This blog explores the ways in which Venmo provides secure and efficient peer-to-peer (P2P) payments through strong security architecture, AI-powered fraud protection, PCI DSS compliance, and comprehensive performance testing. This blog post explores the ways in which P2P payment systems work, the need for cybersecurity practices, and how scalable infrastructure helps facilitate large-scale online transactions.

For businesses looking to create a P2P payment app like Venmo, this resource provides best practices for secure P2P payment app development.

Introduction

The sudden rise in mobile money and digital payment solutions, fueled by the COVID-19 pandemic, has brought about a paradigm shift in the way people conduct financial transactions globally, with consumers increasingly favoring speed, convenience, and security. In a competitive fintech market, alongside other popular payment solutions such as Cash App, Google Pay, and Apple Pay, Venmo stands out for its Social Feed business model, robust fraud protection, PCI DSS compliance, and extensive banking integrations enabled by its secure cloud-based payment infrastructure.

Understanding Venmo and Its Business Model

A secure peer-to-peer (P2P) payment app needs a sustainable funding model to invest in security architecture, compliance, and performance testing. This is where a robust business model becomes essential.

What is Venmo?

Venmo is a peer-to-peer (P2P) payment app that enables users to send money digitally through connected bank accounts, debit cards, or credit card details. The payment app supports peer-to-peer money transfers, business payments, and merchant payments through a seamless mobile app experience.

Venmo’s Social Feed feature combines social finances with transactions, enabling optional sharing of transactions on social media platforms. The payment app enables users to send money, cash a Check, split bills, and manage mobile money payments using secure authentication methods such as two-factor authentication and biometric authentication methods like face recognition.

What is a Business Model?

A business model is a description of how a business creates and captures value. For fintech, this involves Transaction Fees, Merchant Charges, Subscription Model services, and payment processing income.

Examples of business models are:

- Freemium business model

- SaaS business model

- Subscription Model

- Revenue through the payment gateway

- Revenue through merchants

The business model canvas template with Market Research ensures that key elements meet compliance, scalability, and regulatory requirements.

Venmo’s Business Model Explained

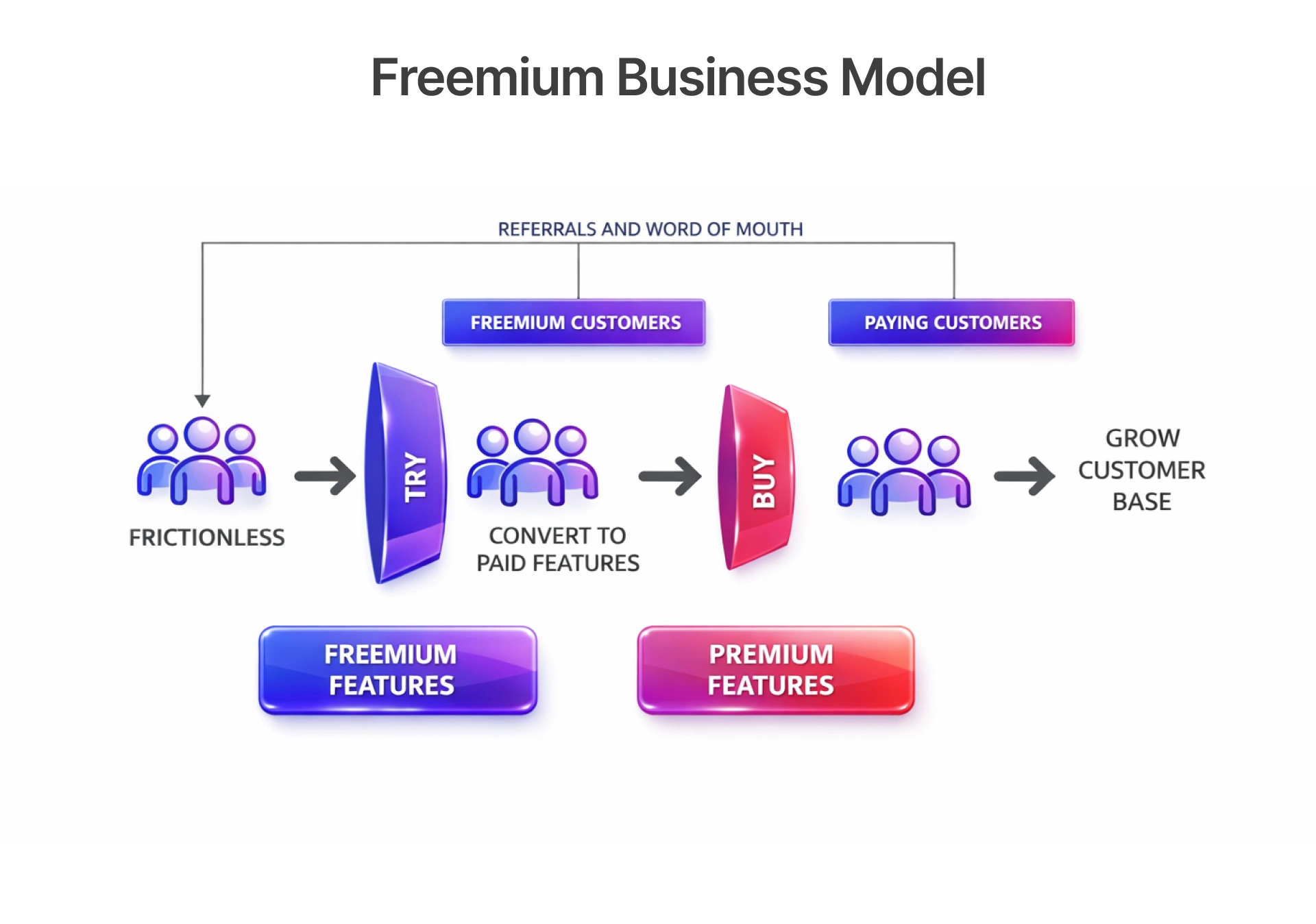

Venmo has a freemium model as its main business structure. The Standard P2P Payment transfer is free, which is a great motivator for people to use the service. The sources of revenue are:

- Instant withdrawal transaction fees

- Credit card processing fees

- Merchant fees

- Business profile transactions

- The sources of revenue enable reinvestment in the following areas:

- Artificial intelligence for fraud detection

- PCI DSS compliance

- ISO 27001 Certified Organization standards

- Security architecture improvements

- Open banking protocols integration

Sustainable funding enables Venmo to make improvements in fraud protection and performance testing.

How Venmo Works: The Mechanics of P2P Transfers

Understanding how Venmo works highlights why continuous testing and layered security are essential.

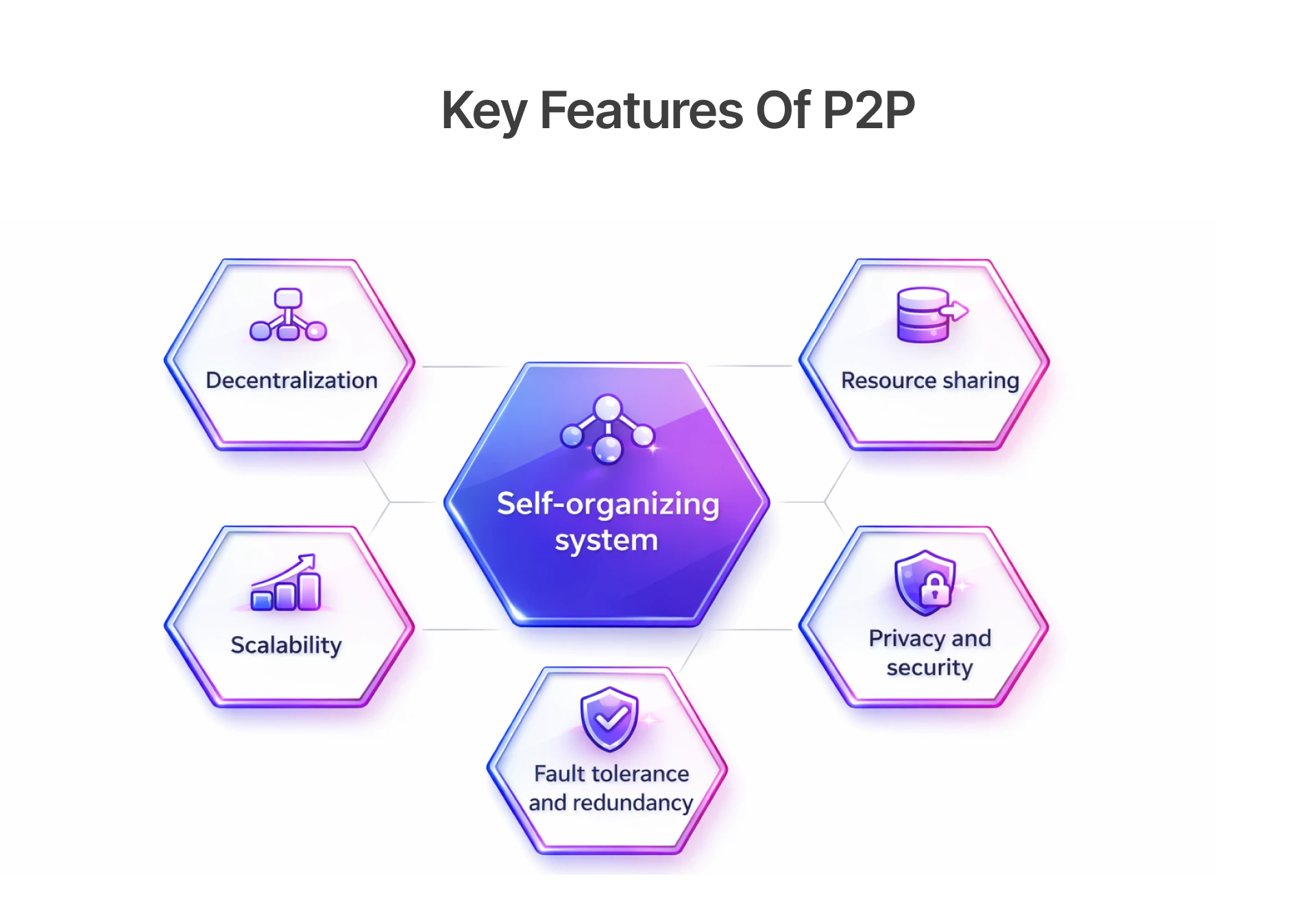

What is P2P Payment?

Peer-to-peer (P2P) payment is the digital transfer of funds from one individual to another using peer-to-peer (P2P) payment solutions. Unlike conventional banking solutions, P2P payment solutions utilize secure APIs, encrypted communication, and banking infrastructure integration to facilitate instant payments.

P2P payment solutions function under very tight Legal and Regulatory Considerations, which may include the EU Payment Services Directive (PSD2).

How Does Venmo Work?

The transaction process on Venmo involves:

- Downloading the app

- Linking a bank account or Debit cards

- Finalizing KYC onboarding and identity verification

- Entering transaction details

- Authenticating via OTP codes, two-factor identification, or multi-factor authentication

- Encrypting data usingSecure Sockets Layer (SSL)

- Processing through secure payment gateways

- Real-time transaction monitoring and confirmation

Behavioral economics patterns such as risk-taking, intertemporal choice, temporal discounting, and irregular transaction behavior are analyzed by artificial intelligence to prevent fraud. Experimental studies and cash transfer experiment knowledge aid in enhancing fraud models.

Venmo also carries out:

- Security Checks

- Monitoring the dispute management system

- Push notifications for suspicious transactions

- Biometric authentication, including face recognition

Venmo Fees and Limits

Venmo fees depend on the type of payment method used. There are no fees for standard transfers, but there are Transaction Fees for instant withdrawals. The use of some credit or debit card details may attract processing fees.

Transaction limits (Venmo limit) are based on the level of verification and the status of KYC onboarding, which helps to minimize identity theft and phishing site risks.

Ensuring Security in Digital Payments

Security Considerations are core to the functionality of secure P2P payment platforms. Without proper IT security measures and forms of network security protection, there are serious security concerns.

Application Security Solutions for Venmo

Venmo integrates:

- Secure socket layer encryption

- Tokenized payment credentials

- Cloud Solutions with restricted access

- Blockchain technology exploration

- Edge Solutions for anomaly detection

These ensure the prevention of data breaches and unauthorized access.

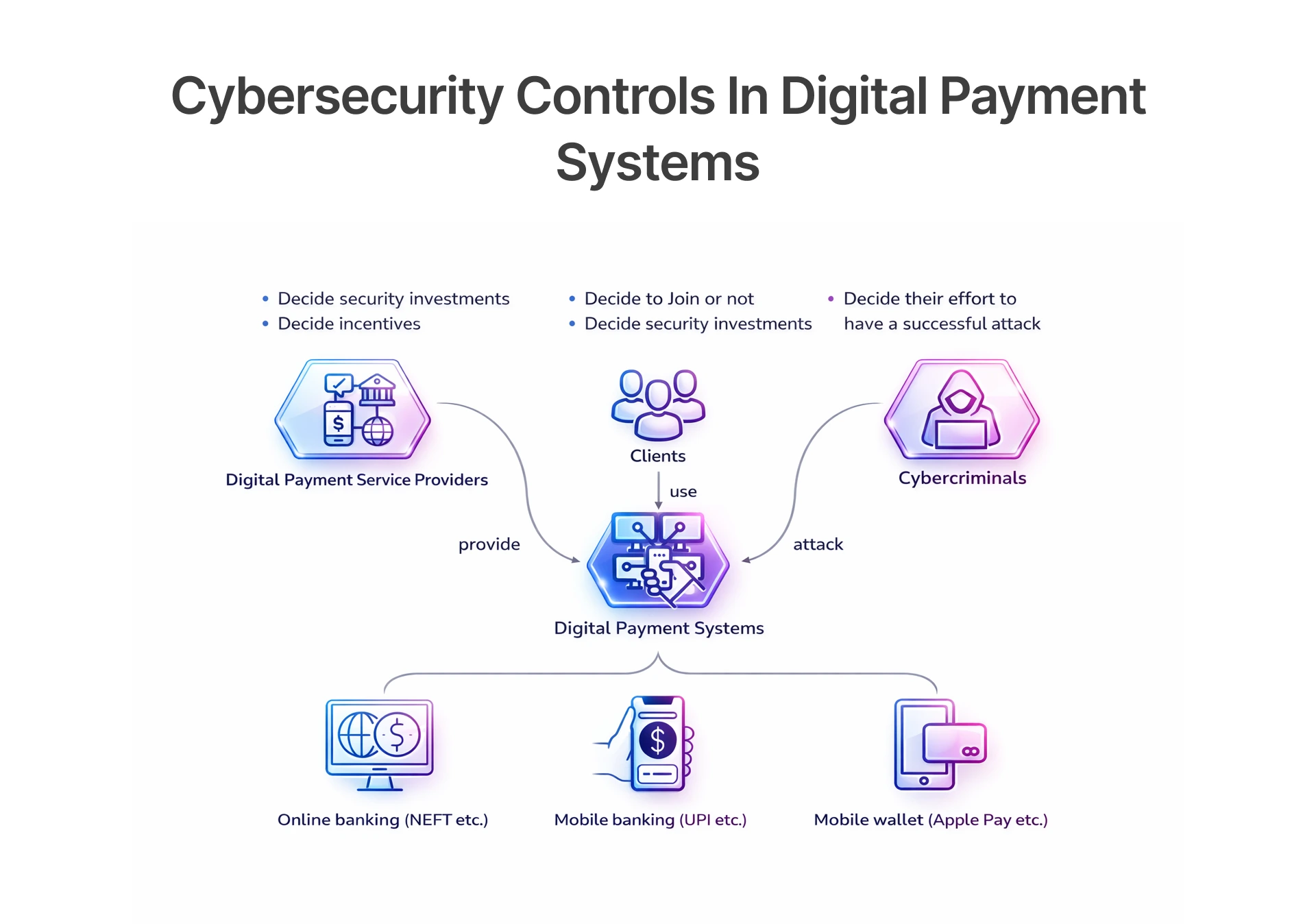

Cyber Security Controls in Digital Payments

Venmo is compliant with the requirements of the following:

- Federal Trade Commission

- Federal Deposit Insurance Corporation

- Consumer Financial Protection Bureau

Security measures include:

- Artificial intelligence fraud protection

- Real-time transaction monitoring

- Two-factor authentication

- Multi-factor authentication

- Biometric authentication

- Face recognition

- OTP codes

- Push notifications

Physical Security Measures for User Protection

Even in digital platforms, the following are used:

- Secure data centers

- Biometric access control

- Collaboration with law enforcement agencies

- Financial Review Board audits

- Strict regulatory systems

These are physical security systems that ensure the banking infrastructure used in digital payments is protected.

The Role of Rigorous and Frugal Testing in Payment Reliability

Trustworthy P2P payment app development needs sophisticated testing techniques.

Venmo uses:

- Functional testing

- Performance testing for payment apps

- Load testing

- Regression testing

- Security testing

- API validation

Frugal testing recommended by buildnextech is risk-driven and automation-optimized. It prioritizes and maximizes coverage rather than wasting resources.

Frugal testing enhances scalability, compliance, and security for organizations providing custom P2P payment app development services.

The Future of Digital Payments and Venmo’s Role

The digital finance environment is rapidly developing at an unprecedented rate. As consumers increasingly turn to mobile apps for their daily transactions, the future of peer-to-peer payment apps such as Venmo will be shaped by innovation in artificial intelligence, blockchain technology, open banking standards, and secure cloud-based payment platform development.

The role of Venmo in this future is not merely that of a peer-to-peer payment app. Rather, through continuous investment in security architecture, transaction monitoring, PCI DSS compliance, and ISO 27001 standards, Venmo positions itself within the future of fintech. This is achieved through the use of artificial intelligence for fraud protection, the improvement of multi-factor authentication systems, and the improvement of User Experience to keep pace with the rapidly growing fintech industry.

Furthermore, as financial institutions upgrade their banking infrastructure and implement Open Banking standards, peer-to-peer payment apps such as Venmo must also keep pace with the evolving Legal and Regulatory Considerations. This is achieved through alignment with organizations such as the Federal Trade Commission, Federal Deposit Insurance Corporation, and Consumer Financial Protection Bureau.

Through innovation and compliance, the future of digital payments will be characterized by speed, intelligence, personalization, and security.

Digital Payments Trends

Some of the upcoming trends in payments include:

- Integration of Artificial Intelligence

- NFC technology with PoS terminals

- Adoption of Blockchain technology

- Launch of the Open Banking initiative

- Real-time settlements

Mobile Apps and social media app integrations are increasingly blurring the lines between social media accounts and digital finance.

The Future of Digital Banking

Future digital banking focuses on:

- Cloud Solutions

- Improved User Experience

- Secure payment gateways

- Open banking protocols

- Regulatory compliance

The fintech ecosystem will witness the adoption of decentralized and AI-driven infrastructure in the future.

The Role of Technology in Finance

The finance technology industry is always evolving in the following ways:

- Artificial intelligence

- Research studies in behavioral economics

- Experimental studies

- Sophisticated fraud modeling

- Automation of decision-making

The development of peer-to-peer payment applications will have to continue innovating based on global compliance standards for secure payments.

Best Practices for Using Venmo Safely

Although Venmo has been able to create effective security systems such as secure socket layer encryption, multi-factor authentication, transaction monitoring, and artificial intelligence-based fraud protection, it is also the duty of the users to make sure that their accounts are secure. Even the most secure P2P payment systems can be vulnerable if the users do not take the right security measures.

The security risks for the users include securing personal information such as Social Security numbers, OTP messages, and credit/debit card information, battling phishing attacks, and being careful about impersonator scams. The users can reduce the risks of fraud by turning on push notifications, checking the transaction history, and being mindful of potential security threats.

If the right security measures are taken on the website and the users take the right measures, peer-to-peer (P2P) payment systems such as Venmo can offer a secure online financial experience.

How to Set Up Venmo

- Download the app

- Link a bank account or a debit card.

- Complete KYC onboarding

- Enable two-factor authentication

- Activate biometric authentication

Never share Social Security numbers or OTP codes with unknown sources.

How to Use Venmo Effectively

- Verify recipient details

- Monitor transaction monitoring alerts.

- Avoid phishing websites

- Limit Social Feed visibility.

- Enable push notifications

Safest Money Transfer Apps

When choosing the safest money transfer app, evaluate:

- Security architecture

- PCI DSS compliance

- Fraud protection systems

- Regulatory alignment

- Transaction monitoring

Venmo, Cash App, Google Pay, and Apple Pay operate within structured compliance frameworks.

Conclusion

The emergence of peer-to-peer payment services has significantly changed the way people and businesses handle digital payments. As explained throughout this blog, the knowledge of what Venmo is, how peer-to-peer payment works, and how Venmo works is not as simple as it seems because there is a lot of complexity involved in providing seamless peer-to-peer money transfer services. Trustworthy digital payments require more than just simplicity and a successful business model.

The rising trend of digital payments has led to the increasing demand for Cloud Solutions, blockchain technology, open banking, and advanced transaction analysis. Frugal testing methods, with the assistance of buildnextech, ensure maximum performance with no overheads.

By embracing regulatory compliance, intelligent security, and comprehensive testing, Venmo is offering secure, scalable, and safe peer-to-peer (P2P) payment solutions in the rapidly evolving fintech future.

People Also Ask (FAQ)

Q1.What is Venmo?

Ans: Venmo is a mobile peer-to-peer payment service that facilitates instant digital money transfers.

Q2.How does Venmo work?

Ans: It is linked to a bank account or debit card, allows multi-factor authentication, encrypts data, and supports secure money transfers through payment gateways.

Q3.What are Venmo fees?

Ans: There are no fees for standard money transfers. However, Instant Transfers and some debit card transactions incur Transaction Fees.

Q4.What is P2P payment?

Ans: P2P Payment is a digital money transfer between individuals using peer-to-peer payment services.

Q5.What are the best practices for using Venmo safely?

Ans: Users should enable two-factor authentication, check transactions, avoid phishing websites, and safeguard sensitive data.