The Reserve Bank of India’s Unified Lending Interface (ULI) is set to transform digital lending by offering a seamless, secure, and transparent way for borrowers and lenders to connect. From digital lending platforms and digital lending software to digital mortgage lending systems, ULI enables faster approvals and improved customer experience.

With the rise of fintech companies, credit card services like Capital One credit card or Bank of America credit card can integrate smarter risk assessments. Backed by digital transformation technology and enhanced through software performance testing tools like k6 performance testing, ULI marks a new era in India’s digital business transformation.

💡 What’s next? Keep scrolling to find out:

🚀 ULI: streamlines India’s digital lending with banks, NBFCs, and fintech.

🚀 Key Features: instant approvals, digital KYC, compliance automation.

🚀 Compared to Traditional Lending: faster, transparent, efficient.

🚀 Benefits: quick credit access, cost savings.

🚀 Challenges: integration, adoption, regulations.

🚀 Future: AI and fintech drive next-gen lending.

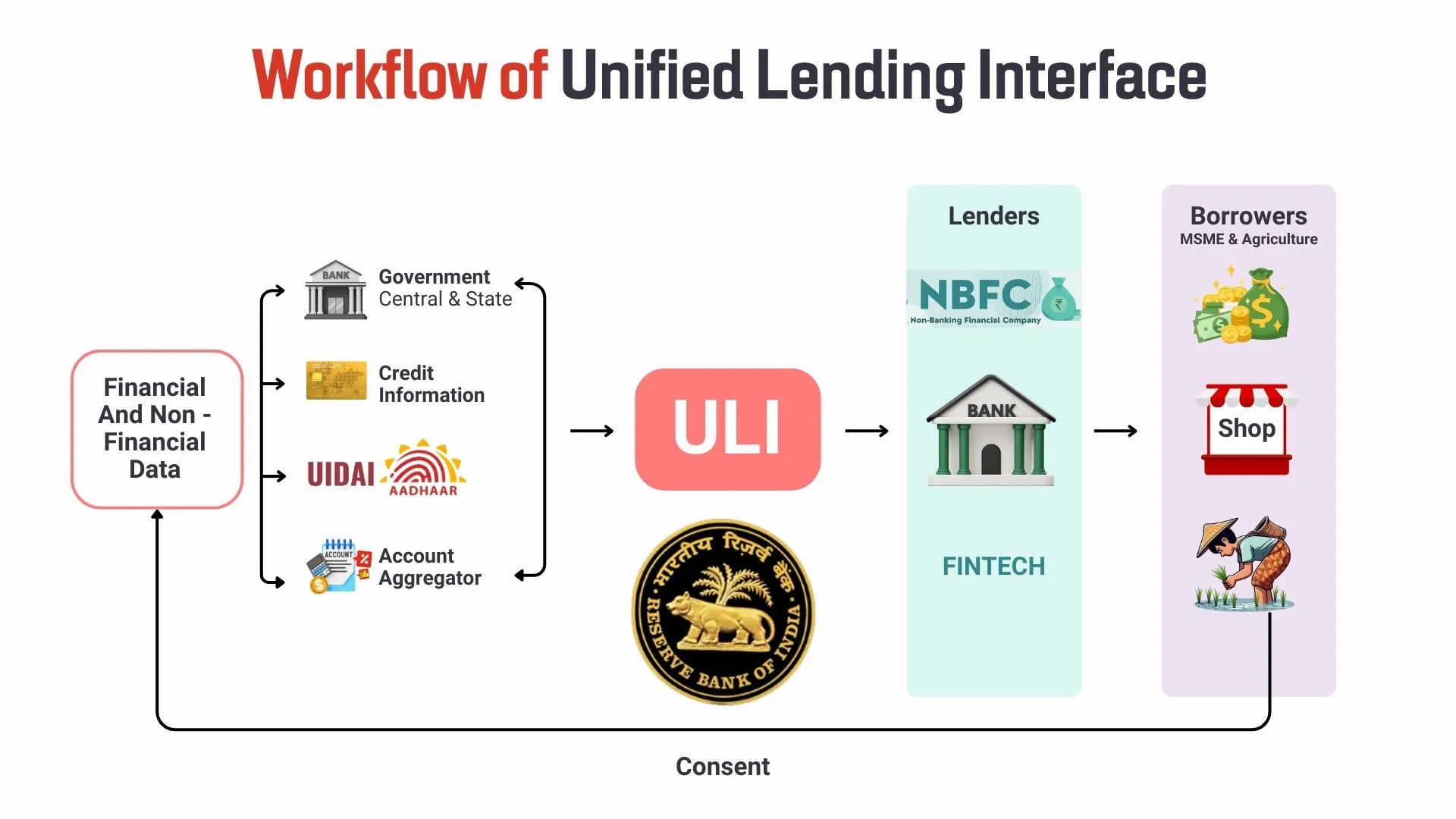

What is RBI’s Unified Lending Interface (ULI) and How It Works

The Unified Lending Interface (ULI) introduced by the Reserve Bank of India is a standardized digital framework that connects banks, NBFCs, and fintech companies under one unified protocol. It is designed to simplify loan processing, enable secure digital identity verification, and provide borrowers with faster access to credit through an interconnected ecosystem.

- Centralized Lending Framework: ULI standardizes digital lending systems so lenders can process applications more efficiently, improving approval rates and reducing operational delays.

- Automated Data Verification: Integration with digital mortgage lending platforms ensures instant borrower verification, eliminating manual paperwork and speeding up loan disbursement.

- Support for Multiple Financial Products: From small business financing to credit cards, such as Capital One Credit Card and Discover Credit Card, ULI streamlines lending workflows across all product types.

Key Features of the Unified Lending Interface

The Unified Lending Interface (ULI) brings together advanced digital lending solutions and digital transformation services to create a more transparent and efficient lending ecosystem. It aligns with the evolving needs of business digital transformation while ensuring compliance with regulatory standards and enhancing customer trust.

- Seamless Platform Integration: ULI works with multiple digital lending platforms to provide lenders with a unified access point, reducing complexity in onboarding and loan processing.

- Real-Time Performance Monitoring: With tools like k6 performance testing and software performance testing, lenders can track and optimize system performance for smoother operations.

- Enhanced User Experience: Leveraging digital transformation strategy and digital transformation process, ULI ensures fast loan approvals with minimal manual intervention.

- Security and Compliance Focus: Built with advanced web performance testing protocols, ULI safeguards sensitive borrower data and meets strict compliance guidelines.

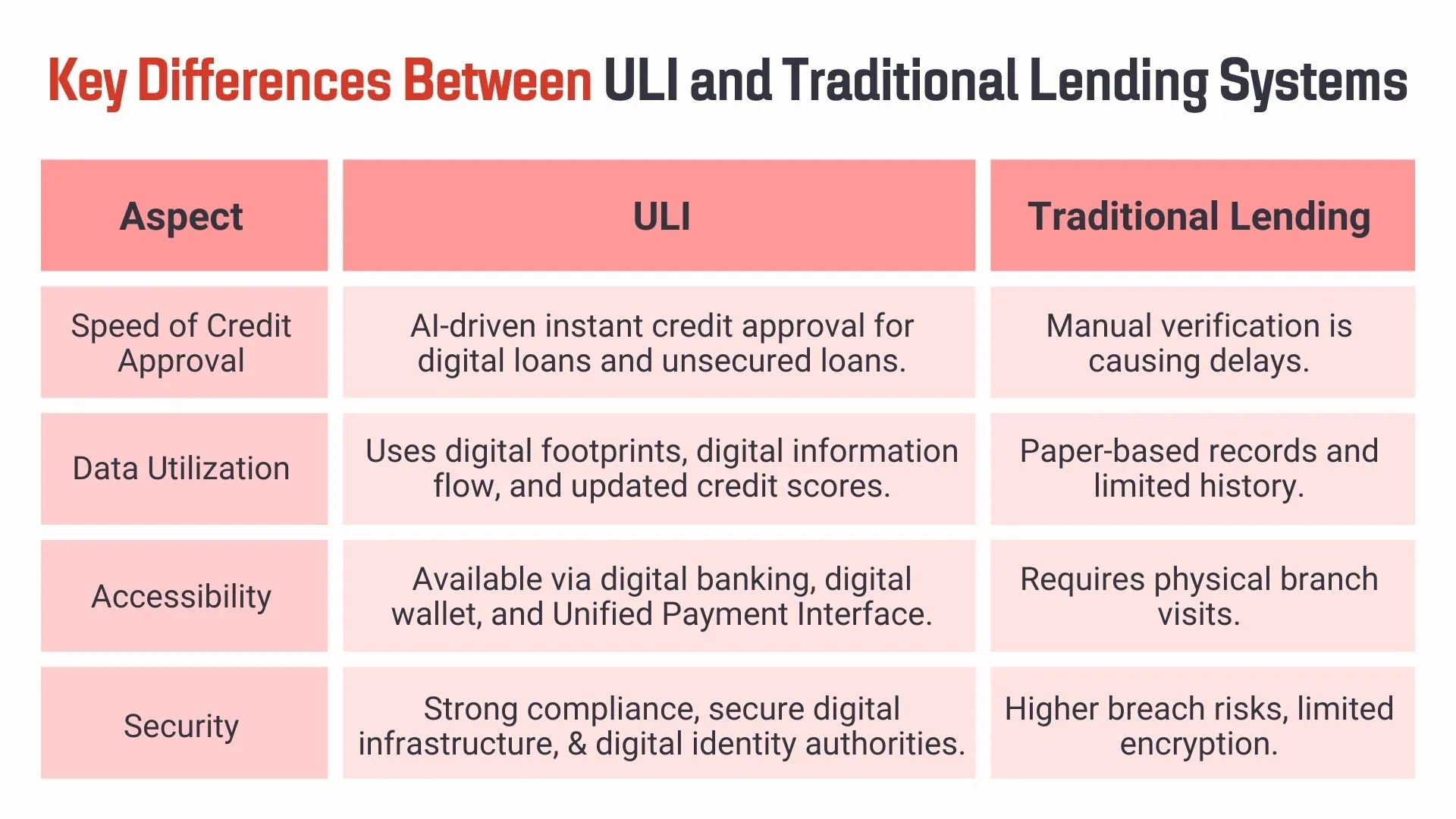

Difference Between ULI and Traditional Lending Systems

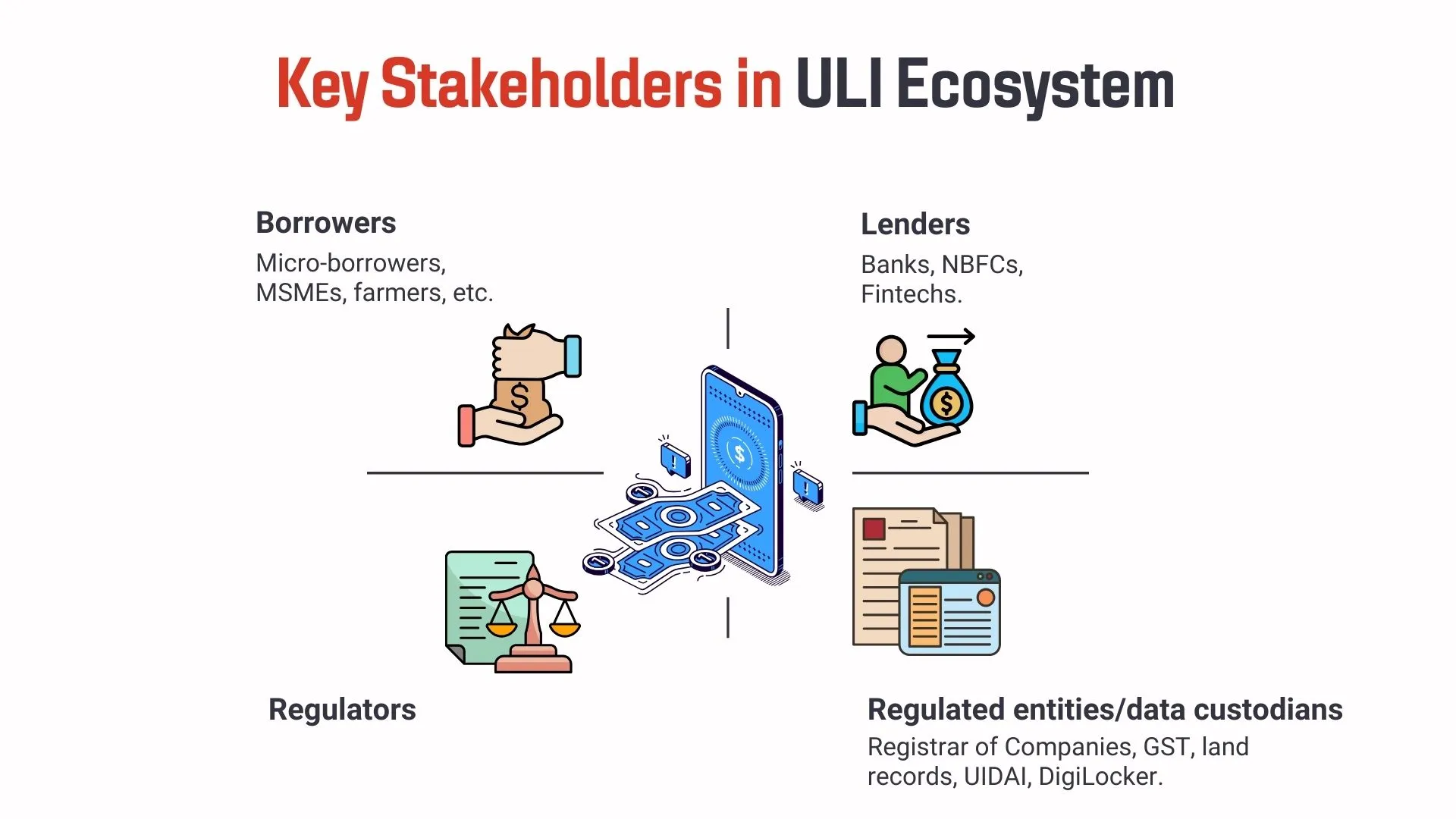

The Unified Lending Interface (ULI) is redefining the credit environment by combining digital public infrastructure with modern fintech firms, non-banking financial companies, and microfinance institutions.

It speeds up credit appraisals, improves credit scoring accuracy, and enhances credit access for micro, small, and medium enterprises as well as rural and smaller borrowers. By leveraging artificial intelligence, machine learning, and alternative data, ULI ensures frictionless credit delivery while maintaining regulatory compliance and data security.

Benefits of ULI for Lenders and Borrowers

The Unified Lending Interface (ULI) transforms the lending process by streamlining credit assessment and enabling a seamless digital innovation ecosystem. By integrating with digital infrastructure and JAM trinity services, it improves operational efficiency for lenders while offering a faster, more inclusive credit disbursement experience for borrowers.

- Enhanced Loan Processing: Automated workflows reduce turnaround time, making micro-enterprise loans and small-ticket financing more accessible. These advancements also benefit consumers seeking personal financing solutions, as lenders can process applications more efficiently and deliver faster decisions through platforms offering services such as Achieve Personal Loans.

- Broader Market Reach: Enables lenders to connect with underserved demographics through digital banking channels.

- Improved Risk Evaluation: Incorporates alternative data for more accurate risk profiling beyond traditional credit scores.

- Inclusive Financial Growth: Extends credit access to individuals without a formal banking history, including rural and smaller borrowers.

- Secure and Compliant Operations: Protects borrower data with digital identity authorities and ensures full regulatory compliance.

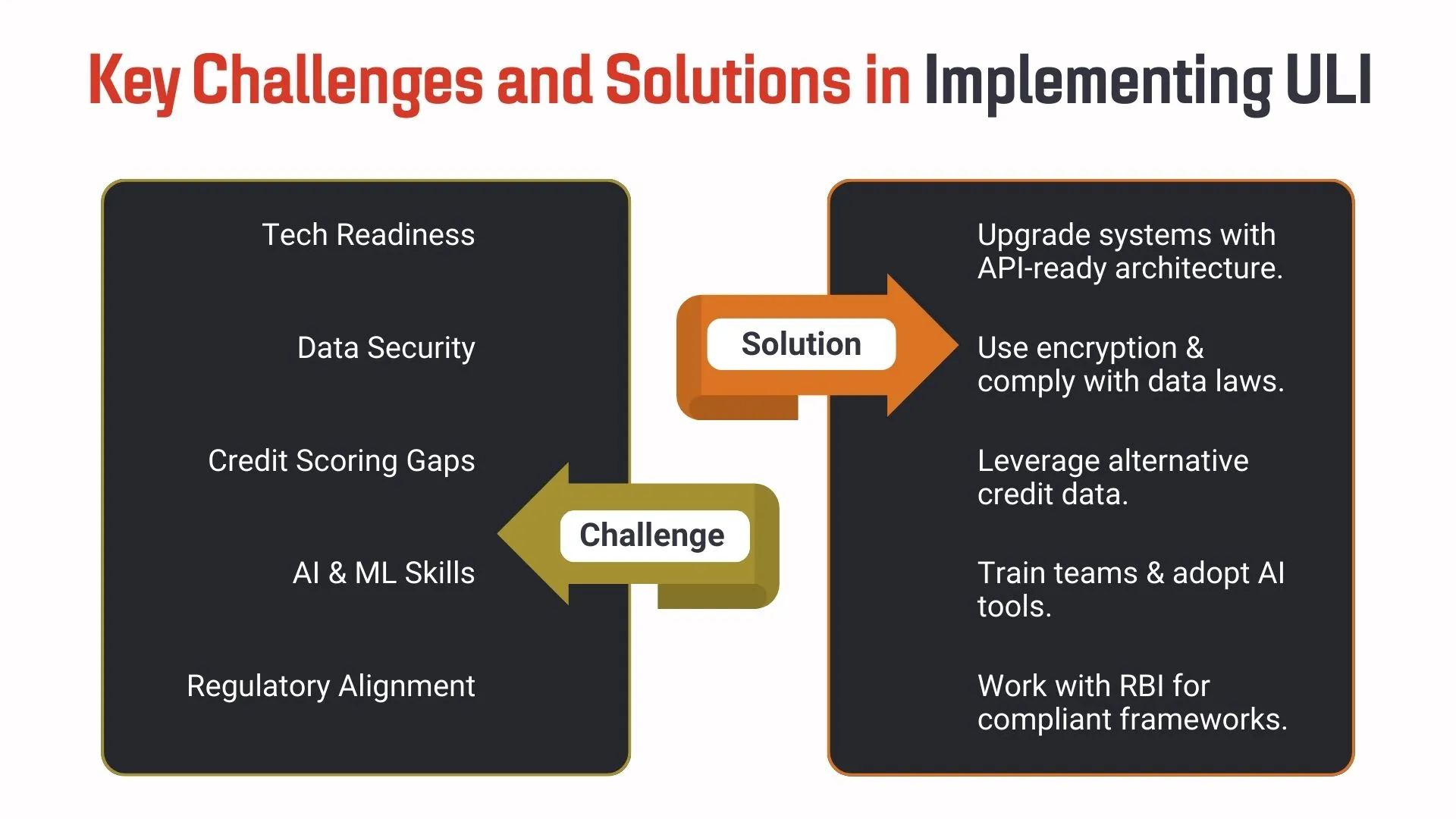

Challenges in Implementing the Unified Lending Interface

While the Unified Lending Interface (ULI) offers transformative potential, its adoption comes with operational and technological hurdles. Integrating digital public infrastructure with existing fintech firms and non-banking financial companies demands robust planning and investment. Ensuring that microfinance institutions and MSMEs can adapt to this shift is equally critical for a smooth transition.

- Technology Readiness: Legacy systems in nucleus software platforms may require upgrades to support digital information flow.

- Data Security Concerns: Protecting sensitive borrower information while enabling data access remains a top priority.

- Credit Scoring Gaps: Incorporating digital footprints into credit appraisals and credit scoring models is still evolving.

- AI & ML Integration: Leveraging artificial intelligence and machine learning for decision-making requires skilled resources.

- Regulatory Alignment: Balancing regulatory compliance with innovation, as highlighted by leaders like Shaktikanta Das, remains challenging.

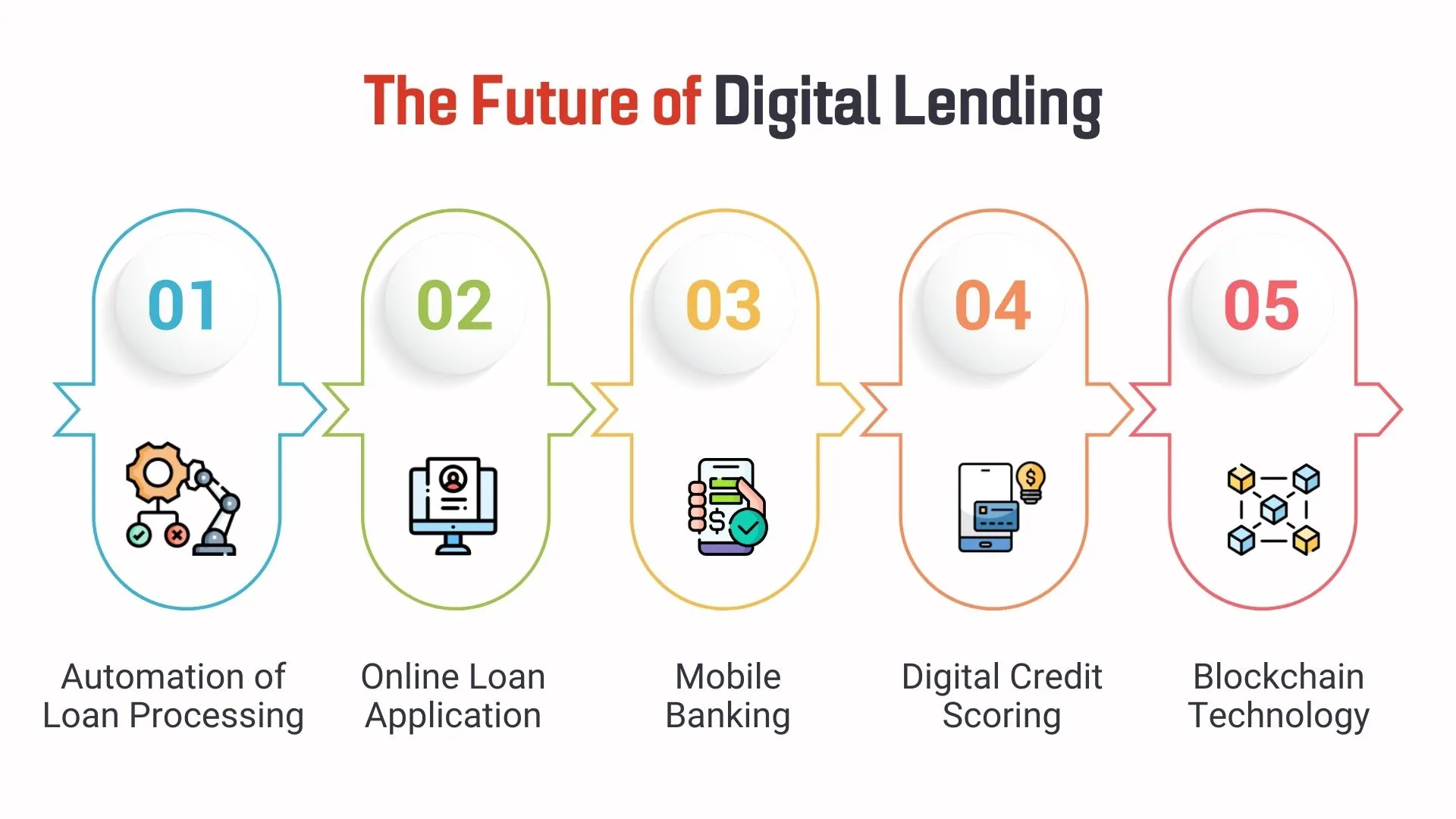

Future of Digital Lending with ULI

The Unified Lending Interface is set to redefine the future of credit by merging innovation with streamlined processes. As the financial sector embraces digital transformation trends, ULI will empower lenders and borrowers with faster, more transparent, and secure lending experiences. Its adoption by banks, fintech banking platforms, and other financial institutions will reshape how loans are processed and approved in the coming years.

- Enhanced loan accessibility: By integrating ULI with fintech companies, borrowers can access loans seamlessly, improving inclusion in underserved areas.

- Optimized lending performance: Advanced performance testing website tools will ensure smooth loan application and approval processes without system slowdowns.

- Seamless digital integration: ULI will blend with website performance testing solutions, enabling lenders to deliver a reliable and fast user experience.

- Innovative financial solutions: Leveraging fintech examples, ULI will enable diverse loan products tailored to modern consumer needs.

- Boost to digital trust: As the fintech definition evolves, ULI will strengthen secure, efficient lending in a competitive digital marketplace.

Conclusion: Unified Lending Interface as a Game-Changer for Digital Lending

The Unified Lending Interface is shaping a smarter, faster, and more inclusive lending ecosystem. By combining innovation with secure and efficient processes, it bridges the gap between traditional finance and the digital era. As adoption grows across fintech banking and financial institutions, ULI promises a future where credit access is seamless, transparent, and tailored to evolving borrower needs, driving the next wave of digital transformation in lending.

This blog explored the Unified Lending Interface, its key features, benefits for lenders and borrowers, and differences from traditional lending systems. It also covered challenges in implementation, the role of technology in enhancing credit access, and the future of digital lending. With insights into performance testing, fintech innovation, and digital transformation trends, the content highlighted how ULI is transforming the lending landscape for faster, smarter, and more inclusive credit solutions.

Frugal Testing, a leading software testing company, offers innovative solutions like functional testing services and AI-driven test automation services to enhance software quality. With expertise in selenium automation testing service and load testing service, the Frugal Testing company supports enterprises with reliable QA processes. Their software load assessment services and functional test solutions make them a trusted software testing service provider for delivering efficiency, accuracy, and performance across diverse digital platforms.

People Also Ask

1. Is ULI integrated with India’s digital public infrastructure, like UPI or Aadhaar?

Yes, ULI integrates with systems like UPI and Aadhaar, enabling instant identity verification and secure digital transactions across lending platforms.

2. How will ULI improve transparency in lending rates and charges?

It standardizes lending data, ensuring borrowers can view clear interest rates, processing fees, and hidden charges upfront before loan approval.

3. Is ULI designed to work with NBFCs as well as banks?

Yes, ULI is built to support both NBFCs and banks, fostering a unified lending ecosystem and enabling wider access to credit.

4. How does ULI handle borrower data privacy and security?

It applies encryption, tokenization, and consent-driven access while adhering to strict data protection laws for maximum borrower information security.

5. What role does AI or machine learning play in the ULI ecosystem?

AI and ML power risk profiling, fraud detection, and predictive analytics, enabling faster, more accurate, and personalized lending decisions.