.webp)

Financial transactions have shifted dramatically from online banking portals to digital wallets, POS systems, and QR code payments. Consumers expect instant, frictionless experiences. Behind the scenes, however, ensuring that every transaction remains secure is a complex orchestration of security protocols, encryption methods, multi-factor authentication, and real-time fraud detection.

One foundational yet often underappreciated element in India’s digital payment architecture is the Indian Financial System Code (IFSC). While many users simply copy and paste this 11-character code when sending money, IFSC codes are a linchpin in preventing misrouting, fraud, and unauthorized access integral to the “security chain” of Financial Services and fintech solutions.

In this guide, packed with industry best practices, code snippets, real-world examples, and insight into application security testing and software testing services, we’ll explore:

💡Insights

📌 What IFSC codes are and why they matter?

📌 How they secure NEFT, RTGS, and IMPS transfers?

📌 Best practices, common errors, and regulatory mandates

📌 IFSC comparison with IBAN and SWIFT

📌 The future of IFSC in India’s Digital Transformation

Along the way, we'll weave in topics like fintech, digital payment gateway, web application security testing, and more.

What Are IFSC Codes and Why Do They Matter in Digital Payment Security?

The IFSC (Indian Financial System Code) is an alphanumeric code of 11 characters that uniquely identifies every bank branch participating in India’s electronic payment systems: NEFT, RTGS, and IMPS.

Why IFSC Codes Matter

- Accurate Routing & Addressing

In a digital payment system or digital payment app, the IFSC ensures funds are directed to the exact branch. Mistyping even one character can send money to an unintended location - or cause a payment to fail. - Automated Verification & Fraud Reduction

Modern fintech companies embed IFSC validation into their digital payment gateway integrations. This instantaneous check prevents phishing attempts, SQL injection, and malformed inputs from progressing beyond the front-end. - Audit Trail & Reconciliation

Every NEFT, RTGS, or IMPS transaction logs the IFSC. This is crucial for back-office software testing life cycle audits, reconciliation, and dispute resolution. - Integration with Multi-Factor Authentication

Online banking platforms often tie IFSC validation with two-factor authentication (2FA) or multi-factor authentication (MFA). If the IFSC fails validation, the MFA step is halted, thwarting unauthorized attempts.

How to Find Your IFSC Code and Initiate a Bank Transfer

To initiate a bank transfer follow the below steps:

- Step1

Get the IFSC: Check your cheque’s top-left, passbook first page, bank’s website, RBI directory, or an IFSC-lookup app. - Step 2

Log in: Access your bank’s net-banking or mobile app. - Step 3

Start Transfer: Choose NEFT/RTGS/IMPS. - Step 4

Enter Details: Add beneficiary name, account number, and IFSC. - Step 5

Set Amount: Specify the sum to send. - Step 6

Confirm: Review, submit, and authenticate with OTP/password.

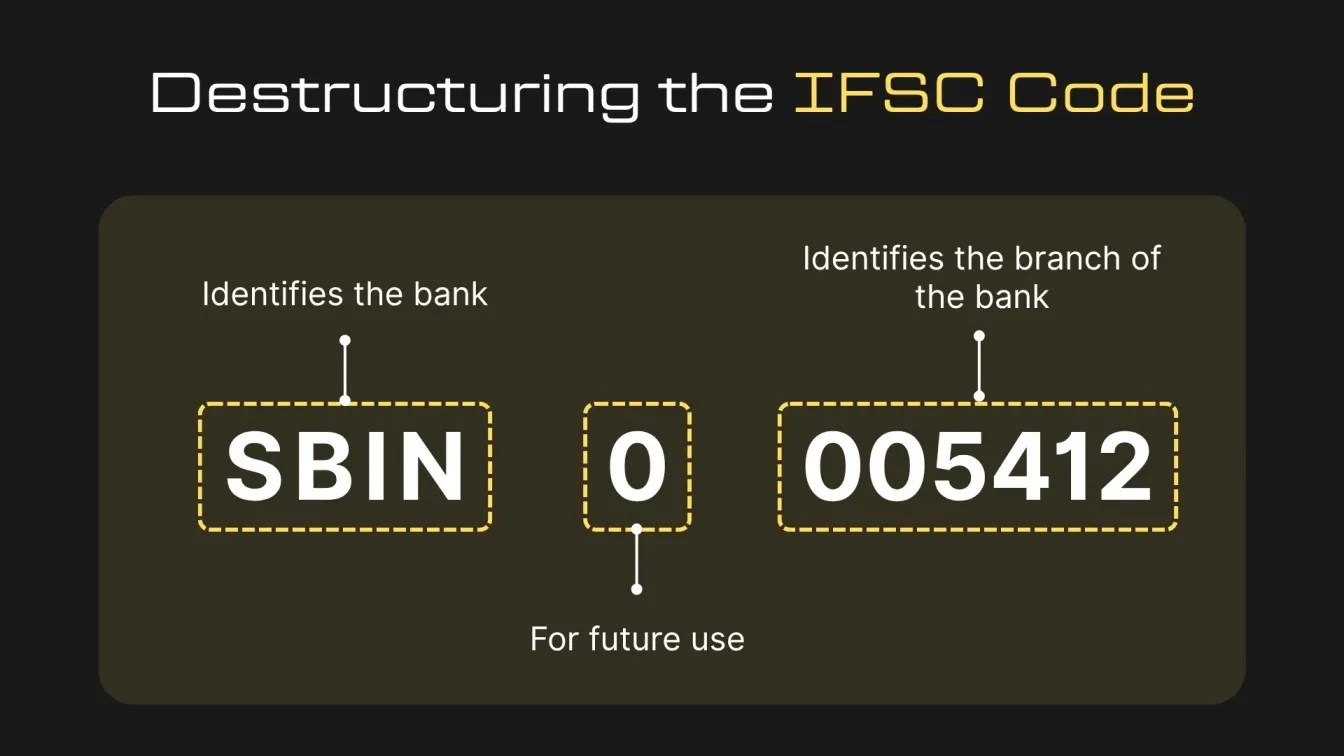

How Is an IFSC Code Structured and What Does Each Segment Signify?

A standardized 11-character format, an IFSC code’s three parts - bank prefix, reserved zero, and branch suffix - ensure precise routing and validation. A typical IFSC code looks like:

By enforcing a fixed format, IFSC codes prevent ambiguous entries and simplify software testing, including automated software testing and user testing software used by software testing companies to validate data input flows.

What are the Use Cases of IFSC Code in the Digital Age for Secure Banking Transactions?

An IFSC code uniquely identifies a bank branch for electronic transfers, enhancing security measures, streamlining financial transactions, and enabling remote banking in the era of Digital Transformation:

- Easy Online Transfers

Just enter the recipient’s account number and IFSC in your net-banking or mobile app to send money via NEFT, RTGS, or IMPS. - Improved Safety

By matching funds to the correct branch, an invalid IFSC stops the transaction rather than misdirecting your payment. - Fraud Prevention

Every branch’s unique code makes it simple to verify bank details, sharply reducing the risk of fraudulent transfers.

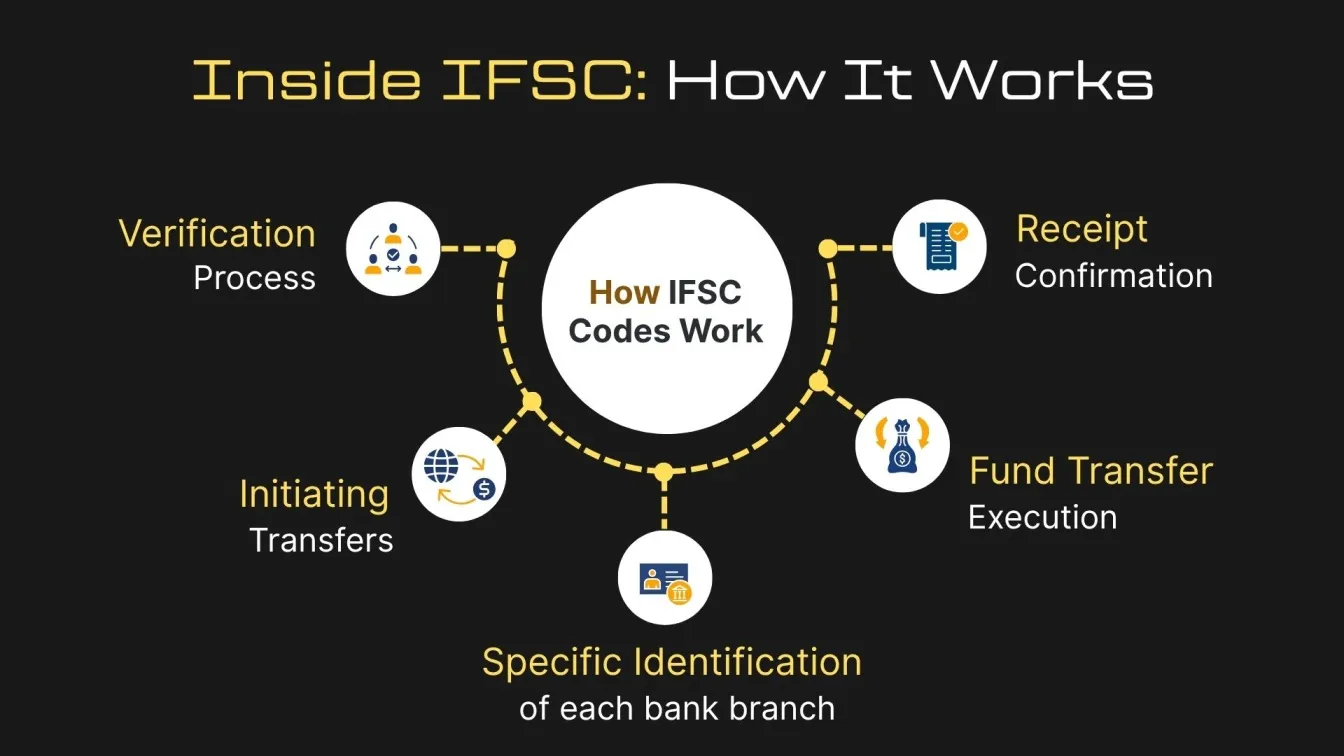

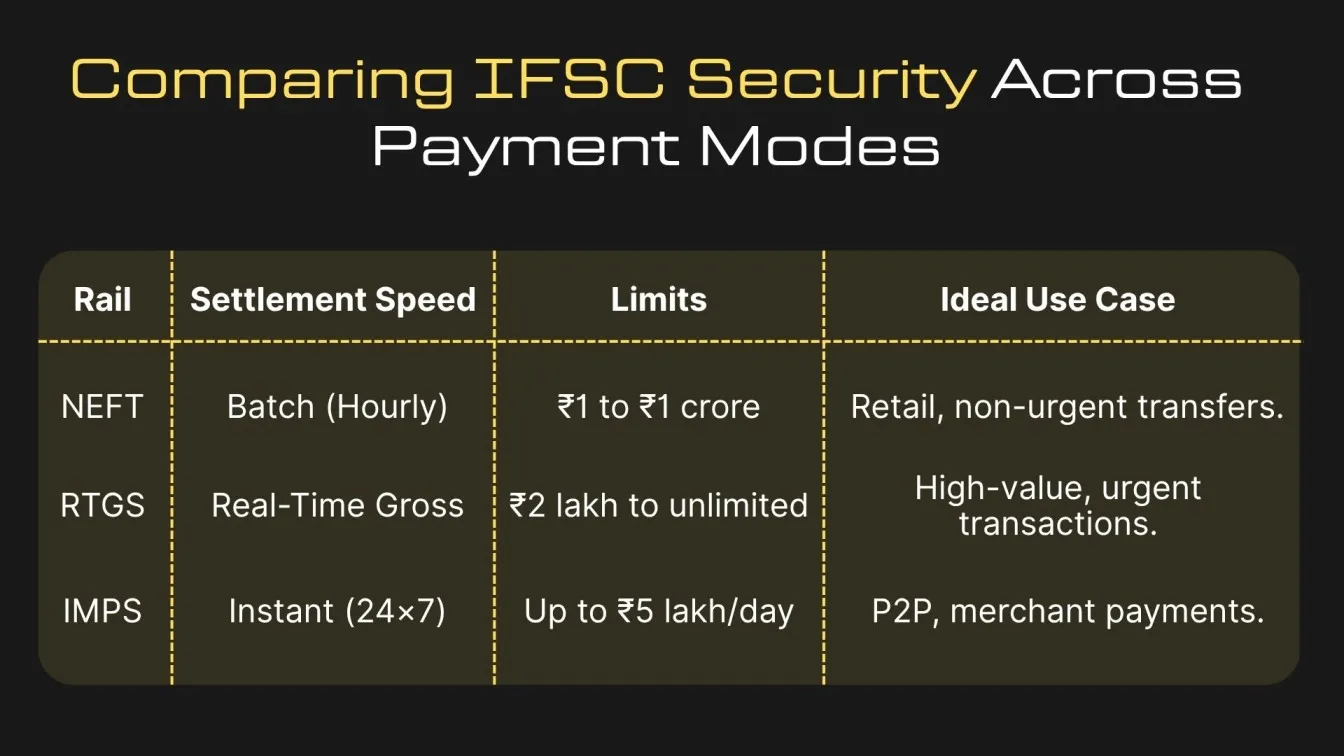

How Do IFSC Codes Ensure Secure Electronic Fund Transfers via NEFT, RTGS & IMPS?

India’s three primary electronic payment rails - NEFT, RTGS, and IMPS - each leverage IFSC codes to ensure secure protocols and seamless operations.

1. NEFT Security with IFSC

- Batch Validation: Before each batch, sending banks validate IFSC codes against the RBI directory.

- Reconciliation: Receiving banks cross-check IFSC + account combos before crediting, preventing orphaned credits.

- Reversal Logic: Any mismatch triggers automated reversals, safeguarding banking transactions.

2. RTGS Protection via Real-Time Checks

- Syntax & Directory Lookup: Banks implement both regex checks and live API calls to RBI’s IFSC directory for each transaction.

- Integration with MFA: RTGS portals often require OTP + MPIN after IFSC validation, reinforcing multi-factor authentication.

- AI-Based Fraud Scoring: Advanced artificial intelligence engines analyze IFSC usage patterns, flagging anomalies.

3. IMPS Fraud Mitigation through Instant Validation

- Front-End Blocking: Dynamic application security testing reveals vulnerabilities; hardened code prevents invalid IFSCs at the UI level.

- Geo-Tagging & Device Fingerprinting: IMPS apps integrate Virtual Private Network detection and device checks tied to branch coordinates.

- MMID Cross-Check: Pairing IFSC with Mobile Money Identifiers adds an extra layer of authentication.

Code Snippet: JavaScript IFSC Regex Validation

function isValidIFSC(ifsc) {

const regex = /^[A-Z]{4}0[A-Z0-9]{6}$/;

return regex.test(ifsc.toUpperCase().trim());

}// Sample Usage

['HDFC0MFRT01', 'abcd0123456', 'SBIN0000456']

.forEach(code => console.log(code, isValidIFSC(code)));How Do IFSC Codes Help Prevent Digital Payment Fraud?

In a world rife with cyber threats, IFSC codes form one of the first lines of defense:

- Input Sanitization

- Regex at the front-end and back-end prevents SQL injection, XSS, and buffer overflows.

- Security patches ensure the validation logic can’t be bypassed.

- Regex at the front-end and back-end prevents SQL injection, XSS, and buffer overflows.

- Reconciliation Checks

- The software testing life cycle for fintech apps includes automated reconciliation tests matching IFSC + account combos.

- Rapid detection of duplicate or inconsistent entries stops fraudulent duplicate payments.

- The software testing life cycle for fintech apps includes automated reconciliation tests matching IFSC + account combos.

- Branch Whitelisting / Blacklisting

- Banks maintain lists of active IFSCs; compromised codes can be blacklisted and automatically blocked.

- Machine learning models ingest IFSC usage data to flag unusual patterns - e.g., a high volume of transfers from a small rural branch all at once.

- Banks maintain lists of active IFSCs; compromised codes can be blacklisted and automatically blocked.

- Audit Trails

- Every transaction’s IFSC is logged in immutable ledgers, making forensic analysis and penetration testing software audits straightforward.

What Are the Best Practices for Verifying IFSC Codes During Transaction Processing?

A defense-in-depth approach leverages multiple layers of validation:

- Front-End Validation

- HTML5 pattern attribute + JavaScript regex.

- Auto-uppercase and trim whitespace.

- Immediate error feedback: “Format: 4 letters + 0 + 6 alphanumeric characters.”

- HTML5 pattern attribute + JavaScript regex.

- Back-End Verification

- Use a cached IFSC directory (Redis, Memcached) refreshed daily via RBI’s official CSV/JSON feed.

- Rate-limit lookup endpoints to ward off DoS attacks.

- Log all failed attempts with client IP, user agent, and timestamp.

- Use a cached IFSC directory (Redis, Memcached) refreshed daily via RBI’s official CSV/JSON feed.

- API-Level Sanity Checks

- Wrap IFSC lookups in safe-guarded API calls; avoid exposing raw database errors to clients.

- Application security testing tools (e.g., OWASP ZAP, Burp Suite) should verify no code paths skip IFSC checks.

- Wrap IFSC lookups in safe-guarded API calls; avoid exposing raw database errors to clients.

- User-Experience Enhancements

- Typeahead suggestions: Users start typing “HDFC” and see branch names + IFSC codes.

- Tooltips and inline help to reduce input errors.

- Typeahead suggestions: Users start typing “HDFC” and see branch names + IFSC codes.

- Periodic Audits & Testing

- Conduct quarterly reconciliation audits against RBI’s mandated IFSC list.

- Use automated software testing and user testing software to simulate thousands of transactions - ensuring corner cases are covered.

- Conduct quarterly reconciliation audits against RBI’s mandated IFSC list.

Code Snippet: Python Back-End IFSC Verification

import requests

RBI_IFSC_API = "https://ifsc.razorpay.com/"

def verify_ifsc(ifsc_code: str) -> bool:

""" Returns True if IFSC exists per RBI's directory """

response = requests.get(RBI_IFSC_API + ifsc_code.upper().strip())

return response.status_code == 200# Example

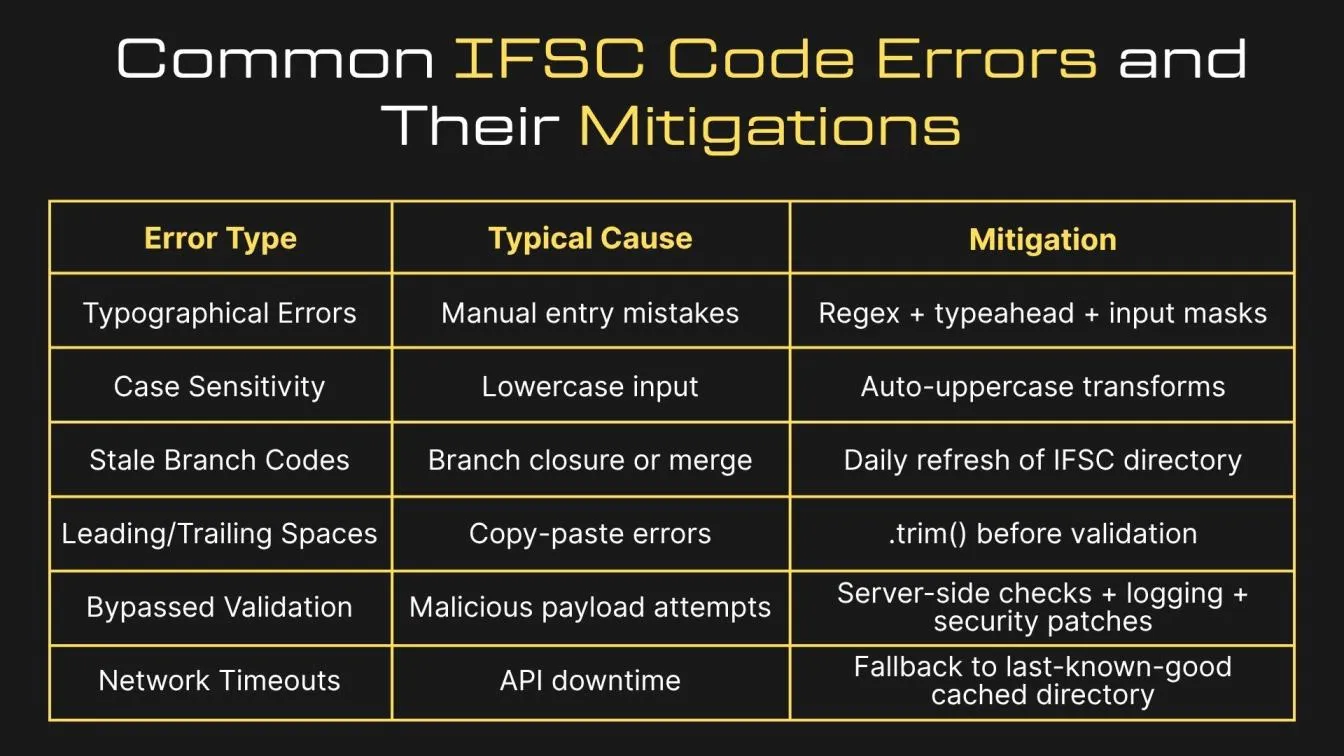

print(verify_ifsc("SBIN0000456")) # True if valid, else FalseWhat Common IFSC Code Errors Cause Transaction Failures and How Can You Avoid Them?

Even small IFSC mistakes - from typos to outdated branch codes can derail payments. Here’s how to spot and prevent each common error:

What RBI Mandates Govern IFSC Codes for Regulatory Compliance in Digital Security?

The Reserve Bank of India (RBI) has issued clear directives around IFSC codes to maintain the integrity of the digital payments eco-system:

- Master Direction on Digital Payments (RBI/2016-17/22)

- Lays out technical standards for IFSC generation, distribution, and validation.

- Lays out technical standards for IFSC generation, distribution, and validation.

- IT Act, 2000 & Amendments

- Mandates encryption of all payment credentials - including IFSC - in transit and at rest, often via Transport Layer Security (TLS).

- Mandates encryption of all payment credentials - including IFSC - in transit and at rest, often via Transport Layer Security (TLS).

- Periodic Audits

- Banks and fintech companies must reconcile their in-house IFSC directories quarterly against RBI’s official list.

- Banks and fintech companies must reconcile their in-house IFSC directories quarterly against RBI’s official list.

- Data Privacy & Protection

- Under India’s forthcoming Digital Personal Data Protection Act, IFSCs tied to personal accounts are considered sensitive personal data, subject to data minimization and secure storage.

- Under India’s forthcoming Digital Personal Data Protection Act, IFSCs tied to personal accounts are considered sensitive personal data, subject to data minimization and secure storage.

Industry Best Practice: Preserve an audit trail of every IFSC directory refresh - recording timestamps, source URLs, and checksum hashes for full traceability.

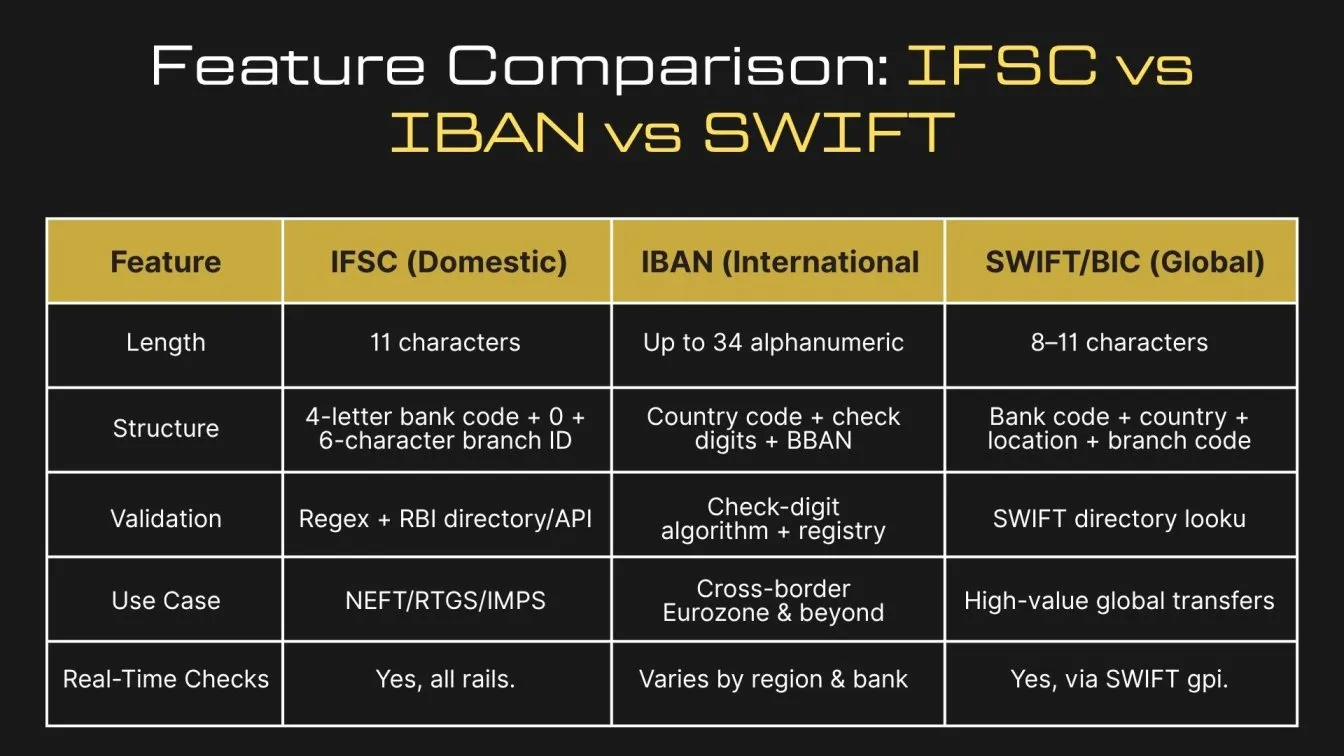

How Do IFSC Codes Compare with IBAN and SWIFT for International Transfers?

While IBAN and SWIFT excel in cross-border interoperability, IFSC’s concise 11-character format is tailor-made for India’s high-volume, low-value domestic transfers. Its simple structure enables lightning-fast NEFT, RTGS, and IMPS processing with minimal overhead.

While IBAN and SWIFT excel at global interoperability, IFSC remains optimized for India’s high-volume, low-value domestic rails - prioritizing minimal latency, simple checks, and deep integration with fintech software and digital payment gateway providers.

What Does the Future Hold for IFSC Codes in Digital Payment Security Innovations?

As India accelerates toward a Digital Transformation powered by UPI (Unified Payments Interface), open APIs, and real-time data analytics, IFSC codes will not be left behind. Emerging trends include:

- User-Friendly Aliases

- Hiding raw IFSC codes behind easy-to-remember addresses (e.g., hdfc.fort@bank) for frictionless online banking experiences.

- Hiding raw IFSC codes behind easy-to-remember addresses (e.g., hdfc.fort@bank) for frictionless online banking experiences.

- Blockchain-Backed Registries

- Storing IFSC directories on permissioned ledgers to guarantee tamper-proof, auditable histories.

- Storing IFSC directories on permissioned ledgers to guarantee tamper-proof, auditable histories.

- AI-Driven Anomaly Detection

- Integrating artificial intelligence and machine learning into security testing platforms to spot evolving fraud patterns based on IFSC usage.

- Integrating artificial intelligence and machine learning into security testing platforms to spot evolving fraud patterns based on IFSC usage.

- Geo-Fencing Enhancements

- Enforcing branch-specific GPS constraints at the API level, so transactions outside a branch’s geo-perimeter trigger OTPs or manual review.

- Enforcing branch-specific GPS constraints at the API level, so transactions outside a branch’s geo-perimeter trigger OTPs or manual review.

- Seamless Integration with Fintech Offering

- Fintech companies and digital payment apps embedding IFSC lookups into richer UX, complete with software testing of edge cases, application security testing, and robust penetration testing cycles.

- Fintech companies and digital payment apps embedding IFSC lookups into richer UX, complete with software testing of edge cases, application security testing, and robust penetration testing cycles.

By combining rigorous IFSC validation with multi-factor authentication, encryption methods, Transport Layer Security, Endpoint Security, and continuous security protocols improvements, India’s modern banking ecosystem can ensure every banking transaction is swift, user-friendly, and fundamentally secure - upholding trust in a rapidly evolving digital revolution.

Wrapping it Up

In summary, IFSC codes underpin India’s digital payment security by ensuring precise routing, real-time validation, and seamless integration with multi-factor authentication and AI-driven fraud detection for banking transactions, online banking services, and digital payment types.

Companies like Frugal Testing enhance security measures by delivering targeted application and software testing services that quickly validate critical financial transactions (e.g., IFSC lookups, OTP checks) and expose vulnerabilities early. Combined with regular IFSC directory audits, digital solutions like blockchain registries, and protection against cyber threats in POS systems and remote banking, this lean, risk-focused approach helps financial institutions keep every transaction safe in our fast-evolving digital transformation.

FAQs

👉 How to identify AML?

Deploy a combination of digital KYC, transaction monitoring engines with machine learning, PEP/sanctions screening, and Suspicious Transaction Reporting (STR) mechanisms.

👉 How to verify ACH payments?

Use micro-deposit validation, prenotification entries, handle ACH return codes (e.g., R03 - No Account), and reconcile payments against ledger entries.

👉 What is risk-based security testing?

It’s a methodology that focuses testing software efforts on high-impact, high-likelihood threats - ranked via risk analysis - covering areas like IFSC validation, authentication flows, and encryption controls.

👉 What is the difference between security and compliance testing?

Security testing uncovers vulnerabilities (e.g., pen testing, code reviews, dynamic application security testing), while compliance testing verifies adherence to standards/regulations (e.g., RBI mandates, PCI-DSS).

👉 What is a red flag in payment screening?

Indicators include unusual IFSC patterns (newly opened or dormant branches), high-value, low-frequency transfers, geolocation mismatches, rapid successive transactions to different accounts, and anomalies detected by AI-driven fraud systems.