That tempting "Pay in 4 easy installments" button is everywhere, from your favorite clothing retailer to the checkout page for a new mattress. Buy Now, Pay Later (BNPL) has exploded into a multi-billion dollar industry, offering unparalleled convenience. But as you use these popular Buy now, pay later services, a crucial question arises: Is Buy Now, Pay Later safe? The convenience is clear, but the potential impact on your financial health is often buried in the fine print.

This comprehensive guide is designed for both consumers and business leaders trying to navigate the fintech landscape. We'll dissect the BNPL model, weigh its rewards against its inherent risks, and explore the critical connection between BNPL use and your credit score. You'll walk away with actionable strategies to use these services smartly and a clear understanding of the evolving regulatory environment. Let's dive in.

💵 From this blog, you will understand

📌 What is Buy Now, Pay Later?

📌 The primary dangers involve accumulating debt through multiple payment plans

📌 Credit score impact on Buy Now Pay Later

📌 How to Assess Interest Rate?

What Is Buy Now, Pay Later?

Buy Now, Pay Later lets consumers buy products or services right away. They pay over time in several installments. It is a type of short-term, point-of-sale financing. Think of it as a modern, digitized version of the classic layaway plan, but you get the item upfront. Unlike traditional credit cards, many BNPL plans are interest-free if you pay on time, which is a major part of their appeal.

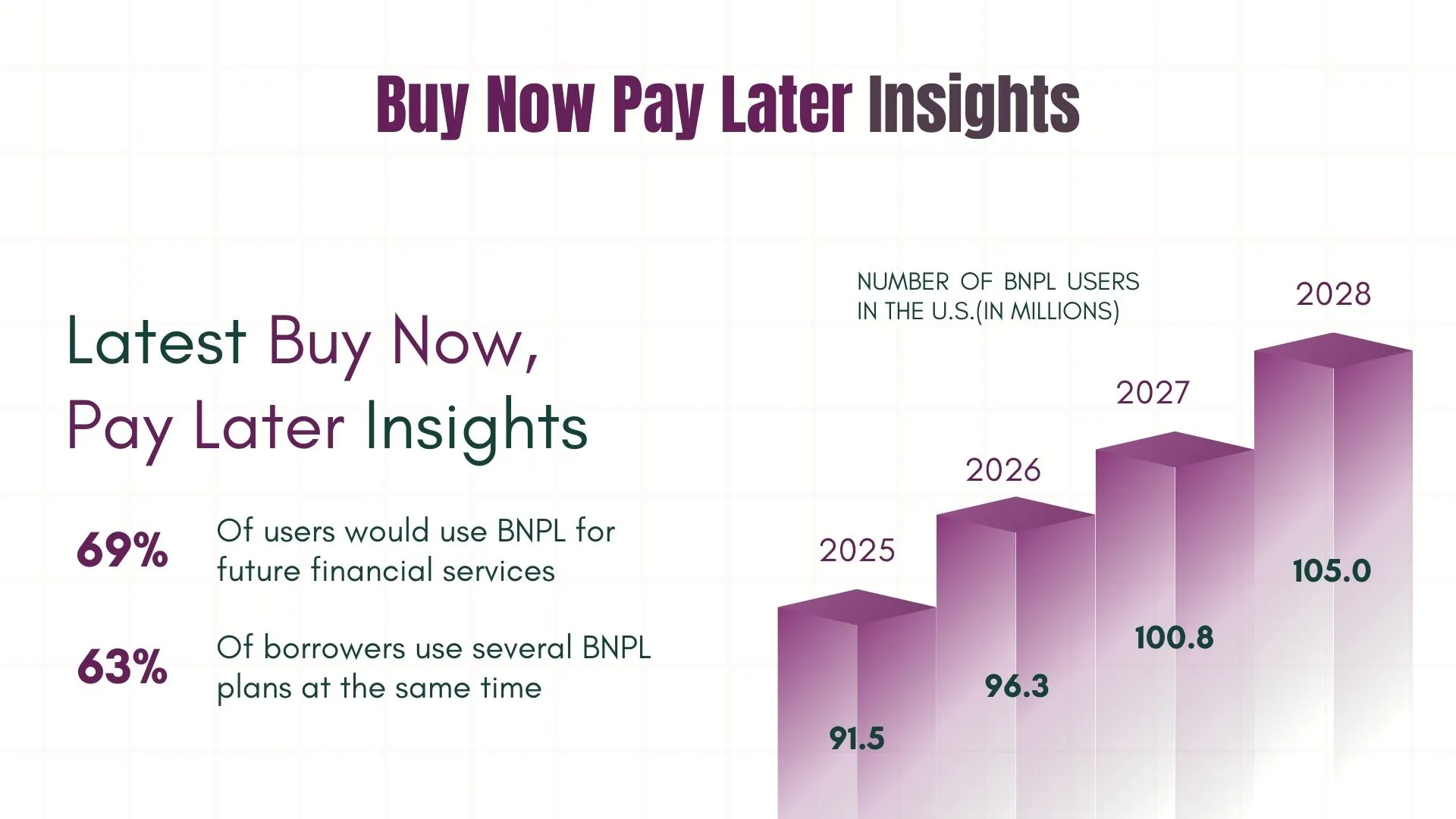

The growth of BNPL has been nothing short of meteoric. The industry is transforming the e-commerce and retail landscape by lowering the barrier to purchase for consumers. According to projections from Statista, the global BNPL transaction value is expected to surge past $680 billion by 2025 (Source: Statista, 2023).

This explosive trend is driven by younger consumers who are often wary of traditional credit card debt and appreciate the transparent, fixed payment schedules that BNPL offers. For merchants, offering BNPL can lead to higher conversion rates and larger average order values, making it a powerful tool in a competitive market. This fast growth has caught the attention of consumer protection agencies. They are now looking into possible harm to consumers.

💡 Key Takeaways

1. BNPL splits purchases into smaller, interest-free payments.

2. It’s convenient but offers fewer protections than credit cards.

3. Late or missed payments can hurt your credit score.

How BNPL Works for Consumers & Lenders

Understanding the mechanics of BNPL is key to assessing its safety. The process looks simple at first. But the financial model involves three parties: you (the consumer), the merchant, and the BNPL provider like Klarna, Afterpay, or Affirm.

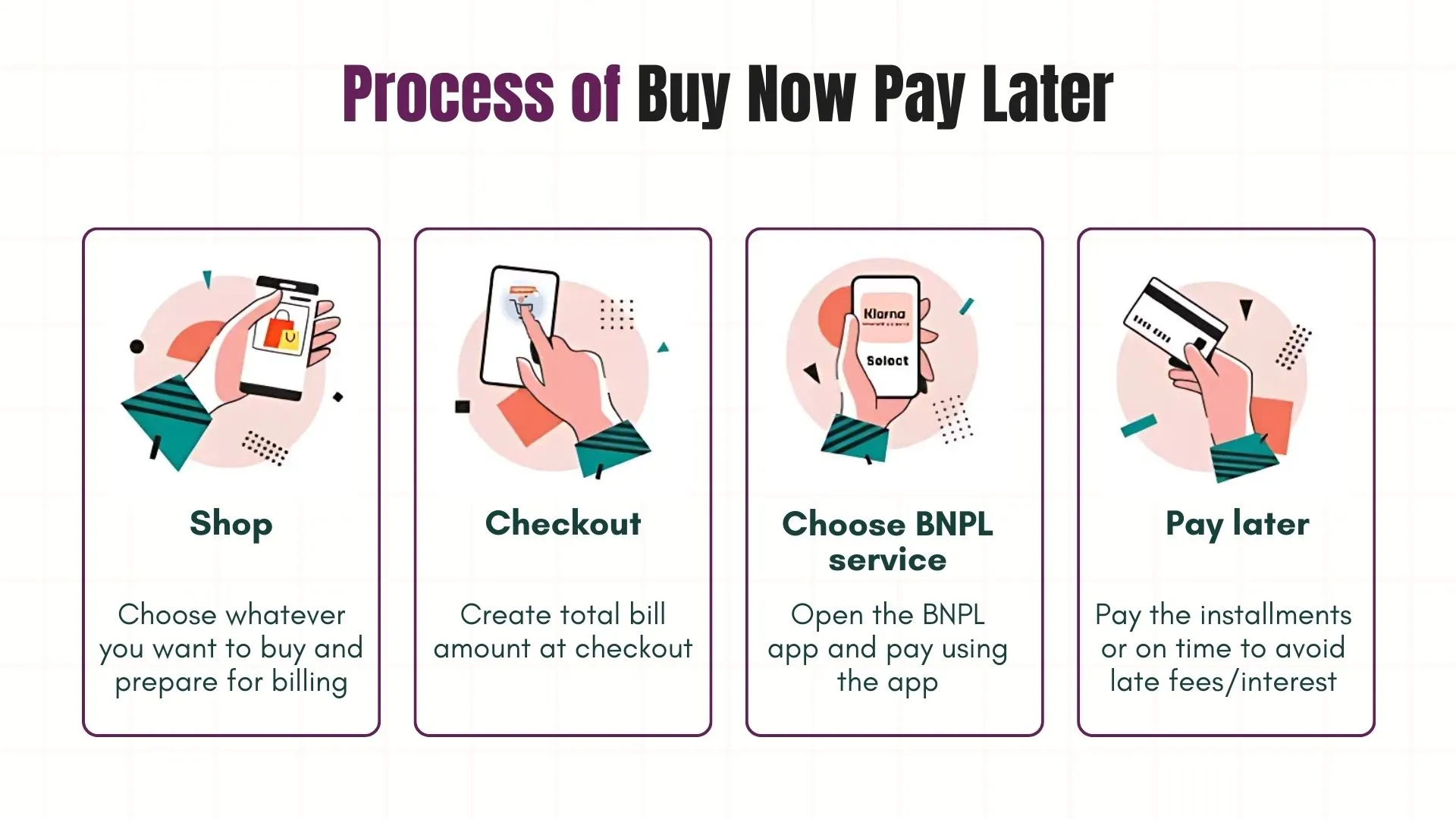

Consumer Checkout & Repayment Flow

For you, the shopper, the journey is designed to be as frictionless as possible. It typically follows these steps:

- Selection at Checkout: You're ready to buy and proceed to the payment page. Alongside credit cards and PayPal, you see an option like "Pay with Affirm" or "4 interest-free payments with Klarna."

- Instant Decision: After selecting the BNPL option, you'll be prompted to enter a few personal details (name, address, date of birth, and sometimes the last four digits of your SSN). The BNPL provider runs a quick, automated assessment, usually a soft credit check, that doesn't harm your score and gives you an instant approval decision.

- Down Payment: For most "Pay in 4" plans, you'll make the first payment (typically 25% of the total purchase price) immediately at the time of purchase.

- Automated Repayments: The remaining installments, often structured as bi-weekly or monthly payments, are then automatically charged to your linked debit card, credit card, or bank account until the balance is paid in full.

As shown in the above image the BNPL process for consumers is designed for speed and simplicity at the point of sale.

Lender-Merchant Revenue Dynamics

So if many plans are "interest-free" for consumers, how do BNPL companies make money? Their revenue model is twofold, relying on both the merchant and, in some cases, the consumer.

- Merchant Fees: The primary revenue stream for BNPL providers comes from the retailers. When a customer uses a BNPL service, the merchant pays the provider a percentage of the purchase price. This fee typically ranges from 2% to 8%, which is higher than standard credit card processing fees (Source: The Motley Fool, 2024).

- Why would merchants agree to this?

Because studies show that offering BNPL can increase customer conversion rates by 20-30% and boost the average ticket size. - Consumer Fees & Interest: The second revenue stream comes directly from consumers. This includes:

- Late Fees: If you miss an automatic payment, you'll likely be charged a fixed late fee or a percentage of the installment amount. These fees can add up quickly.

- Interest on Longer-Term Plans: While the popular "Pay in 4" model is often interest-free, many BNPL providers also offer longer-term financing for larger purchases (e.g., 6, 12, or 24 months). These plans almost always charge interest, with high interest rates and Annual Percentage Rates (APRs) that can sometimes be comparable to or even exceed those of credit cards.

This dual-revenue structure is a key reason why the system thrives, but it's also where the risks for consumers begin to emerge.

What Are the Rewards and Risks of BNPL?

BNPL is a financial tool, and like any tool, it can be incredibly helpful when used correctly or damaging when misused. Its safety depends entirely on your understanding of the trade-offs and your own financial discipline.Cash-flow pressure affects businesses and households alike. For consumers, one area worth understanding is debt relief, a space where companies like Freedom Debt Relief work with people every day.

The Rewards:

- Increased Affordability: BNPL breaks down a large purchase into manageable chunks, making expensive items feel more accessible without having to save up for months.

- Convenience and Speed: The approval process is nearly instantaneous and integrated directly into the checkout flow.

- Interest-Free Financing: The flagship "Pay in 4" models offer a way to borrow money for free, a compelling alternative to interest-bearing credit cards.

- Simple Approval: BNPL services often use soft credit checks, making them accessible to consumers with thin or poor credit histories who might not qualify for a traditional credit card.

The Risks:

- Encourages Overspending: The "pain of paying" is psychologically reduced when a $400 purchase is framed as "4 easy payments of $100." This can lead to impulse buys and budget overruns.

- Risk of "Loan Stacking": It's easy to lose track of multiple BNPL plans across different retailers. Managing several payment schedules simultaneously increases the risk of a missed payment.

- Steep Late Fees: While a single late fee might seem small (e.g., $7-$10), they can accumulate. Some providers may continue to charge fees for each missed payment.

- The Debt Spiral: According to a 2022 report from the Consumer Financial Protection Bureau (CFPB), a growing number of BNPL users are exhibiting signs of financial distress, carrying debt from multiple providers and struggling to keep up.

- Lack of Regulatory Protection: BNPL loans are not currently protected by the same federal consumer protection laws that apply to credit cards, such as standardized fee disclosures and dispute resolution rights.

Can BNPL Harm Your Credit Score?

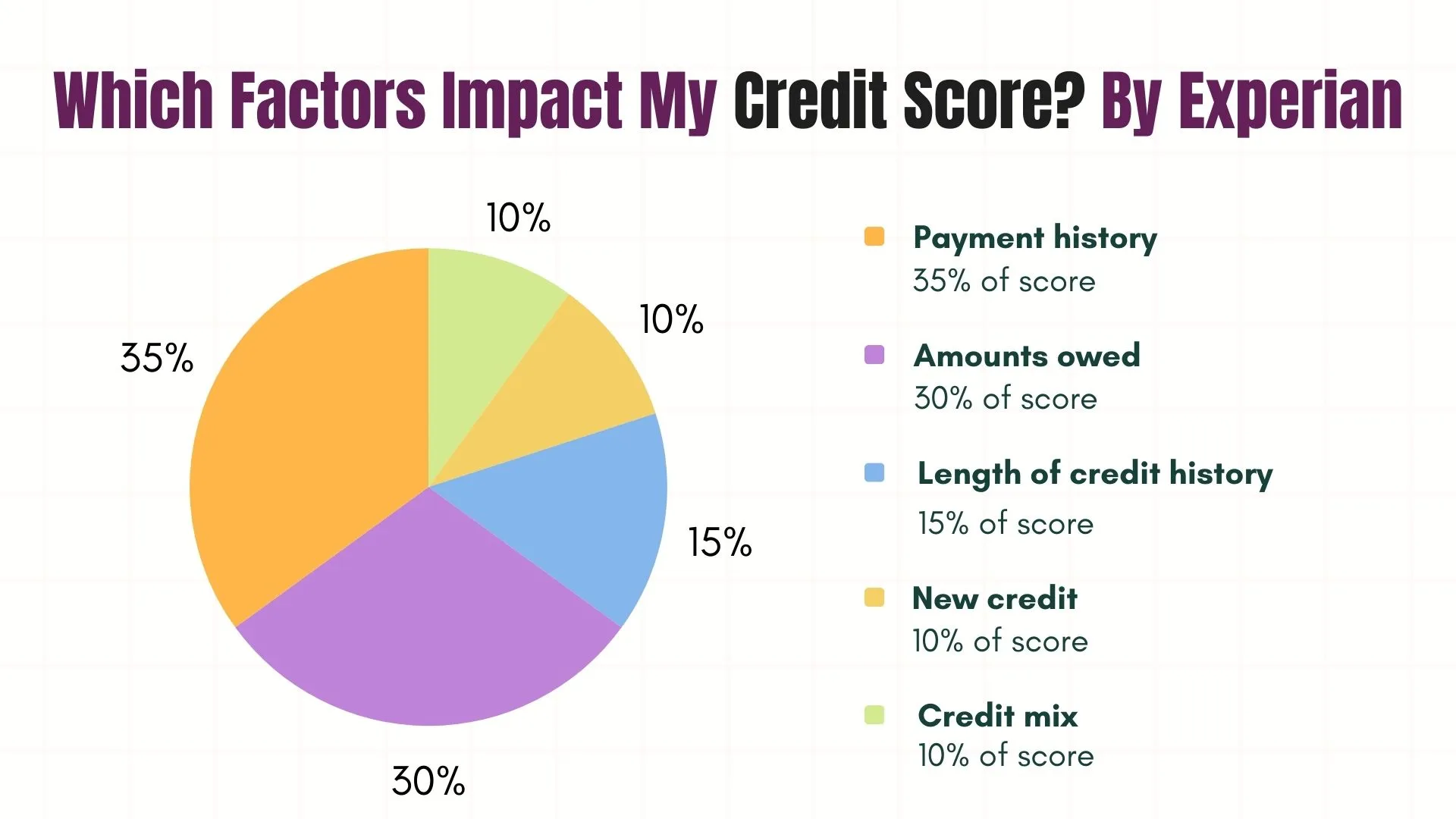

Yes, it can. While historically BNPL providers didn't report on-time payments, most will report missed payments and defaults to credit bureaus. Now, major bureaus like Experian, Equifax, and TransUnion are actively incorporating all BNPL payment data, meaning on-time payments can help your score, but late payments will certainly hurt it.

Initially, a key selling point of BNPL was that it operated outside the traditional credit reporting system. You could make your payments on time, but it wouldn't help build your credit history. Conversely, if you defaulted, the provider might send your account to a collections agency, which would then report it and damage your score.

However, the landscape is shifting rapidly. The major credit bureaus have recognized the significance of BNPL data.

- Experian has "Experian Boost," which allows consumers to voluntarily add BNPL payment history to their credit file.

- Equifax and TransUnion have also developed specific frameworks to accept and display BNPL data, treating it as a short-term installment loan.

What this means for you: Using BNPL is no longer a credit-invisible activity. A consistent record of on-time payments could potentially help build a positive credit history, especially for those with limited credit. The downside is worse. Now, a single missed payment is more likely to be reported. This can lower your credit score. It can also make it harder to get credit like a car loan or mortgage.

The impact of these BNPL services on your financial record is now more direct. A single missed payment is now more likely than ever to be reported on your credit report, which can lower your credit scores. This negative mark can directly impact your FICO score, as payment history is the single most important factor in its calculation. Lenders frequently use the FICO credit score to determine creditworthiness, so a drop can have long-term consequences.

Ethical Design & Consumer Protection in BNPL

The meteoric rise of BNPL has largely outpaced regulation. Unlike the credit card industry, which is governed by decades-old laws like the Truth in Lending Act (TILA), the BNPL space has been described as a "regulatory gray area." This raises significant questions about ethical design and the need for robust consumer protections.

One of the core ethical debates centers on the concept of "positive and negative friction." Traditional loan applications have built-in "friction" - paperwork, credit checks, a waiting period that forces consumers to pause and consider the debt they are about to take on. BNPL is designed to be frictionless, which, while convenient, removes these moments of reflection and can facilitate impulsive over-borrowing.

The Consumer Financial Protection Bureau (CFPB) has taken a keen interest in the industry. Their research has highlighted several key areas of concern (Source: CFPB Report, 2023):

- Inconsistent Disclosures: The terms, fees, variable interest rates, and consequences of missing a payment are not always presented clearly and uniformly across different providers.

- Lack of Dispute Resolution Rights: Consumers who use BNPL and have an issue with a product (e.g., it never arrives or is defective) do not have the same legal rights to withhold payment as they do with credit cards.

- Data Harvesting: BNPL apps collect vast amounts of user data, raising concerns about how this information is used for marketing and product development.

So, are regulators trying to shut down BNPL?

"Not at all. The goal isn't to eliminate BNPL, but to ensure it operates within a framework that is fair and transparent for consumers. Regulators in the U.S., U.K., and Australia are all moving toward rules that would treat many BNPL products more like traditional credit, requiring clearer disclosures, affordability checks, and access to official complaint channels."

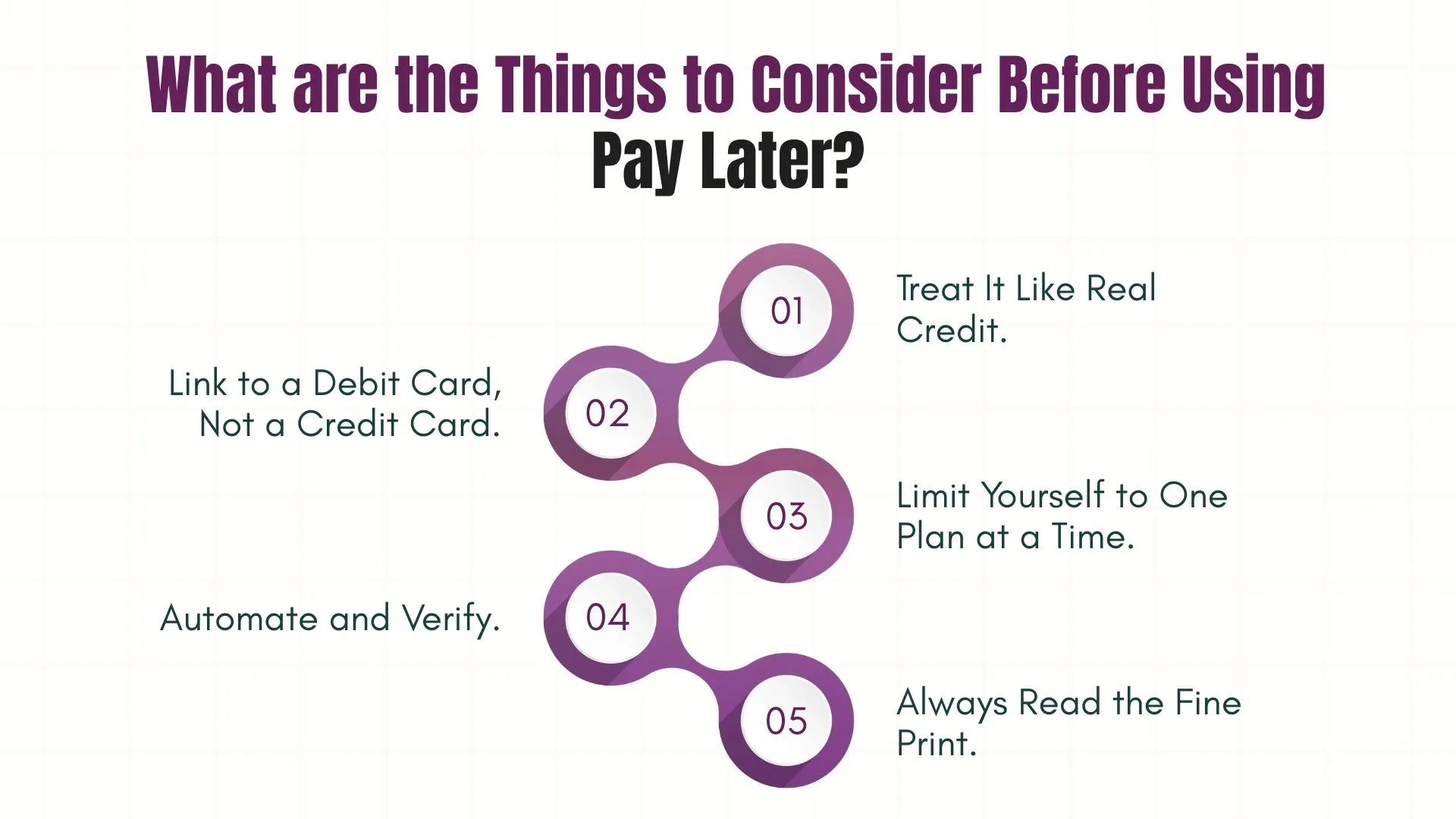

Pro Tips for Smart BNPL Use

BNPL can be a safe and effective financial tool if you approach it with a clear strategy. Here are five pro tips to protect your financial well-being.

- Treat it like real credit - If you wouldn’t feel okay putting the full amount on your credit card today, don’t us-e BNPL. It’s still debt, just presented differently.

- Link to a debit card - Avoid adding debt on top of debt. Linking BNPL to a credit card risks late fees plus interest charges on your card.

- Limit to one plan at a time - Multiple BNPL plans can quickly spiral. Clear one before starting another.

- Automate and monitor - Set up autopay to avoid missed payments, but check your balance a day or two before to prevent overdraft fees.

- Read the fine print - Know the late fees, interest rates for longer terms, and return policies before committing.

Pro Tip: Use a calendar app or a dedicated budgeting tool to set reminders for your BNPL payment dates. Treating it with the same seriousness as a rent or utility payment is key to staying on track.

Why you Should Consider Software Testing for BNPL Payments

Thorough software testing for your Buy Now, Pay Later (BNPL) integration is crucial to prevent lost sales, protect your brand, and ensure a secure customer experience. A flawed payment process directly impacts your bottom line and customer trust.

Here’s why you must prioritize it:

- To Protect Revenue & Trust: Bugs at checkout cause failed transactions, leading directly to lost sales. A smooth payment process builds confidence in your brand.

- To Guarantee a Seamless Experience: The appeal of BNPL is its convenience. Testing ensures the entire payment journey is fast and frictionless, meeting customer expectations.

- To Mitigate Security & Compliance Risks: Handling payment data is a major responsibility. Testing helps secure sensitive customer information against breaches and ensures you meet financial and data privacy standards.

- To Handle Real-World Complexity: BNPL involves tricky scenarios. Rigorous testing for edge cases like partial refunds, failed installments, and cart modifications prevents customer frustration and operational problems.

Looking for a QA Partner?

This is precisely where a dedicated QA partner like Frugal Testing provides critical value. Recognizing the unique challenges of the rapidly evolving Indian and global fintech landscape.

Conclusion & Next Steps for Stakeholders

So, is Buy Now, Pay Later safe? The answer is a qualified yes - but only when used with caution, discipline, and a full understanding of the risks. BNPL is not inherently good or bad; it is a powerful financial tool that offers flexibility and convenience. For consumers, its safety is directly proportional to their own financial literacy and self-control. Overspending, stacking multiple loans, and missing payments can quickly turn a convenient tool into a debt trap, with real consequences for your credit score.

Merchants, fintech providers, and regulators must focus more on ethical design. They must also protect consumers. As the industry grows, companies must use standard disclosures. They must also do responsible lending checks. Clear dispute resolution processes are needed. These steps will help the industry grow well and keep consumer trust.

Frequently Asked Questions

👉Is Paylater a loan?

Yes, definitely. "Paylater" or Buy Now, Pay Later is a form of point-of-sale installment loan. Even if it's interest-free, you are borrowing money that you are legally obligated to repay over a set period.

👉How does Amazon pay work?

Amazon Pay is a digital wallet and online payment processing service, similar to PayPal. It allows you to use the payment methods already stored in your Amazon account to pay for goods on third-party websites.

👉Will Afterpay do a credit check?

Yes, Afterpay performs a "soft" credit check when you sign up. A soft check does not impact your credit score and is not visible to other lenders.

👉How does Apple pay work?

Apple Pay is a mobile payment and digital wallet service. It lets users pay in person, in iOS apps, and on the web using a securely stored credit or debit card.

👉What does the 15-3 rule for credit score?

It is a popular financial planning tip for managing debt:

1. Invest 15% of pre-tax income for retirement.

2. Build a 3-month emergency fund.

3. Then, tackle high-interest debt - without letting BNPL affect these priorities.