The rise of the Digital Rupee marks a pivotal moment in India’s fintech industry, combining CBDC technology with the promise of secure and scalable digital money solutions. As fintech companies and fintech startups accelerate innovation, the need for robust software testing and security testing becomes critical.

Ensuring the safety of UPI transactions, protecting against cyber threats, and validating performance through penetration testing in cyber security are vital. From fintech software to CBDC platforms, testing ensures reliability and trust in digital money transfer services. This blog examines how testing enhances CBDC scalability, strengthens fintech technology, and fosters confidence in UPI India payments.

Types of CBDC

- Retail CBDC (e₹‑R)

Retail CBDC is designed for the general public—individuals, small businesses, and merchants. It enables secure digital transactions for daily usage, such as peer-to-peer payments, merchant purchases, and utility bill payments, acting as a digital equivalent of physical cash.

- Wholesale CBDC (e₹‑W)

Financial institutions use wholesale CBDC for large-scale, high-value settlements. It improves efficiency in interbank transfers, government securities transactions, and cross-border remittances, offering near real-time clearing with reduced operational costs.

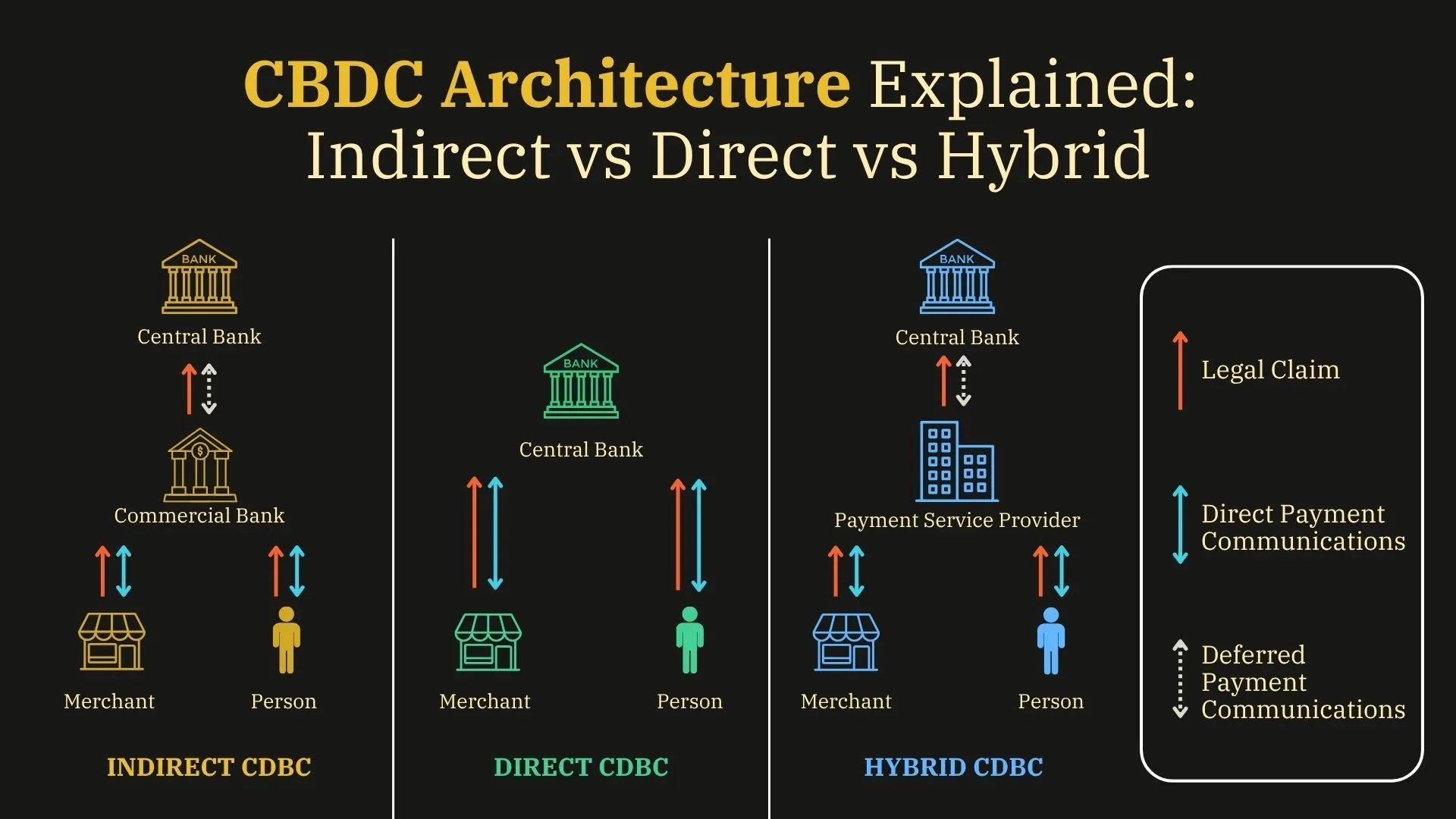

Models for CBDC Issuance: Direct, Indirect (Intermediary), and Hybrid

India’s CBDC system explores three distribution models:

- Direct: In the direct model, the Reserve Bank of India (RBI) issues and distributes the Digital Rupee directly to end-users, without involving intermediaries. This gives RBI full control over issuance, distribution, and user account management.

- Indirect: Under this model, commercial banks and licensed intermediaries manage user accounts and distribute CBDC on behalf of RBI. While the RBI issues the currency, intermediaries handle customer interaction, wallets, and KYC compliance.

- Hybrid: The hybrid approach allows intermediaries to manage front-end services like wallets and customer support, while RBI retains control over the core ledger. It ensures operational scalability without compromising centralized oversight and security.

💡 What’s next? Keep scrolling to find out:

🚀 Exploring the core features of India’s CBDC framework.

🚀 Understanding RBI’s purpose behind introducing the Digital Rupee.

🚀 Applying security, scalability, and functionality testing across layers.

🚀 Tackling blockchain tech, user interface, and privacy concerns.

🚀 RBI’s structured, tested strategy for seamless Digital Rupee rollout.

Introduction to India’s Digital Rupee and Its Core Features

India’s Digital Rupee, the country’s official Central Bank Digital Currency (CBDC), marks a major shift in how digital money is issued and managed. Backed by the Reserve Bank of India, it combines fintech innovation with secure design to provide a faster, more scalable, and transparent alternative to physical currency and traditional banking systems.

India’s Digital Rupee introduces a secure, government-backed digital currency designed for faster, transparent transactions. It enhances financial inclusion, supports UPI integration, reduces dependence on cash, and enables programmable, scalable solutions aligned with the nation’s growing fintech infrastructure.

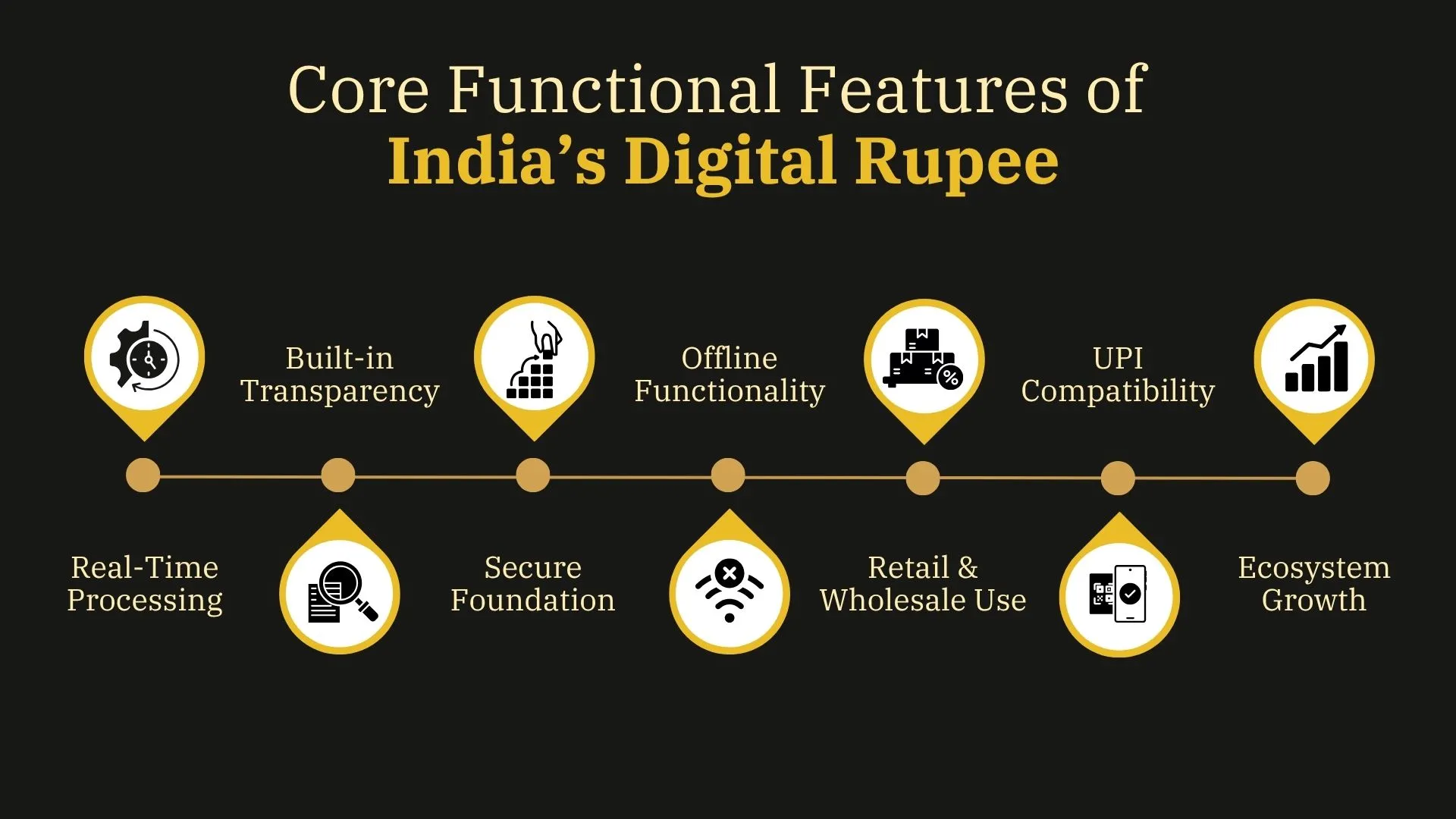

- Real-time processing: Enables seamless digital money transfer across platforms using UPI India payment systems.

- Built-in transparency: Every transaction is trackable, supporting trust across fintech software environments.

- Secure foundation: Developed using advanced software testing services to meet strict digital currency safety standards.

- Offline functionality: Enables digital transactions even without internet connectivity, ideal for remote or low-connectivity regions..

- Retail and wholesale use: Works for both consumer purchases and banking operations, unlike typical digital money stocks.

- UPI compatibility: Easily integrates with UPI pay frameworks, ensuring wide-scale acceptance.

- Ecosystem growth: Encourages fintech startups and top fintech companies to create digital tools around CBDC.

Objectives Behind Launching the Indian CBDC

The introduction of India’s Central Bank Digital Currency (CBDC) aligns with the government’s goal to modernize the financial ecosystem using secure, efficient, and inclusive digital payment tools. The CBDC aims to bridge the gap between physical cash and emerging fintech technology, offering a stable, regulated digital alternative for both urban and rural users.

- Financial inclusion: Empowers users with limited banking access through digital money transfer services.

- Reduced currency management costs: Eliminates printing and distribution costs associated with traditional cash.

- Support for fintech industry innovation: Encourages growth in fintech companies by offering a government-backed digital currency.

- Cross-border efficiency: Enhances speed and accuracy in international digital money transfer.

- Secure infrastructure: Integrates qa software testing to reduce risk and ensure consistent system behavior.

- Alternative to cryptocurrencies: Offers the benefits of digital money without the volatility of private tokens.

- Boost digital economy adoption: Strengthens the digital foundation supporting fintech startups and platforms.

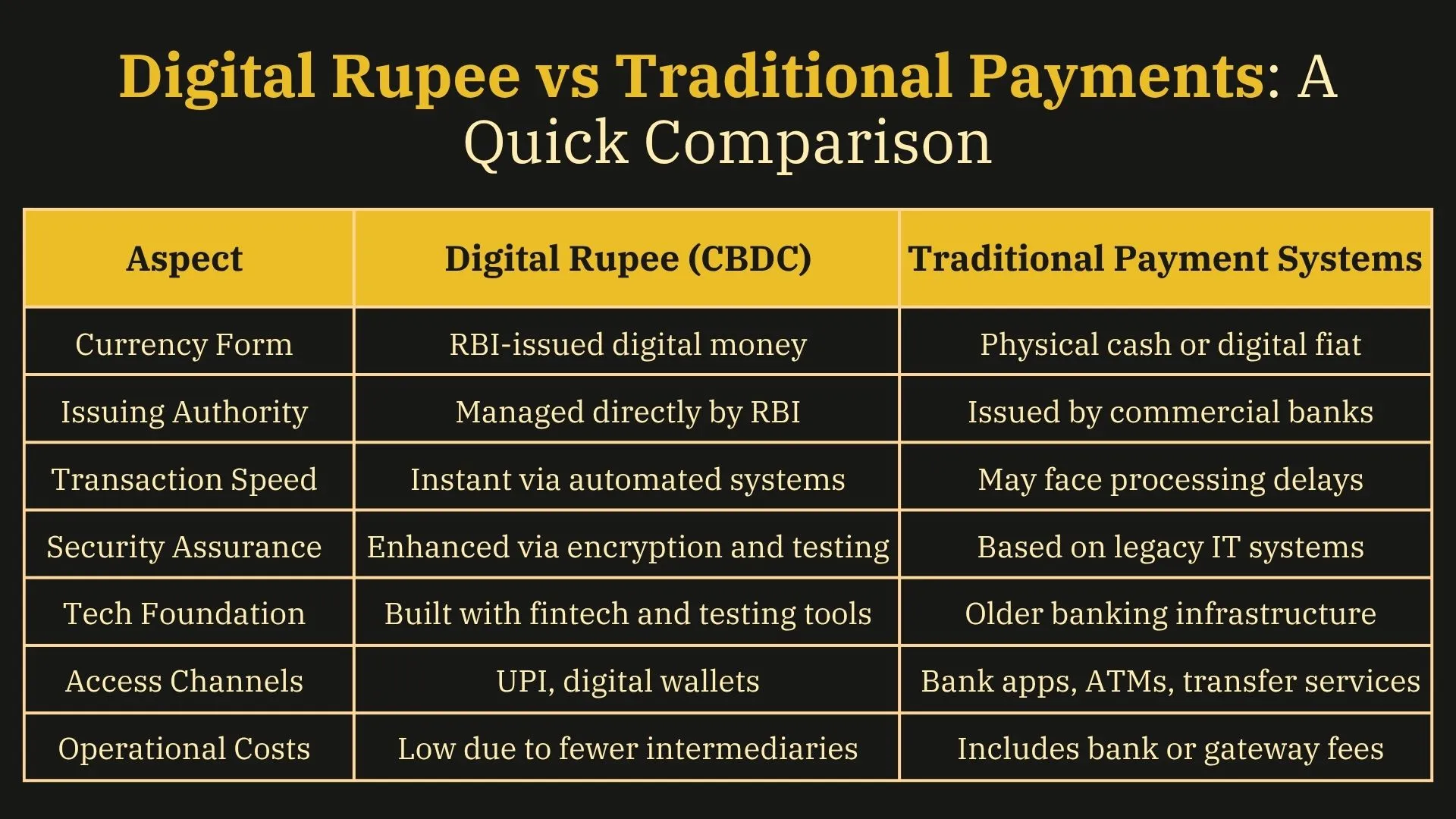

Difference Between Digital Rupee and Traditional Payment Systems

India’s digital money ecosystem is evolving rapidly with the introduction of the CBDC. Unlike traditional systems like UPI India payment or NEFT, the CBDC platform brings in direct, programmable currency supported by advanced fintech technology and secure software testing.

Types of Software Testing Applied in Digital Rupee Development

India’s Digital Rupee requires a high level of testing precision due to its role in secure, large-scale financial infrastructures. Various software testing types are adopted to validate functionality, security, and performance of this digital central bank money across complex CBDC system designs.

- Functional Testing: Validates core transaction workflows across digital wallets, Aadhaar-enabled payments, and token-based transfers. It ensures every user journey from onboarding to transaction confirmation functions as intended under various scenarios.

- Performance Testing: Assesses the system's ability to handle high transaction volumes, particularly during peak usage of Retail Payments or when operating in offline modes. It identifies latency, throughput, and response-time bottlenecks.

- Security Testing: Identifies vulnerabilities in digital identity frameworks, cryptographic implementations, and privacy-preserving technologies. It helps secure user data and prevent tampering, fraud, or unauthorized access across the CBDC infrastructure.

- Integration Testing: Verifies how well different modules, such as Speed Wallets, overlay networks, QR-based payments, and token issuance systems, interact with each other to support seamless end-to-end transactions. Uniqode's QR code Generator also helps streamline secure and scalable QR payment experiences across multiple platforms.

- Compliance Testing: Ensures that the entire CBDC system adheres to national and international regulatory standards like ISO 27001, data protection laws, and RBI security protocols for digital finance.

- Usability Testing: Focuses on user interface design and ease of navigation, especially for semi-digital or rural users. It supports digital literacy goals while building trust in Peer-to-Peer and Merchant Payments.

Security Testing Measures to Safeguard the CBDC Infrastructure

Securing the CBDC infrastructure is to prevent breaches, ensure privacy, and maintain trust in India’s Digital Rupee. Robust security testing practices are applied to identify potential risks and reinforce the integrity of the system architecture supporting digital central bank money.

- Vulnerability assessment: Detects flaws in blockchain frameworks, such as Corda DLT and Hyperledger Fabric, used in private blockchain setups.

- Penetration testing: Simulates attacks on the CBDC system design to uncover risks in user privacy, cryptographic protocols, and smart contracts.

- Access control verification: Validates the token-based access model and hybrid access model within the centralized ledger.

- Encryption testing: Assesses homomorphic encryption and zero-knowledge proofs to protect financial stability and sensitive digital onboarding data.

- Authentication checks: Ensures secure wallet issuance and QR code access in Speed wallet apps.

- Compliance evaluation: Confirms Regulatory Compliance against standards for digital cash and cross-border transactions.

Scalability Testing for Handling High Transaction Volumes

The success of India’s Digital Rupee depends heavily on its ability to manage high transaction volumes across diverse use cases. Scalability testing ensures that the CBDC infrastructure can maintain performance during peak loads without delays or failures.

- Load simulation tools: Stress test the CBDC platform under varying transaction workflows and peak user demand using digital wallet integration scenarios.

- Performance metrics tracking: Monitors system responsiveness, throughput, and latency across the unified lending interface and India Stack-based services.

- Infrastructure elasticity testing: Validates the CBDC system’s adaptability within digital public infrastructure, including retail payments and interbank settlements.

- Network traffic validation: Evaluates overlay networks and consortium blockchain capacity for cross-border payments.

- Node distribution analysis: Assesses how permissioned blockchain networks scale with user onboarding and QR code usage.

- System upgrade checks: Ensures real-time scalability with peer-to-peer transactions, offline payments, and artificial intelligence-driven enhancements.

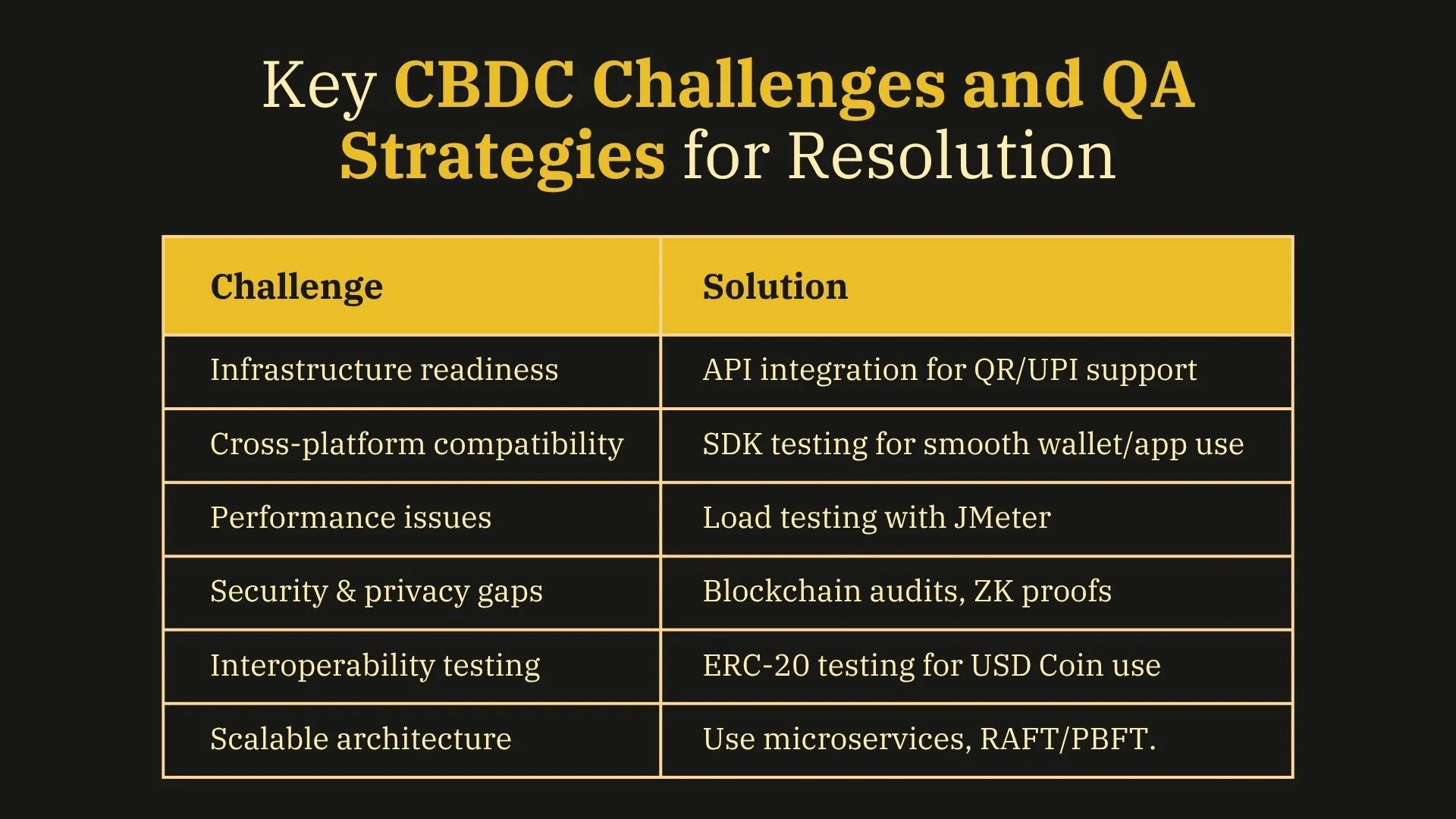

Challenges in Testing and Deploying the Digital Rupee

Testing and deploying the Digital Rupee within India’s financial ecosystem involves overcoming complex obstacles that touch on infrastructure, regulatory frameworks, and evolving user expectations. Here are the critical challenges:

- Infrastructure readiness: Integrating with legacy systems of fintech companies while supporting modern features like QR codes and UPI payments.

- Cross-platform compatibility: Ensuring the digital currency operates smoothly across cryptocurrency wallets and digital wallet apps.

- Real-time performance issues: Handling high-volume transactions to meet best digital money standards in peak hours.

- Security and privacy gaps: Addressing security penetration testing for smart contracts and decentralised nature without compromising user privacy.

- Interoperability testing: Validating smooth transitions between digital rupee and USD Coin for cross-border use cases.

- Scalable architecture: Deploying under a two-tier architecture model while managing consensus mechanisms.

Final Thoughts on India’s Digital Rupee and Its Tested Path to Secure Adoption

The Digital Rupee marks a pivotal shift toward a cashless economy, driven by innovations in blockchain technology, Big Data, and secure User Interface design. As India advances its account-based access model, addressing security concerns and integrating notary service mechanisms becomes essential. For every fintech company, understanding what CBDC stands for is key to adapting to this evolution and enabling users to confidently buy digital money in the future.

This shift marks more than just a technological upgrade; it reflects India’s evolving approach to inclusive, efficient digital finance. As the Digital Rupee ecosystem matures, continued focus on performance, resilience, and seamless user experience will define its success, offering a blueprint for future-ready monetary systems in a rapidly digitizing world.

With expert support from Frugal Testing, including functional testing services, bug testing services, and load testing services, organizations can ensure performance at scale. Recognized among top software testing companies, Frugal’s AI-driven test automation services and Selenium automation testing service streamline quality assurance for SaaS application testing and enterprise solutions.

People Also Ask

1. Which banks are currently involved in the Digital Rupee pilot program?

Major banks like SBI, ICICI Bank, HDFC Bank, Yes Bank, and IDFC First Bank are part of the RBI's Digital Rupee pilot program.

2. Which banks are currently involved in the Digital Rupee pilot program?

Banks like SBI, HDFC, ICICI, Kotak Mahindra, IDFC First, and Yes Bank are actively participating in the pilot rollout.

3. How does RBI ensure the privacy of Digital Rupee transactions?

RBI adopts a Privacy and Security Layer with account-based access and encryption to protect transaction data and user identity.

4. What is the future roadmap for the Digital Rupee in India?

The roadmap includes nationwide rollout, offline payment support, cross-border capabilities, and deep integration with UPI and digital wallets.

5. How can individuals access and use the Digital Rupee?

Users can access the Digital Rupee through banking apps or dedicated CBDC wallets and make payments via QR codes or UPI integration.