Cross-border payments or international payments look simple from the outside. Money goes in, money comes out. But underneath that sits a fragile chain: payment gateways, foreign exchange engines, compliance layers, API-based bank connectivity, and real-time processing that has zero tolerance for inconsistency.

Fintech platforms like Stripe Payments, Papaya Global, and Crown Agents Bank handle thousands of these transactions daily across global payment networks. What most people don't see is how much can go wrong between initiation and settlement and how rarely standard QA catches it before production does.

We've spent years at Frugal Testing helping payment platforms find those gaps before users do. This is what actually breaks, and how to test for it properly.

Why Cross-Border Payment Systems Fail in Production

Most failures aren't bugs in a single system. They happen because five systems that each passed QA in isolation behave differently when they're all running together under load. Add ISO 20022 message standards, live foreign exchange rates, and multi-jurisdiction regulatory frameworks, and even small timing mismatches create real financial errors.

The patterns we see most often:

• Foreign exchange rate out of sync frontend cached, backend live, customer charged a different amount than quoted

• Settlement delays caused by payment gateway misconfigurations or bottlenecks in settlement layers

• Transaction monitoring breaking at system boundaries, not within any individual component

• Compliance checks including anti-money laundering and sanctions screening firing after the money has already moved

• Blockchain networks or smart contracts behave differently under load than in test environments

What Actually Shows Up in QA on Real Projects

FX inconsistency. Frontend pulls a cached rate, and the backend calculates from a live foreign exchange feed. The gap per transaction is small across thousands of payments on an e-commerce platform, it becomes a reconciliation disaster.

Duplicate charges. The API times out. The system retries. Nobody checked whether the original payment went through. The customer gets debited twice. This is a retry logic problem with no idempotency check and it surfaces late almost every time.

Fraud engine misfires. Real-time fraud detection built on machine learning and artificial intelligence looks fine in staging. In production, it starts blocking legitimate transactions or stops flagging suspicious ones. Almost always because the model wasn't tested against realistic transaction data patterns.

Compliance gaps. Sanctions screening is wired up but running after transaction initiation. By the time the check fails, money's already moved. Suspicious Activity Reports never get generated. This is the one that regulators notice.

What Makes This Type of Testing Hard

Everything Is Connected

One payment can touch a payment gateway, a payment hub, a SWIFT network, blockchain networks, and a core banking system each running its own protocol with its own failure behavior. Testing any one in isolation tells you almost nothing about how the whole thing behaves. Bugs live in the connections, not the components.

SWIFT gpi transactions add another layer of payment messages, end-to-end tracking across global payment networks, and ISO 20022 formatting that has to be exactly right. A single wrong field can stall an entire SWIFT payment with no obvious error message.

Transactions Don't Finish in a Straight Line

International payments settle asynchronously across Nostro accounts and intermediary banks. A transaction that looks complete on the issuing bank side might still be pending validation downstream. Your test suite needs to handle delays, out-of-sequence events, and partial completions not just scenarios where everything resolves cleanly in order.

Core Test Scenarios That Actually Matter

Currency Conversion & FX Validation

Don't just verify that a foreign exchange rate gets applied. Check when it's pulled, from which source, what rounding rules apply, and what happens when the rate changes between the quote and the transaction execution. That last scenario causes more reconciliation issues than most teams expect especially on payment platforms handling multiple payment methods simultaneously.

Payment Routing & Network Testing

When the primary route fails, where does the payment go? Fallback logic gets skipped during normal QA cycles and only shows up when something breaks in production. Also test SWIFT payments message formatting and for platforms using blockchain technology or smart contracts, validate behavior under network congestion, not just normal conditions.

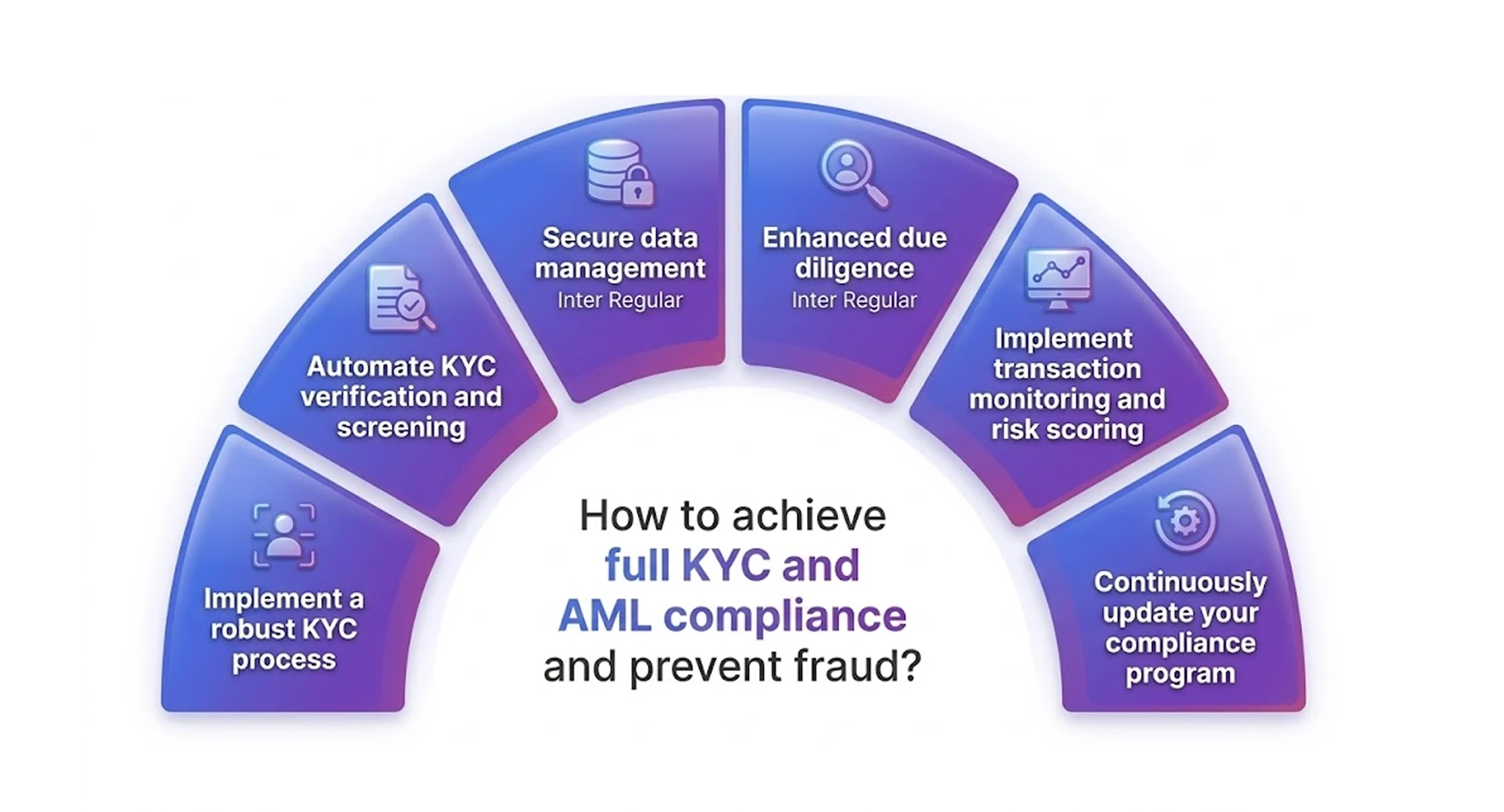

AML & KYC Testing Scenarios

This is where most compliance failures hide. It's rarely that checks aren't implemented it's that they run in the wrong sequence or at the wrong trigger point. Validate that anti-money laundering checks, beneficial ownership verification, adverse media screening, and sanctions list validation all fire before the transaction routes. Natural language processing is increasingly used for adverse media checks; test that too.

Regulatory reporting is another area that gets skipped. Suspicious Activity Reports need to be generated correctly, completely, and at the right point in the payment process not as an afterthought after regulatory pressure kicks in.

API & Integration Testing

Modern payment platforms are held together by APIs connecting merchant systems, payment processors, issuing banks, and third-party compliance engines. The easy stuff (does the endpoint return 200?) isn't where the problems are. The problem is what happens when a dependency returns 200 with malformed transaction data. Or when a timeout triggers a retry with no idempotency check. Or when API-based bank connectivity drops mid-session across customer devices.

Retry Logic & Idempotency

The most skipped area in payment QA, without question. If the same transaction gets submitted twice with the same idempotency key, the system should return the same result not create a second charge. We've seen this fail on fintech platforms processing instant payments more times than we can count. Test it explicitly, test it under load, and test it when the payment gateway is slow.

Security Testing

Security testing in payment systems goes beyond standard vulnerability scanning. Biometric authentication flows need to be tested across different customer devices and network conditions. Data exposure risks exist at every logging and error-handling layer. Cyber threats targeting payment platforms have grown more sophisticated testing needs to reflect that, including validation of privacy-enhancing technologies and federated learning models used for fraud detection

Performance Testing for High-Volume Transactions

Load Testing Payment Systems

Run your payment processor, payment hub, and APIs simultaneously under realistic transaction volumes not separately. Bottlenecks almost always appear at integration points between systems. Load and performance testing tools like JMeter and Gatling let you simulate the kind of concurrent traffic that e-commerce platforms and subscription-based SaaS services generate, including varied payment methods and transaction sizes.

Peak Load Scenarios

10,000 transactions spread across an hour is a completely different problem than 10,000 hitting in 90 seconds. Instant payments and real-time payments are particularly vulnerable here the systems designed for speed often haven't been tested for sudden volume spikes. End-of-month batch runs and flash sale traffic hit in bursts. Test the timing pattern, not just the total volume.

Latency & Failure Simulation

Deliberately kill dependencies mid-test. Slow down the foreign exchange service. Make the payment gateway unreachable. If your system hasn't been tested under failure conditions, you're assuming it recovers cleanly and that assumption is usually wrong in exactly the situations where being wrong costs the most. This includes simulating cyber threats and network disruptions that mirror real-world attack patterns.

Compliance Testing in Practice

PCI DSS Compliance Validation

Payment gateway PCI compliance and PCI DSS validation need to be tested at every point where card data is handled not just entry and exit. One misconfigured logging step can expose transaction data. Regulatory standards here are non-negotiable, and the testing has to match that seriousness.

Data Security and Privacy Testing

Data security and data privacy testing cover more ground than most QA teams' budgets. The California Consumer Privacy Act and equivalent global data privacy regulations don't throw runtime errors when you're non-compliant. Data security compliance means testing retention limits, access controls, and deletion workflows explicitly. Privacy-enhancing technologies and federated learning models used for fraud insights need their own validation paths. Data security law varies by jurisdiction your test scenarios need to reflect that variation.

Regulatory Compliance Validation

Financial compliance and regulatory compliance requirements change Base Erosion and Profit Shifting rules, regulatory announcements, updated sanctions lists. Your automated screening engine needs to be retested when the regulatory framework shifts, not just when the code changes. Regulatory reporting outputs including transaction monitoring logs and Suspicious Activity Reports should be part of your continuous integration testing suite.

Audit Trail Validation

We've worked with payment platforms where the audit trail looked complete but was missing entire transaction legs retries that fired but weren't logged, failures swallowed by error handlers. Every retry, every failure, and every status change needs to be captured accurately. Test your logs the same way you test your code including adversarial scenarios where multiple things fail simultaneously.

Real Cases From Fintech Projects

FX Mismatch-Reconciliation Breakdown

The frontend cached the exchange rate. The backend pulled live foreign exchange data. The gap was small per transaction across thousands of international payments, it became a reconciliation nightmare that took weeks to untangle. Caught during integration testing before it reached production. Platforms like Lucid Financials use AI-powered bookkeeping to catch these discrepancies post-transaction, but catching them in testing is cheaper and cleaner.

Duplicate Transaction Retry Without Idempotency

The payment platform resubmitted transactions on API timeout without checking prior completion. Customers were double-charged. Idempotency testing found it in QA. Nobody had written a test for the timeout-then-retry scenario because it 'never happens in staging.' It happened in production on day three

AML Failure Wrong Sequence

Anti-money laundering checks were implemented, but running after transaction initiation, not before. Payments were clearing before the automated screening engine completed sanctions screening. We mapped the payment process and identified the sequence gap, and the fix was a workflow change not new code. Scenario-based compliance testing is what was was found.

Tools We Actually Use

API & Integration

Postman and REST Assured for functional API validation not just response codes but transaction data accuracy, timeout handling, and retry behavior. WireMock to simulate banks, FX providers, and payment processors, which is the only reliable way to test failure scenarios when real dependencies are unpredictable. For continuous integration testing, these slot into CI pipelines cleanly alongside Playwright integration testing for end-to-end flows.

Performance

JMeter and Gatling for load simulation. Application performance testing tools like these aren't just for hitting TPS numbers the goal is replicating realistic traffic patterns: varied transaction sizes, concurrent calls to foreign exchange services and payment hubs, and timing intervals that match actual usage peaks. Web performance and load testing tools also help validate behavior across different network conditions and customer devices.

End-to-End

Selenium and Cypress for UI workflows. Backend validation covers ISO 20022 message formats, cross-system transaction data consistency, and async transaction status tracking across settlement layers. AML checks, sanctions screening, and regulatory reporting validation are inside the E2E scope not tested separately as a compliance afterthought.

How Frugal Testing Works

Our Approach

We don't split functional, performance, security testing, and compliance into separate tracks. Every transaction gets validated end-to-end from API call through payment gateway, settlement layers, reconciliation, and compliance check in one coordinated pass.

We test with real-world transaction data distributions, simulate third-party failures including payment processor outages and foreign exchange service delays, and treat financial compliance as part of the transaction flow rather than a checkbox at the end.

What We Actually Validate

• Foreign exchange calculation consistency across all system layers and payment methods

• API behavior under timeouts, retries, and failure conditions, including API-based bank connectivity drops

• Anti-money laundering, sanctions screening, and transaction monitoring in correct sequence, before routing

• Real-time fraud detection behavior under realistic transaction patterns not just clean test data

• Security testing across payment platforms, including biometric authentication and data exposure risks

• Audit trail completeness across all transaction states, including retries, failures, and regulatory reporting outputs

Why Teams Come to Us

Usually, after something broke in production that standard testing missed a reconciliation mismatch from an FX sync issue, a duplicate charge from bad retry logic, or a compliance gap that only appeared under load when the automated screening engine couldn't keep up with transaction volume.

We deliberately test for those failure conditions. And we work as part of the product team, not as a vendor running scripts against staging. The difference shows in what gets caught before go-live and what doesn't end up in front of a regulator.

What QA Teams Miss Most

Test the full lifecycle, not just success paths

Most production incidents happen in scenarios nobody wrote a test for the retry that fired twice on an instant payment, the async response from an intermediary bank that came back out of order, the partial completion that left transaction data in an inconsistent state across the payment hub. Cover those explicitly. Don't wait for customer expectations to expose them.

Make your test environment behave like production

Sanitized test data hides whole categories of bugs. Real payment gateway integrations, realistic transaction distributions across payment methods, and simulated banking APIs without those, your test environment is measuring something other than your actual system. Global dynamics and regulatory frameworks vary by region; your test data should reflect that variation.

Break things on purpose

Kill dependencies mid-test. Introduce latency on the foreign exchange service. Simulate cyber threats and network disruptions. If you haven't tested your payment platform under failure conditions, you're guessing about how it recovers. That guess is usually wrong in exactly the situations that matter most peak load on a global payment network or a regulatory audit where every transaction log gets scrutinized.

Conclusion

Honestly, most of the gaps we find aren't technical failures. They're testing failures payment process edge cases nobody thought to write a scenario for, compliance checks that looked right in isolation but ran in the wrong sequence, and real-time fraud detection that wasn't validated against the transaction patterns it would actually see.

If you're building or scaling a payment platform, we can help you find the blind spots before your customers or your compliance team does. Get in touch, and let's talk through where your current testing falls short.

People Also Ask (FAQs)

Q1.What is cross-border payment testing?

Ans: Validating that international payment systems process transactions accurately across currencies, regions, and systems APIs, gateways, FX engines, compliance checks, the lot. The tricky part isn't testing each component; it's testing how they behave together.

Q2.Why is compliance testing critical in cross-border payments?

Ans: Regulatory violations don't throw runtime errors. AML checks can be wired up and still run too late. Sanctions screening can pass unit tests and still miss real transactions. You need scenario-based testing to confirm compliance is actually working in the flow, not just present in the codebase.

Q3.What are the most common issues in cross-border payment systems?

Ans: FX mismatches between cached and live rates, duplicate transactions from bad retry logic, and compliance checks that run after the money's already moved. Almost all of them are integration problems, not individual component bugs.

Q4.How do you test high-volume and real-time payment systems?

Ans: Load testing with realistic transaction patterns not just volume, but timing. Spike tests that match actual usage peaks like end-of-month batch runs. The goal is behavior at integration points under realistic conditions, not clean-environment TPS numbers.

Q5.What are the best practices for testing cross-border payment systems?

Ans: Test end-to-end flows. Simulate failures deliberately. Use environments that behave like production. And stop treating compliance as a separate testing track it needs to be validated inside the transaction flow, not after it.