Companies handling real cash operate in high-risk environments where even minor API weaknesses in mobile banking or payment systems can result in data breaches and fraudulent transactions. To protect financial data and user information, organizations must secure all endpoints using API Security, API Authorization, Encryption Algorithms, Two Factor Authentication, Biometric Authentication, Device Fingerprinting, and Cloud Security Validation.

A structured penetration testing plan combining automated and manual penetration testing, OWASP Top 10 validation, Real-Time Fraud Detection, AML Monitoring, and Continuous Vulnerability Management helps prevent API exploitation and phishing attacks. This approach also ensures regulatory compliance with PCI-DSS and GDPR while strengthening overall fintech cybersecurity.

Understanding Fintech App Security

It is critical to protect the confidentiality of financial data, payment gateway integration security, and security for user transaction security in order to maintain trust in a business and meet the requirements for regulatory compliance.

This includes protection of payment data, user information, cloud security validation, and alignment with compliance frameworks, AML monitoring, Money Laundering prevention, and Money Transmitter Licenses required by payment processors and fintech startups.

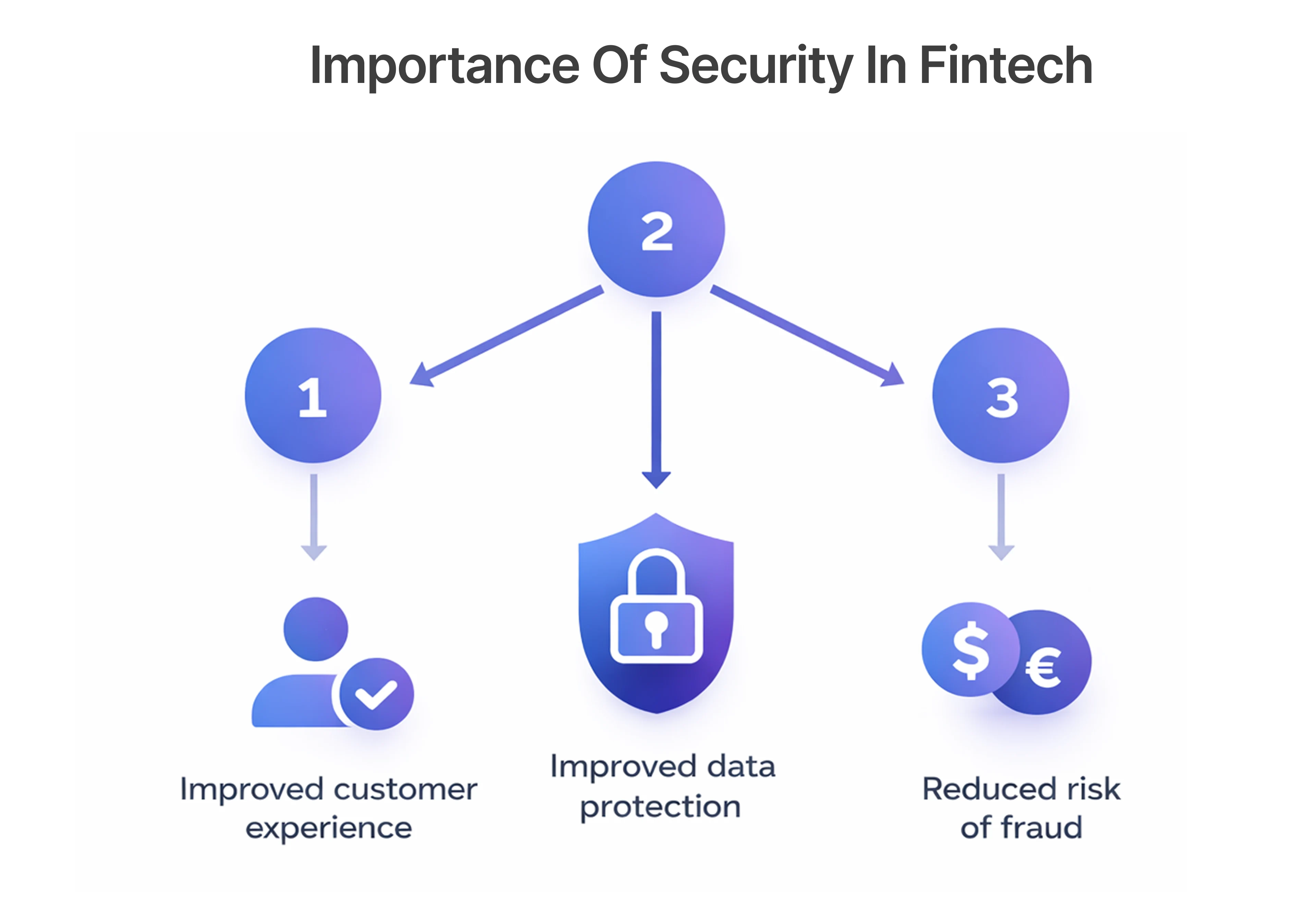

The Importance of Security in Fintech

Fintech platforms handle sensitive financial data, transactions, and users' identities. Any security weakness may impact both customers and financial institutions. Thus, strong fintech cybersecurity provides:

- Protection of financial data security and user identity

- Safe payment gateway integration and payment transactions

- Compliance with global regulations on cybersecurity in financial services

- Prevention of fraud and erroneous access to financial systems

Support for real-time fraud detection, transaction monitoring, fraud detection systems powered by machine learning, and prevention of phishing attacks across digital banking channels.

Without sufficient testing for fintech security and application security, fintech companies will be vulnerable to financial loss and damage to their brand reputation.Security measures such as multi-factor authentication, biometric authentication, device fingerprinting, role-based access control, and encryption algorithms help mitigate these risks.

Key Components of Fintech App Security

Secure fintech applications require a multi-layered security approach across application, infrastructure, and network layers to protect real money transactions.

Key components include:

- Secure gateways and payment systems to protect financial data and user information

- Encryption Algorithms, Two Factor Authentication, Biometric Authentication, and Device Fingerprinting

- API Security and API Authorization controls

- Application Security Testing, Continuous Vulnerability Monitoring, and regular Security Testing

- AI Tokenization, Blockchain Technology, Cloud Security Validation, and secure Third-Party APIs integration across Open Banking

These measures ensure secure payment processing across mobile banking apps, mobile wallets, and traditional banking systems.

Emerging Threats in Fintech Security

As fintech adoption grows, cyber threats targeting financial platforms continue to evolve. Attackers exploit vulnerabilities in payment systems, APIs, and mobile applications to access sensitive financial data and transactions.

Common threats include:

- API and Payment Gateway vulnerabilities exposing transaction data

- Account Takeover due to weak authentication

- Malware targeting mobile banking and fintech applications

- Data Breaches involving sensitive financial data

- Insider Threats and misconfigured access controls

- API Exploitation, API Abuse, Phishing Attacks, and Cloud Security misconfigurations across Open Banking and Third-Party APIs

To stay ahead, fintech organizations must adopt proactive security strategies using advanced vulnerability detection and continuous monitoring. Technologies such as Machine Learning-based Fraud Detection, Real-Time Fraud Detection, AML Monitoring, and Device Fingerprinting play a critical role in strengthening modern fintech security frameworks.

The Role of Penetration Testing in Fintech Security

Fintech companies use penetration testing to identify security gaps in their networks that could be exploited by hackers. Financial data is critical and processed at a fast pace, so continuous testing of applications, networks, and payment processes is key to minimizing the risk of fraud or theft of personal information.

Regular testing will continue to improve Application Security, support compliance with regulations, and gain the user's confidence by checking for vulnerabilities within the OWASP Top 10 Risks, the API Security, Cloud Security Validation gaps (also known as “Gaps in Cloud Security Validation”), and vulnerabilities within Mobile Banking Apps and Open Bank Services.

And deficiencies within financial applications, or at the Network Level when payment processing.

What is Penetration Testing?

A penetration test is an authorised security assessment tool that simulates a real-world cyberattack as a way to identify vulnerabilities in your networks, applications, or payment systems.

Through penetration testing, organisations gain insight into their financial cybersecurity readiness, enhance the security of their fintech application, and remediate vulnerabilities before they are exploited by hackers.

Tools like OWASP ZAP are commonly used to identify API abuse, API exploitation, and OWASP Top 10 vulnerabilities in fintech ecosystems.

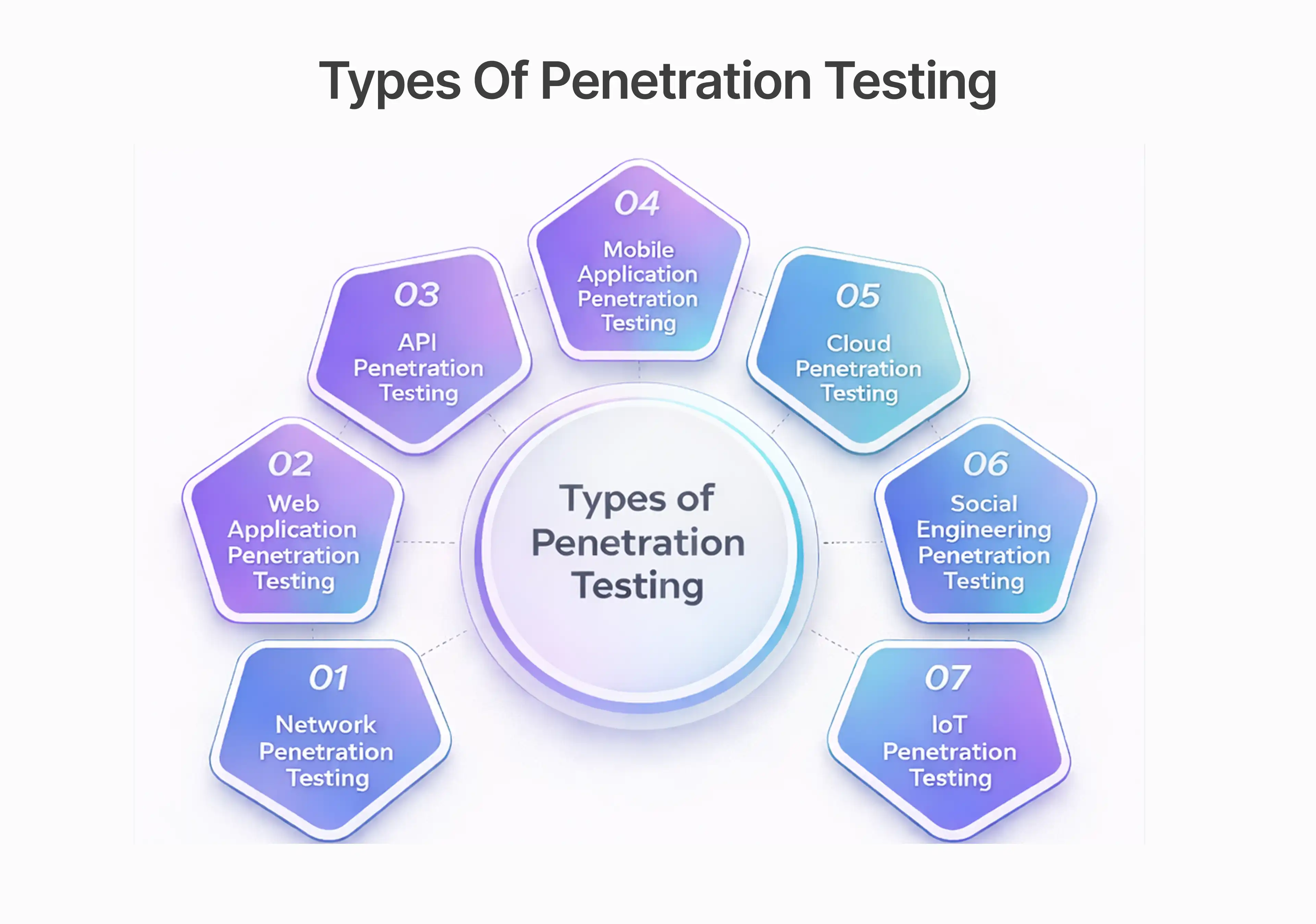

Types of Penetration Testing

Each approach supports strong application security testing across fintech ecosystems. They also help validate API authorization, firewall configurations, hardware encryption, and encryption algorithms used to secure payment data and user information.

Choosing the Right Penetration Testing Service

It is important to select a suitable Penetration Testing provider for accurate testing results and security compliance regarding Finance Standards.

Necessities for evaluation include:

- Proficient in Financial & Application Security Testing

- Utilising Advanced Tools/Methodologies for Penetration Testing

- Knowledge of Regulatory & Compliance Requirements

- Well-defined Reporting with Actionable Recommendations

Experience in open banking security, cloud security validation, third-party APIs testing, and compliance with Money Services Business regulations and Money Transmitter Licenses.

Collaborating with a knowledgeable service provider allows Fintech companies to identify IT process weaknesses more quickly and provide solutions to fix them while improving overall security through advanced knowledge regarding the IT environment.

This ensures alignment with compliance frameworks, AML monitoring, and global financial industry security standards.

Essential Elements of a Pentesting Checklist for Fintech Apps

FinTech companies can identify vulnerabilities in their systems and processes by using a well-developed penetration test checklist to assist them with securing their transactions and protecting their sensitive financial data. Because FinTech Apps process real money and other important customer data, all phases of penetration testing need to be sufficiently planned, performed, and reviewed.

This is especially crucial for API-driven open banking services, mobile banking apps, mobile wallet platforms, and fintech startups undergoing digital transformation.

Pre-Testing Considerations

Pre-testing should include evaluation of API security, API authorization,Cloud Security Validation, third-party APIs, firewall configurations, device fingerprinting systems, and hardware encryption implementations.

To properly define the above items, the following items should be included in consideration:

- Identify mission-critical assets, including payment systems, user databases, and transaction flows.

- Overall, map all payment gateway/API integrations within the environment to identify possible entry points for an attack

- Define any applicable regulatory/compliance obligations as it applies to financial services.

- Full assessment of application security, network infrastructure, and access controls

- Create a secure testing environment and have any necessary permissions.

The use of a structured vulnerability assessment at this stage will give visibility into which components of the environment are at a higher likelihood/greater severity risk and allow for more efficient testing.

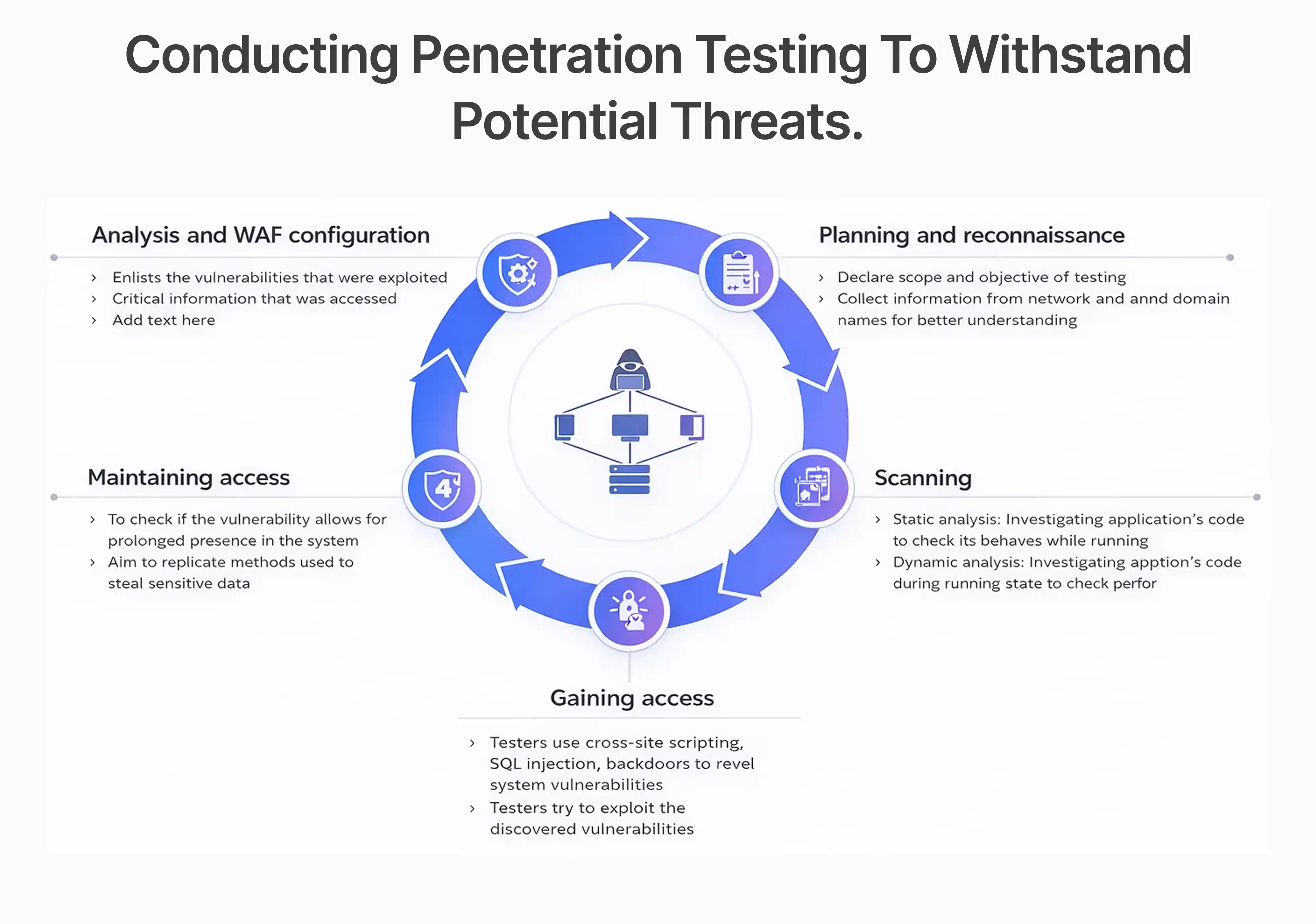

Conducting the Penetration Test

During the testing phase, security teams simulate real-world attack scenarios to evaluate how well the fintech application can withstand potential threats. This helps identify weaknesses in both infrastructure and application layers.

Key actions:

- Test authentication and authorisation mechanisms for potential misuse

- Evaluate payment gateway integration and transaction security.

- Perform vulnerability testing and detection across applications and APIs

- Analyse transaction workflows to detect logic flaws or bypasses.

- Conduct network penetration testing to assess server and infrastructure security.

Security teams use advanced penetration testing tools and vulnerability detection tools to uncover hidden risks and validate system resilience.

Post-Testing Analysis and Reporting

After testing is completed, findings must be analysed, documented, and resolved to strengthen overall security. Clear reporting ensures that development and security teams can address issues effectively.

Post-testing steps:

- Analyse identified vulnerabilities and assess their risk levels.

- Generate detailed reports with technical findings and recommendations.

- Prioritise remediation for critical and high-risk issues.

- Implement fixes and security improvements.

- Conduct retesting to validate remediation and ensure closure.

Reports should highlight security gaps, API abuse risks, OWASP Top 10 vulnerabilities, and recommendations for improving fraud detection and transaction monitoring systems.

Automated Penetration Testing Tools and Techniques

Automated penetration testing plays a vital role in securing fintech applications that handle real money. These tools help identify vulnerabilities quickly, support continuous monitoring, and strengthen overall cybersecurity testing processes. By combining automated tools with manual testing, fintech organisations can detect risks early and maintain secure financial operations.

Tools such as OWASP ZAP, cloud security validation tools, and API security scanners are widely used across open banking platforms and fintech startups.

Popular Penetration Testing Tools

Automated penetration testing tools help security teams scan applications, networks, and payment systems efficiently. They enable faster vulnerability detection and support continuous fintech security testing.

These tools help organisations strengthen application security and maintain secure digital financial environments.

Key Areas to Test

Fintech apps handling real money require comprehensive testing across all critical components. Even a minor weakness can expose sensitive financial data or transactions.

Focus areas include:

- Payment gateway security and transaction validation

- User authentication and authorization controls

- APIs and backend service security

- Data encryption, storage, and transmission

- Transaction processing and workflow logic

Continuous vulnerability detection and monitoring help identify threats early and prevent potential breaches.Testing should also include fraud detection systems, real-time fraud detection, AML monitoring, machine learning models, blockchain technology integrations, and third-party APIs.

Integrating Tools into Your Security Workflow

Integrating automated penetration testing into development and deployment processes helps maintain consistent security across fintech applications.

Best practices include:

- Integrating security testing into CI/CD pipelines

- Using vulnerability monitoring tools continuously

- Combining manual and automated penetration testing

- Conducting regular security audits and reviews

- Maintaining compliance and security documentation

Ensure compliance with compliance frameworks, Money Services Business regulations, Money Transmitter Licenses, and financial industry standards for open banking and payment processors.

This approach strengthens application security and reduces long-term risks.

Best Practices for Fintech App Security

Maintaining strong fintech app security requires continuous monitoring, regular testing, and well-defined response strategies. Implementing best practices ensures secure transactions, protects financial data, and supports regulatory compliance.

Regular Security Audits

Routine security audits help fintech organisations identify and address vulnerabilities before they become critical threats.

Audits should include:

- Regular vulnerability assessment and testing

- Code reviews and static application security testing

- Payment gateway and transaction security checks

- Compliance and regulatory reviews

Frequent audits ensure systems remain secure and up to date.

Employee Training and Awareness

Human error remains one of the leading causes of security breaches. Educating employees about security practices significantly reduces risks.

Training should cover:

- Secure coding and development practices

- Data protection and privacy policies

- Phishing and social engineering awareness

- Incident reporting and response procedures

Well-informed teams contribute to stronger overall cybersecurity.

Incident Response Planning

Every fintech organisation must be prepared to respond quickly to potential security incidents.

Key elements include:

- Clear incident response framework and roles

- Rapid vulnerability detection and containment

- Communication and escalation protocols

- Recovery planning and compliance reporting

Integration of real-time fraud detection, transaction monitoring, AML monitoring, and machine learning-based fraud detection tools.

An effective response strategy helps organisations recover quickly while maintaining customer trust and regulatory compliance.

Conclusion

The importance of securing FinTech applications as they handle real transactions through a structured approach to security, as well as every rise in cyber threats targeted towards financial institutions; therefore, it is imperative that organizations make FinTech application security and protection of financial data, payment processing, API security, validate the security of the cloud and comply with the standards of PCI-DSS, part of their fintech security priority.

In addition, proper planning of penetration tests helps identify vulnerabilities earlier in the process to mitigate risks in terms of fraud, exploitation of APIs, or money laundering and strengthen the security posture of open banking platforms, mobile wallets, and third-party integrations of APIs.

Penetration testing should occur as part of the entire security lifecycle from pre-launch through major upgrades to before PCI audits to prior to investor due diligence. The combination of automated security assessments, ongoing vulnerability scanning, strong encryption, hardware security, the use of AI to tokenize sensitive information as well as real-time fraud detection will ultimately provide regulatory compliance, operational resilience and customer confidence within the entire FinTech Ecosystem.

People Also Ask (FAQs)

Q1.What is the difference between penetration testing and vulnerability assessment?

Ans: Penetration testing simulates real-world attacks to exploit vulnerabilities, while vulnerability assessment identifies and prioritises potential security weaknesses without exploitation.

Q2.How often should fintech apps undergo penetration testing?

Ans: Fintech apps should undergo testing at least quarterly, after major updates, and before launching new features that impact financial transactions or user data.

Q3.What are the most common vulnerabilities in fintech apps?

Ans: Common issues include insecure APIs, weak authentication, payment gateway flaws, misconfigured servers, and poor data encryption practices.

Q4.How can automated penetration testing benefit fintech companies?

Ans: Automated testing enables continuous monitoring, faster vulnerability detection, and seamless integration into development workflows, improving overall security posture.

Q5.What regulations should fintech companies be aware of regarding cybersecurity?

Ans: Fintech companies must comply with data protection and financial security regulations such as PCI-DSS, GDPR, and regional cybersecurity standards relevant to financial services.