked directly to Amazon orders, improving transparency and payment tracking.

- Payment Security Layers: Combines biometric authentication with real-time backend fraud monitoring to protect user data and transactions.

- High-Value Transaction Support: Supports large-value payments during sales, festivals, and exclusive Amazon events, accommodating diverse shopping needs.

- Wallet and UPI Combo: Offers flexible payment choices by combining wallet balance and direct bank payments for a hassle-free checkout experience.

Mobikwik

Mobikwik’s wallet-first strategy is now elevated with UPI 3.0, blending digital wallet convenience with instant bank transfers for a seamless digital payment option. This integration supports the evolving demands of India’s cashless economy, making Mobikwik a preferred choice for millions.

Mobikwik’s Distinct UPI 3.0 Features:

- Recurring Payment Mandates for Investments: Facilitates automated payments for SIPs and other systematic investments, ensuring timely transactions without manual intervention.

- Digital Invoice Integration: Enables clear, detailed invoicing linked with both wallet and UPI payments, enhancing transparency and user trust.

- Strong Biometric Security: Combines fingerprint and facial recognition technologies with frequent security audits to safeguard user accounts and prevent fraud.

- Robust Offline Transaction Support: Allows users to make payments even without internet connectivity, boosting financial inclusion in remote and low-network areas.

- Wide QR Code Compatibility: Supports payments through both national and local merchant QR codes, providing broad usability across India’s diverse retail landscape.

WhatsApp Pay

WhatsApp Pay uniquely integrates UPI payments within India’s most popular messaging app, making money transfers as easy as sending a chat. Leveraging UPI 3.0, WhatsApp Pay combines convenience with advanced security features, redefining the future of payments for millions of users.

WhatsApp Pay’s UPI 3.0 Highlights:

- Smart Chat-Based Reminders: WhatsApp Pay sends intuitive reminders for due payments, EMIs, and subscriptions right within the conversation thread, keeping users informed in real time.

- Contextual Payment Flows: Payment options appear contextually during relevant conversations (like splitting a bill or gifting), streamlining peer-to-peer transfers without disrupting the chat experience.

- Multi-Language Support for Transaction Prompts: UPI actions and invoice confirmations are available in multiple Indian languages, enhancing inclusivity for regional users.

- High Limit Payments for Groups: Facilitates seamless handling of group expenses, events, and larger transfers, making it ideal for social payments.

- Offline Payments via UPI: Users can complete transactions even with poor or no internet connectivity, supporting financial inclusion across India’s diverse regions.

The Role of UPI 3.0 in India’s Digital Future

UPI 3.0 is a transformative upgrade in India's digital payments ecosystem, driving financial innovation and inclusion. It strengthens the foundation of secure, real-time transactions while offering a better user experience across platforms like Paytm, Google Pay, Amazon Pay, and BHIM App. As a part of India’s fintech revolution, UPI 3.0 plays a vital role in expanding digital reach and enabling smarter transactions.

Highlights of UPI 3.0 Driving India’s Fintech Evolution:

- Mandate Feature for Future Transactions: Simplifies recurring payments such as EMIs, insurance, and subscriptions through one-time approvals.

- Digital Invoice Attachments: Users can verify merchant invoices before paying, improving trust and reducing transaction disputes.

- Enhanced Security Architecture: Built-in multi-layer authentication ensures advanced fraud detection and data protection.

- Offline Payment Support: UPI 3.0’s offline capabilities help users transact without an internet connection, especially useful in rural India.

- Increased UPI Limits: Allows users and businesses to transfer higher amounts, enabling broader adoption across industries.

- Interoperability with UPI Apps: Ensures smooth integration across all major apps and banks using standard UPI protocols.

- Support for Loyalty and Rewards: Merchants can link loyalty programs, cashback, and rewards directly to UPI payments, enhancing engagement.

Final Thoughts

UPI 3.0 is revolutionizing India’s digital payment landscape by combining enhanced security, seamless offline capabilities, and smart transaction features. Leading apps like Google Pay, PhonePe, and WhatsApp Pay are driving this cashless future with innovative digital payment options that cater to diverse user needs. Embracing these advancements unlocks a new era of convenience, trust, and financial inclusion, solidifying India’s position as a global fintech leader.

UPI 3.0 is transforming India’s digital payment ecosystem by offering enhanced security, seamless offline transactions, and smart payment features through leading apps like Google Pay, PhonePe, and WhatsApp Pay. This cashless future relies heavily on robust support from top software testing companies, including those providing QA testing services, functional testing solutions, AI-driven test automation services, and cloud-based test automation services, ensuring secure, reliable, and efficient digital payment experiences.

People Also Ask

What are the performance benchmarks for UPI 3.0 under high load conditions?

UPI 3.0 is optimized to support over 100,000 transactions per second, maintaining low latency and consistent uptime during peak traffic.

What are the RBI compliance requirements for apps using UPI 3.0?

Applications must adhere to RBI regulations including full KYC, data localization policies, PCI-DSS compliance, and regular security testing.

Is UPI 3.0 integrated with Bharat Bill Payment System (BBPS)?

Yes, UPI 3.0 supports integration with BBPS through AutoPay, enabling automated recurring bill payments using UPI-linked bank accounts.

Can UPI 3.0 be used for international remittances from India?

UPI 3.0 does not currently support global remittances, but trials are underway with countries like Singapore and the UAE.

How can developers test UPI 3.0 APIs in a staging environment before production?

NPCI provides a developer sandbox that allows complete API testing with mock transactions, mandate flows, and invoice validations.

.webp)