As India’s digital economy accelerates, fintech companies are under increasing pressure to deliver fast, secure, and compliant payment experiences. From UPI-based transfers to ecommerce payment gateways, the demand for seamless digital payments is at an all-time high. However, with innovation comes regulation and that's where the Reserve Bank of India (RBI) plays a pivotal role.

Whether you’re building a fintech payment gateway, a mobile wallet, or a cross border digital payments platform, aligning your product with RBI guidelines isn’t optional, it's essential. The central bank enforces strict rules on everything from data localization and fraud detection to interoperability standards, all aimed at protecting consumers and maintaining financial stability.

💡 In this blog, we’ll explore:

- How the RBI regulates fintech operations and defines compliance requirements.

- Why following RBI guidelines is crucial for building secure, scalable fintech applications.

- The key regulatory mandates for digital payment systems, including data localization, security controls, and UPI interoperability.

- The core testing activities functional, security, and performance that ensure a fintech product is launch-ready.

- The testing frameworks and methodologies fintechs use to meet RBI compliance standards.

What is the Role of RBI in Fintech ?

The Reserve Bank of India plays a pivotal role in shaping the fintech technology ecosystem in India. In the age of digital transformation, it has expanded its scope to oversee and regulate the rapidly growing fintech industry including everything from fintech payments and best payment gateway systems to fintech software solutions and cross-border transactions.

RBI’s role in fintech revolves around three key pillars:

- Stability: Ensuring a safe and resilient digital financial ecosystem

- Security: Protecting consumer data and preventing fraud

- Standardization: Enforcing interoperability across platforms like UPI, NEFT, and RTGS

As fintech adoption accelerates across India, RBI has taken proactive steps to strike a balance between regulatory control and technological innovation. Whether you're building a fintech payment gateway, offering BNPL (Buy Now, Pay Later) services, or working on global payment gateway integration, your product must comply with RBI’s framework to ensure operational viability and trust in the Indian market.

Importance of following RBI guidelines for fintech apps

For any digital payments company operating in the fintech industry, aligning with RBI guidelines is not just a regulatory checkbox, it's a strategic necessity. Whether you're developing a fintech payment gateway, offering ecommerce payment fintech solutions, or building a digital wallet, Square Digital Payments ensures your gateway payment processing platform is legally viable, secure, and market-ready by adhering to RBI compliance standards.

Here’s why strict adherence to RBI guidelines is essential for fintechs:

- Legal Authorization

RBI mandates licensing and approval for operating any payment gateway system, wallet, or payment aggregator service in India. Non-compliance can result in heavy penalties or loss of authorization. - Data Security and Localization

RBI enforces robust data localization and encryption norms, requiring all financial and transaction data to be stored within India. This ensures greater control, security, and accountability. - Risk Reduction and Fraud Prevention

Adhering to RBI's transaction monitoring and fraud detection standards reduces vulnerabilities, enabling faster fraud response and risk mitigation. - Platform Integration Compatibility

Compliance is required for fintechs to integrate with regulated networks such as UPI, NEFT, IMPS, and RTGS, as well as with secure payment gateways like PayPal, Razorpay, or PhonePe. - Consumer Trust and Brand Reputation

Customers and investors are more likely to trust digital payments companies that demonstrate regulatory compliance and commitment to data protection.

Key Guidelines Issued by RBI for Digital Payment Systems

As the backbone of India’s digital payments ecosystem, the Reserve Bank of India (RBI) has introduced several guidelines that fintech companies must comply with before launching or scaling their platforms. These regulations ensure the safety, transparency, and interoperability of payment systems in India.

Below are the most critical RBI directives that impact fintech development services, payment gateway systems, and digital payment companies:

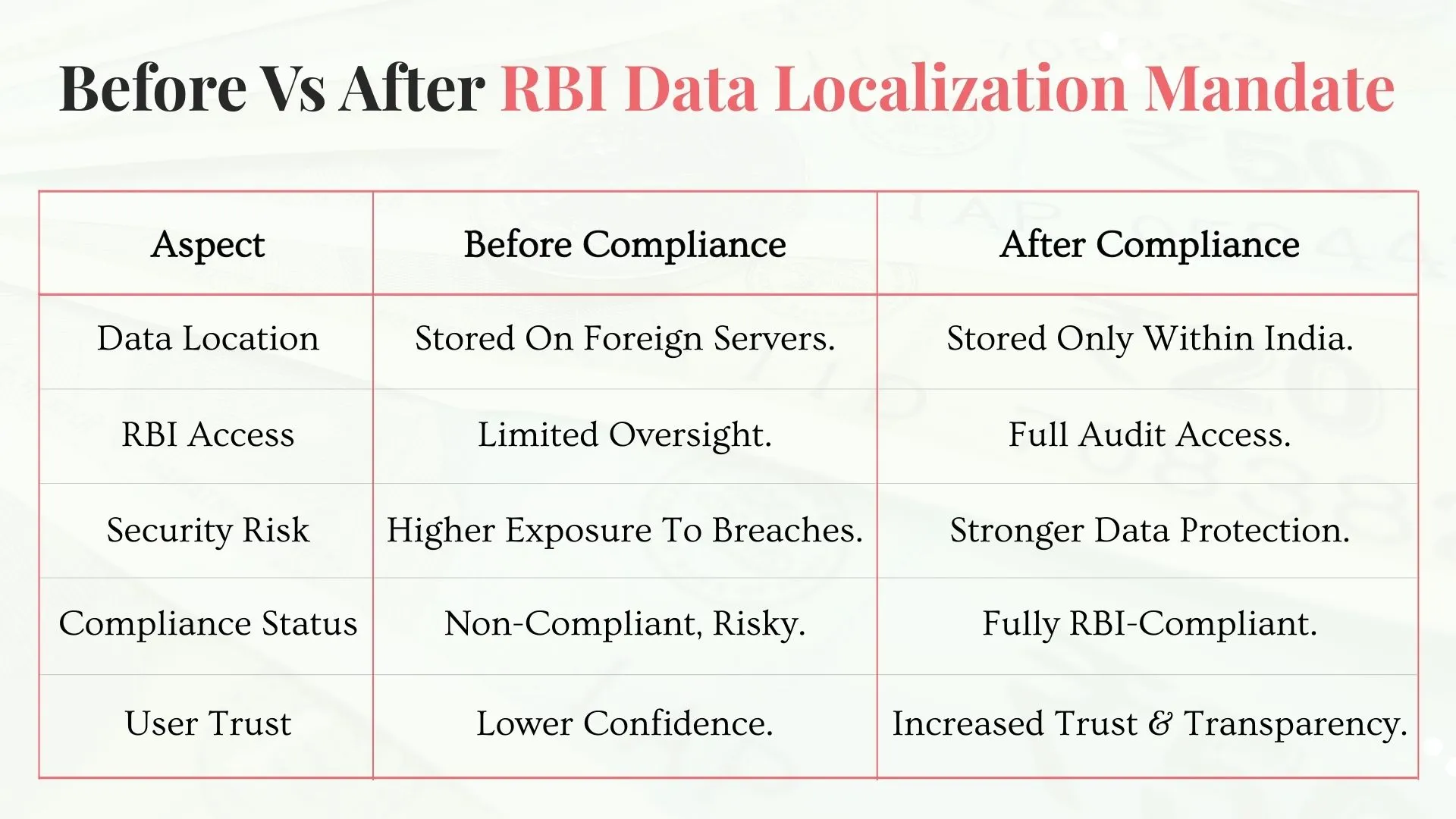

Data Localization and Security Requirements

In an effort to strengthen the integrity of India's financial ecosystem, the Reserve Bank of India (RBI) introduced strict data localization and security compliance requirements for all payment system operators and fintech companies operating in the country prompting a shift toward more secure and regulation-ready fintech software development services.

This mandate aligns with digital payments trends that prioritize data sovereignty and cybersecurity, ensuring that all transaction-related data is stored and processed within India’s geographical boundaries. It helps prevent unauthorized access, data breaches, and the cross-border misuse of sensitive financial information

What Does RBI’s Data Localization Mandate Require?

- Full end-to-end transaction data including card credentials, payment timestamps, transaction values, and user details must be stored on servers physically located in India.

- If the data is processed overseas (e.g., by a global payment gateway), a complete copy must be brought back to India within 24 hours and stored locally.

- Fintechs must provide unrestricted access to RBI for auditing and monitoring stored data.

- Companies are required to conduct regular security audits, penetration testing, and follow encryption standards such as AES and TLS.

Why This Is Critical for Fintechs

- Legal Obligation: Operating without compliance may lead to RBI banning onboarding or freezing services.

- Consumer Trust: Localized data handling improves transparency and builds user confidence in the app or platform.

- Cybersecurity: In-country data handling reduces risks associated with global infrastructure attacks or surveillance.

- Operational Oversight: RBI gains direct access for fraud investigation, financial risk analysis, and legal disputes.

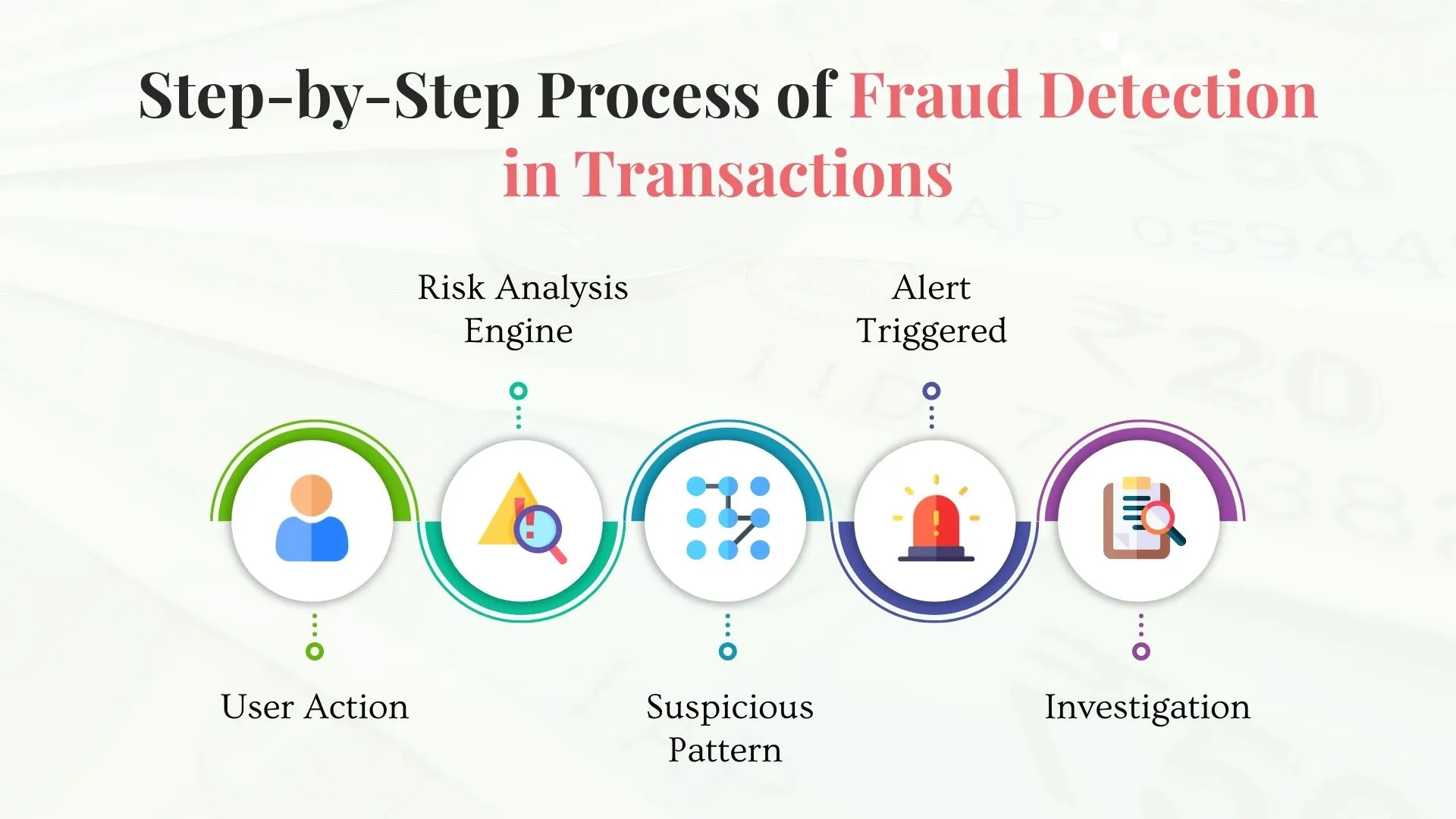

Transaction Monitoring and Fraud Detection

To combat rising threats of digital payment fraud, the Reserve Bank of India (RBI) has issued firm directives on real-time transaction monitoring, anomaly detection, and fraud prevention. These guidelines are especially critical for fintech platforms and payment gateways operating in India’s fast-growing digital economy.

The objective is to ensure early detection of suspicious activity, block fraudulent transactions before they are processed, and maintain a secure, trusted environment for digital financial services.

What Does RBI’s Fraud Detection Guideline Require?

- Fintech platforms must implement AI or rule-based monitoring systems to detect suspicious patterns in real-time (e.g., multiple failed login attempts, unusual transaction volume).

- All payment system operators must report attempted or successful fraudulent transactions to the RBI and relevant stakeholders promptly.

- Companies must set up escalation procedures and alert mechanisms for flagging high-risk behavior like account takeovers or phishing attempts.

- Historical transaction data should be analyzed continuously to improve fraud models using behavioral analytics and risk profiling.

- Strong customer authentication (SCA) and transaction limits must be enforced for high-risk activities or international payments.

Why This Is Critical for Fintechs

- Prevents Financial Losses: Instant detection of fraud helps block illegitimate access before funds are compromised.

- Regulatory Safety: Non-compliance may result in license restrictions or penalties from the RBI.

- Customer Retention: Demonstrating proactive fraud management increases consumer trust and platform credibility.

- Operational Readiness: Ensures the fintech is well-prepared to respond during cyber-attacks or social engineering scams.

Interoperability and UPI Compliance Standards

The Reserve Bank of India (RBI) requires fintech platforms and digital payment operators to strictly adhere to interoperability and compliance standards, particularly when handling sensitive customer information. Ensuring seamless integration across payment systems while maintaining data security is essential not only for legal compliance but also for fostering user trust in digital financial services.

These guidelines highlight the importance of secure data handling, robust encryption protocols, consent-based data sharing, and minimal data retention to reduce risks such as identity theft and unauthorized access.

What Do RBI’s Interoperability & Compliance Guidelines Require?

- Fintech platforms must implement systems that allow smooth interoperability across UPI, NEFT, RTGS, and other payment networks while ensuring secure data transmission.

- Only essential customer data should be collected and protected with end-to-end encryption.

- Platforms must obtain explicit user consent before collecting or sharing data, with transparent communication on how data will be used.

- Role-based access and audit trails must monitor access to sensitive data.

- Third-party integrations (e.g., analytics or payment vendors) must comply with RBI-approved security and compliance standards.

- Clear data retention policies should be in place, with deletion of data once it is no longer required for processing.

Why This Is Critical for Fintechs

- Regulatory Compliance: Ensures alignment with RBI’s Master Directions, UPI regulations, and India’s data protection laws.

- Operational Security: Reduces vulnerabilities and strengthens overall system integrity.

- User Trust: Transparent data handling and interoperability increase customer confidence and platform adoption.

- Reputation Management: Minimizes risks of breaches that could damage the brand or attract penalties.

Core Testing Areas Fintechs Must Cover Before Launch

Before a fintech product enters the competitive digital payments market or the rapidly evolving digital lending ecosystem, it must go through rigorous testing to ensure it’s reliable, secure, and compliant with the regulatory framework. With rising concerns over consumer protection, data breaches, and regulatory non-compliance, overlooking any key testing area can lead to operational failures or legal repercussions.

Whether you're building payment banks, digital lending applications, or platforms using machine learning and artificial intelligence, your QA process should focus on functionality, security, and performance to ensure a seamless user experience, maintain trust through robust consumer protection, and stay compliant with the ever-evolving fintech regulatory landscape.

Functional Testing for Payment Workflows

Functional testing ensures that every step in your payment journey from user authentication to transaction completion works exactly as expected. In the digital lending ecosystem or digital payment apps, even a minor glitch can disrupt user trust and lead to financial or reputational loss.

Whether you're handling digital loans, virtual digital assets, or peer-to-peer transfers, it’s crucial to verify that all workflows operate seamlessly under different scenarios. This includes validating each process through functional testing services to ensure accuracy, compliance, and a secure user experience:

- User login via digital identity mechanisms

- Payment initiation, processing, and confirmation

- Refunds and chargeback handling

- Integration with account aggregators and third-party services

- Edge cases like payment failure or session timeouts

With evolving Digital Lending Guidelines and a complex regulatory environment, these workflows must align with compliance mandates, such as issuing a Key Fact Statement or capturing secure digital signatures.

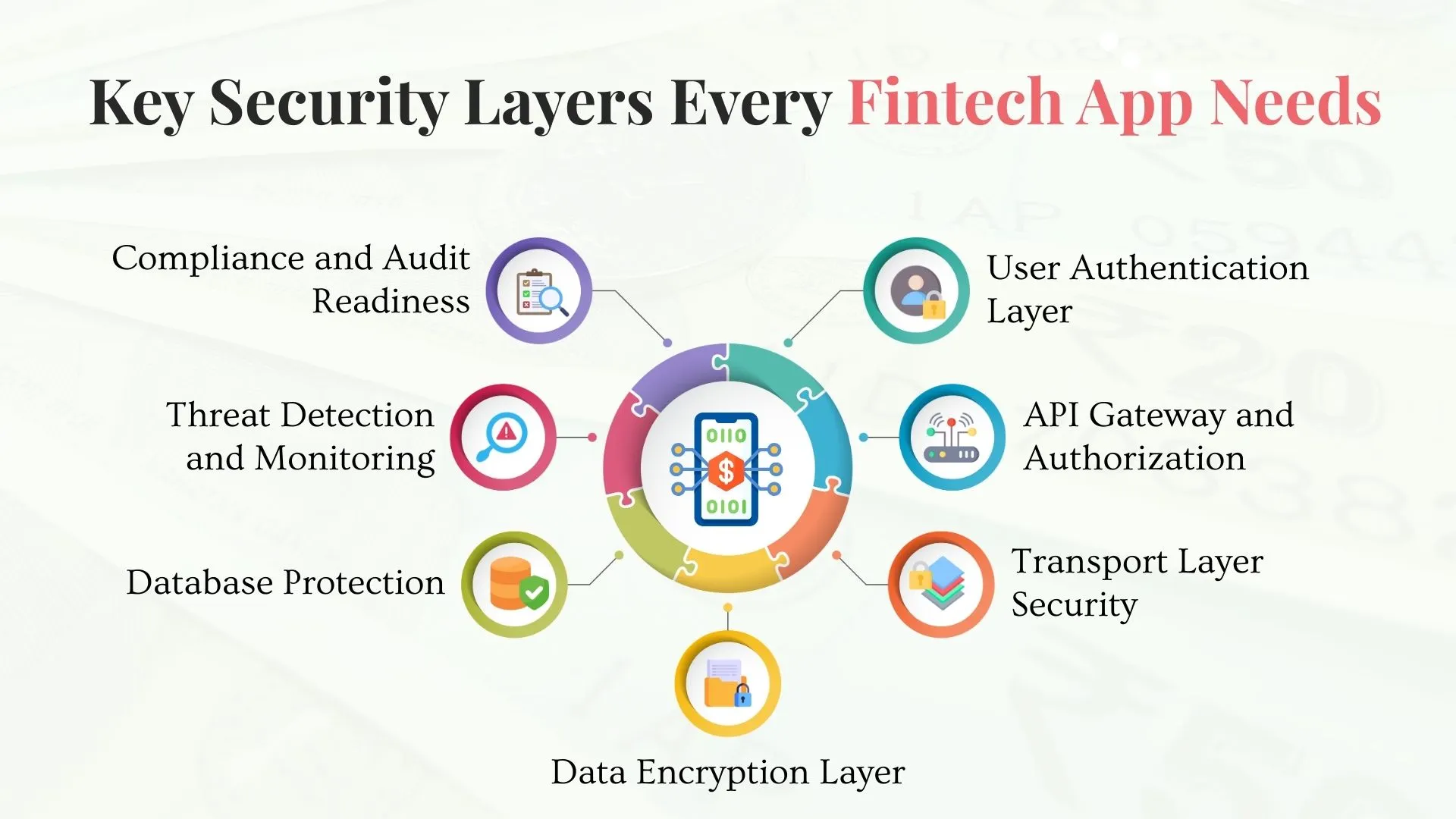

Security Testing for Data Protection

Security is non-negotiable in fintech examples like mobile wallets, digital lending apps, and UPI-based platforms. With sensitive data such as Aadhaar numbers, PAN details, OTPs, and bank credentials being exchanged, even a small vulnerability can lead to a massive breach of trust. In India’s regulated financial environment, non-compliance can also attract hefty penalties. AI-driven test automation services can help identify security gaps faster, ensure compliance with regulations, and safeguard user trust through continuous, intelligent testing.

Important Areas for Security Testing:

- API Security Testing

Validate encryption protocols (e.g., TLS), authentication mechanisms (OAuth 2.0), and token management for APIs interacting with banks, credit bureaus, or UPI networks. - Data Encryption Checks

Ensure both data-in-transit and data-at-rest are encrypted using standards like AES-256. Fintech apps should avoid storing sensitive data unless necessary, and when they do, it must be securely encrypted. - Vulnerability Scanning & Pen Testing

Conduct regular scans for OWASP Top 10 vulnerabilities such as SQL Injection, Broken Authentication, and Insecure Deserialization. Simulate real-world cyberattacks to test system resilience. - Secure Authentication

Verify implementation of MFA (Multi-Factor Authentication), strong password policies, and proper OTP verification flows for user onboarding and high-value transactions. - Compliance Readiness

Your app must pass compliance audits for RBI, PCI-DSS, and CERT-In guidelines. Automated security tests should be part of your CI/CD pipelines.

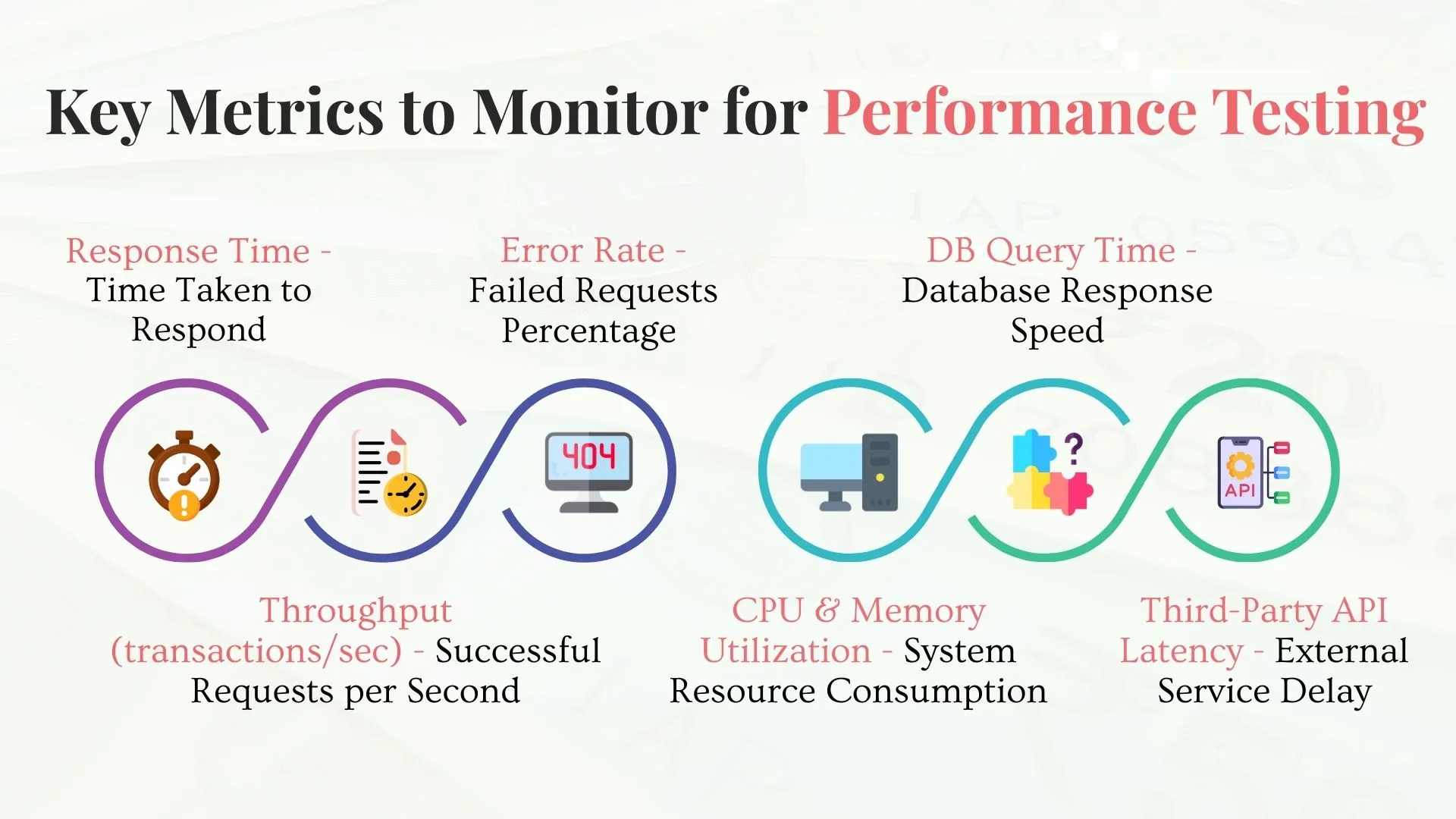

Load and Performance Testing Under Peak Conditions

Fintech apps often face unpredictable user traffic, especially during salary days, IPO launches, or festive seasons. By leveraging Load Testing services, you can evaluate how your application performs under peak conditions and ensure a seamless, uninterrupted user experience.

Core Performance Testing Areas:

- Load Testing: Simulate expected user traffic (e.g., 10,000 concurrent users) to validate if the system performs optimally without degradation.

- Stress Testing: Push your app beyond its capacity to identify breaking points. Helps in understanding system behavior under extreme loads.

- Spike Testing: Test how your app handles sudden surges in traffic (e.g., during flash sales or government scheme deadlines).

- Endurance Testing: Ensure system stability during prolonged usage. This is crucial for apps expected to run 24/7.

- Scalability Testing: Verify if your app can scale horizontally/vertically by adding more servers or cloud resources under load.

Testing Frameworks Commonly Used by Fintechs to Meet RBI Guidelines

To meet strict financial regulation standards set by the Reserve Bank of India (RBI), fintechs especially Non-Banking Financial Companies (NBFCs) rely on QA testing services for enterprises. These services provide structured, automation-friendly testing frameworks that help ensure customer protection, safeguard sensitive data, and maintain a consistent user experience. They also validate integrations with platforms from the payment gateway list, ensuring they meet both compliance and performance expectations.

Here are the commonly adopted testing frameworks:

1. TestNG / JUnit (for Unit Testing)

These are the foundational frameworks used to test core business logic and financial technologies functionalities early in development.

- Ensure logic adheres to Regulatory Technology checks

- Enable fast feedback loops to prevent defects

2. Rest Assured / Postman (for API Testing)

APIs are critical in fintech apps for integrations with banks, payment systems, and third-party tools. These frameworks validate:

- Secure handling of customer data

- Authorization flows for customer protection

- API compliance with financial regulation

3. OWASP ZAP / Burp Suite (for Security Testing)

Security frameworks help identify vulnerabilities that could expose sensitive customer data or impact compliance.

- Ensure encryption, token handling, and access control

- Comply with RBI’s data privacy mandates

4. JMeter / Gatling (for Performance Testing)

Load testing ensures the app stays responsive during high-traffic periods like salary days or tax-filing deadlines.

- Monitor response times to maintain customer experience

- Detect bottlenecks in Non-Banking Financial Company systems

5. Selenium / Cypress (for UI Testing)

UI automation ensures customer workflows like onboarding, payments, and KYC remain seamless across platforms.

- Check for accessibility and input validation

- Ensure workflows align with RBI guidelines

📝 Final Thoughts

As digital payments continue to reshape India’s financial ecosystem, staying aligned with fintech trends and compliance with RBI guidelines is not just a legal necessity, it's a trust-building imperative. Throughout this blog, we explored how the RBI plays a pivotal role in shaping fintech trends by regulating operations from enforcing stringent security measures and ensuring data localization to facilitating seamless UPI integration APIs and promoting interoperability.

We walked through essential testing areas every fintech must prioritize whether it's validating core payment functionalities, ensuring airtight data security, or confirming system resilience under peak loads. Equally important are the modern testing frameworks that help fintech companies streamline these efforts and stay audit-ready.

By avoiding common testing oversights and implementing robust QA strategies, fintechs can not only meet RBI’s rigorous requirements but also deliver secure, seamless, and reliable experiences for their users. In an industry where customer protection and regulatory alignment are non-negotiable, thorough testing is the foundation of long-term success.

FAQs

1. How often does RBI update its digital payment regulations?

RBI updates its digital payment regulations periodically based on evolving technology and market requirements, without a fixed schedule.

2. Can third-party vendors help ensure RBI compliance during testing?

Yes, third-party vendors assist fintechs by providing specialized testing and security assessments to ensure adherence to RBI compliance standards.

3. What is the role of audits in maintaining RBI compliance?

Audits help monitor fintechs adherence to RBI guidelines, focusing on cybersecurity, operational risks, and regulatory compliance for ongoing oversight.

4. How do RBI guidelines impact recurring payments and subscriptions?

RBI supports secure recurring payments through frameworks like NPCI’s Unified Presentment Management System (UPMS), enabling automated billing for subscriptions.

5. Can fintechs customize their KYC process under RBI’s digital payment rules?

Fintechs must follow RBI’s KYC mandates strictly however, within these rules, they can optimize customer experience by adopting technology-driven digital KYC processes.