Unified Payments Interface (UPI), developed by the Reserve Bank of India, is a seamless and real-time digital payment transaction system. With its increasing global reach, UPI is now being integrated into international corridors through fintech companies and partnerships with global remittance apps, making cross-border money transfers faster, easier, and more secure.

This evolution supports the broader digital transformation in banking, where digital banking platforms, digital lending software, and UPI payment gateways are redefining financial services. Enhanced data security solutions and multi-factor authentication ensure that users benefit from safe, efficient, and scalable international fintech solutions.

💡What’s Next? Keep reading to discover:

🚀 How UPI enables seamless international transactions

🚀 Why security and compliance are critical in global transfers

🚀 Real-world UPI use cases in global money transfers

🚀 Key challenges in cross-border UPI adoption

🚀 How UPI and ULI together shape the future of global payments

What Is UPI in Digital Payments?

Unified Payments Interface (UPI) is a real-time digital payment system developed by the National Payments Corporation of India (NPCI) under the guidance of the Reserve Bank of India. It enables users to link multiple digital banking accounts to a single mobile application, offering instant money transfers 24/7.

UPI functions as a unified layer that connects fintech banks, merchants, and individuals, making it a key player in mobile digital payments. With its user-friendly interface, low transaction costs, and strong data security, UPI has become the backbone of India’s fintech solutions ecosystem.

Role of UPI in India’s Payment System

UPI plays a key role in transforming India’s digital payments landscape. It supports everyday transactions, empowers small businesses, and fuels innovation in the fintech and digital banking sectors.

- Driving financial inclusion - Small vendors and rural users can easily access digital banking platforms via UPI.

- Enabling seamless payments - QR codes and UPI payment gateways make peer-to-peer and merchant payments simple.

- Boosting fintech innovation - Powers services like digital lending platforms, fintech payments, and secure authentication.

- Strengthening data security - Uses multi-factor authentication and advanced data security software.

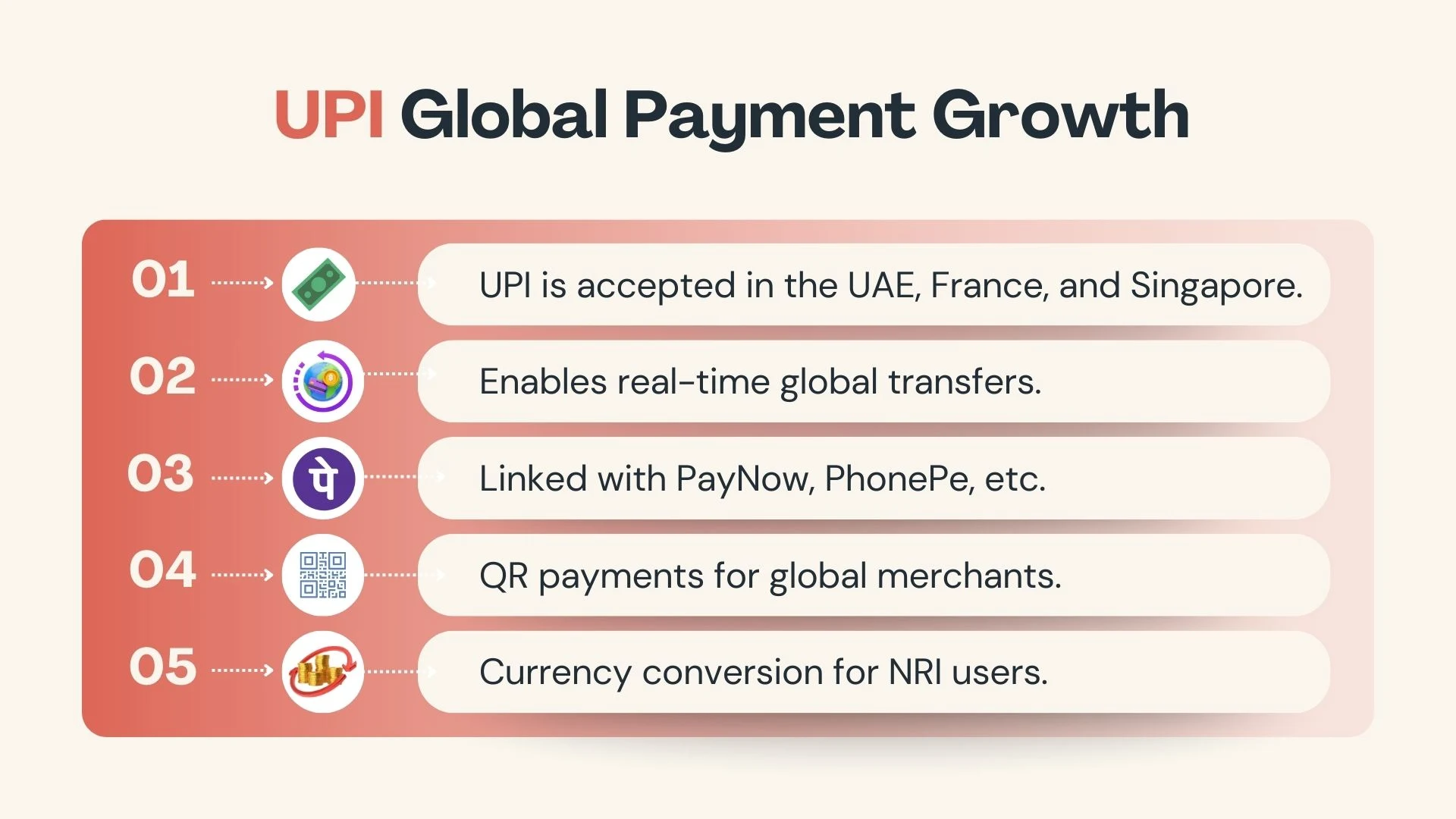

- Improving remittance access - Works with the best remittance apps for fast, cross-border transfers.

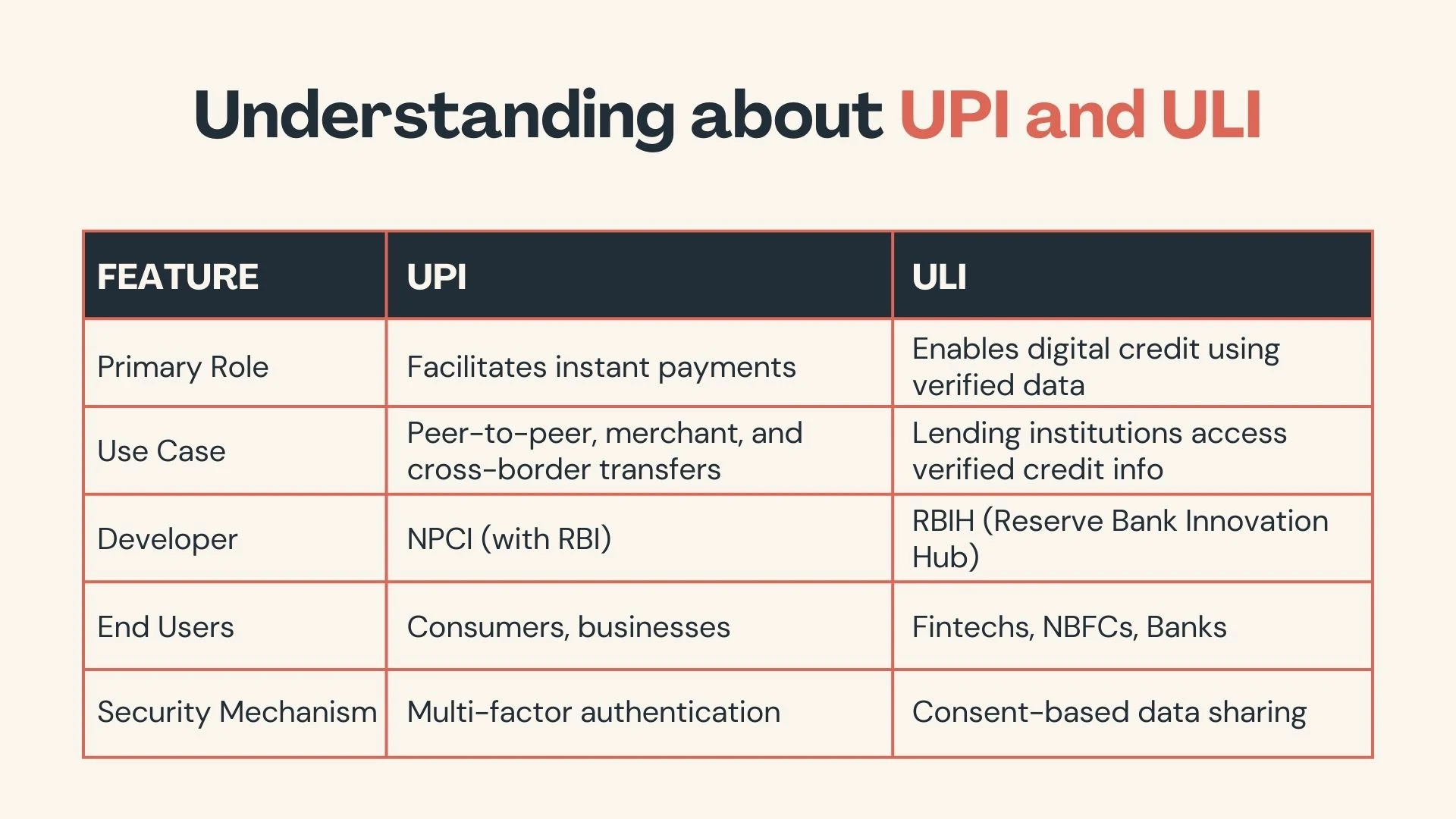

UPI and ULI: Powering Seamless Cross-Border Remittances

The collaboration between Unified Payments Interface (UPI) and Unified Lending Interface (ULI) is transforming cross-border remittances and digital credit services.

- UPI - Enables real-time, low-cost international money transfers via UPI payment apps and gateways, backed by strong data security services and multi-factor authentication.

Example: An Indian user sends money to a relative in Singapore using PhonePe, with instant transfer through UPI-PayNow integration, without needing SWIFT codes. - ULI - Developed by Reserve Bank Innovation Hub, ULI provides standardized API access to verified borrower data, helping fintech companies and digital lending platforms offer fast, consent-based credit.

Example: A digital lending app accesses borrower history via ULI APIs to quickly approve a microloan for a student in India, based on verified credit data.

Together, they create a secure and scalable solution for global fintech payments and lending, ensuring high-speed payments, improved credit access, and strong data security.

Techniques for Secure and Seamless UPI Remittances

To ensure global UPI remittances are both secure and smooth, a combination of advanced technologies and regulatory frameworks is used. These techniques not only safeguard transaction integrity but also enhance the speed and user experience for cross-border transfers.

Integration with Global Payment Gateways

The integration of the UPI payment gateway with global systems is transforming digital banking and remittance app experiences. It simplifies UPI payment for international use while ensuring security and compliance with Reserve Bank of India standards.

1. Cross-Border UPI Connectivity

- Linked with international platforms like PayNow (Singapore) and QRIS (Indonesia).

- Users make global UPI payments using a UPI payment app and VPAs.

2. Simplified Transfer Process

- Eliminates the need for SWIFT codes and complex banking info.

- Transfers via digital banking platforms using only phone numbers or VPAs.

3. Enabling Fintech and Lending

- Helps fintech companies and fintech banks expand internationally.

- Supports digital lending software integration using ULI, regulated by RBI.

- UPI payment limit compliance is also maintained during cross-border transactions.

4. Strong Data Protection

- Enforces secure authentication and multi-factor authentication.

- Ensures compliance with data security solutions and protects against data security breaches.

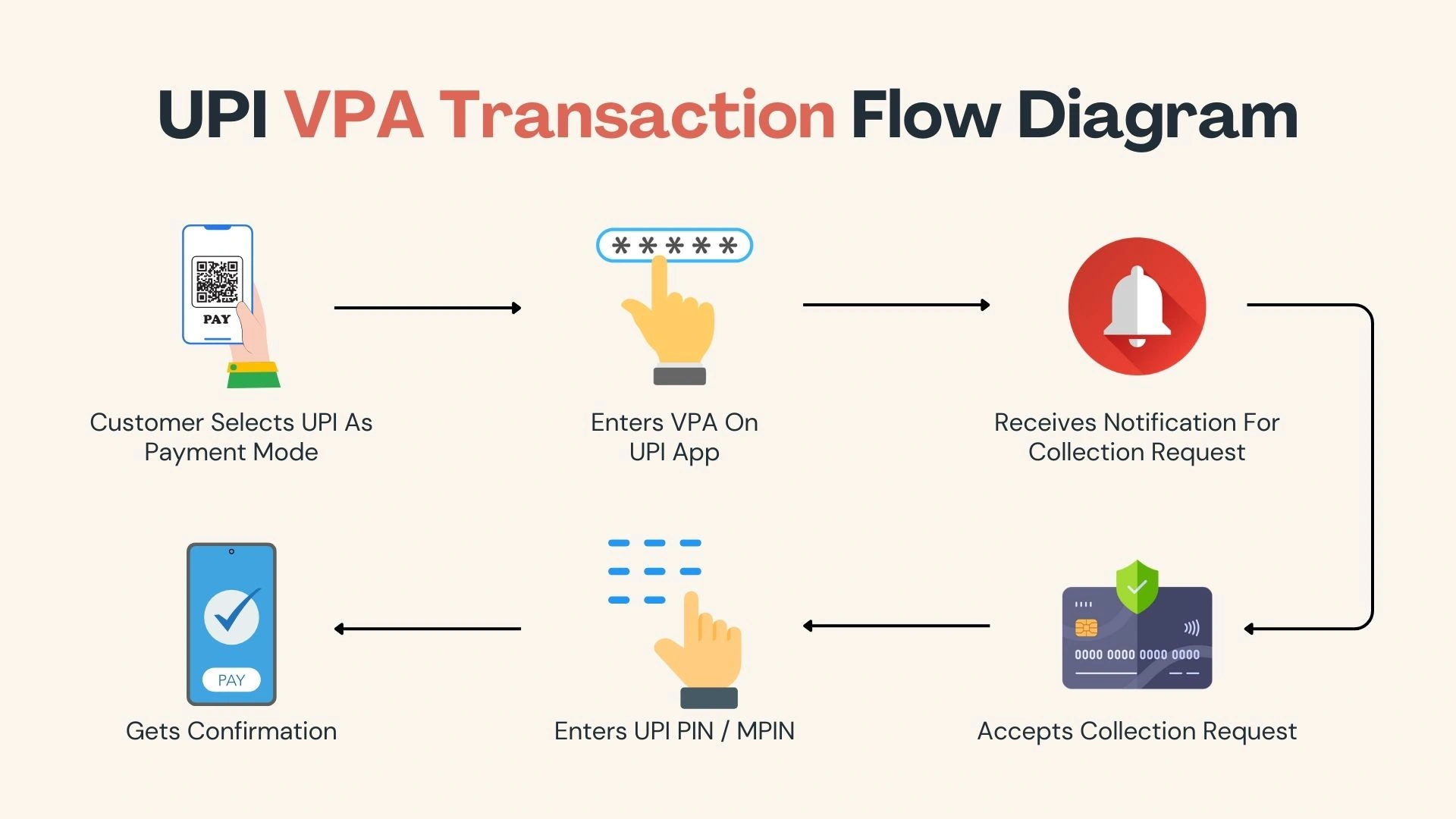

Use of Virtual Payment Addresses (VPAs)

Virtual Payment Addresses (VPAs) simplify payment processing by replacing sensitive bank information with secure aliases. For fintech and digital lending platforms, VPAs streamline bulk transactions, invoicing, and vendor payments through UPI payment apps.

1. Easy Setup for Businesses

- Businesses can create VPAs linked to corporate bank accounts.

- Enables faster digital payments across platforms without revealing bank details.

2. Efficient Invoicing and Reconciliation

- Each client or vendor can be assigned a unique VPA.

- Reduces errors and supports automated digital banking solutions.

3. Scalability for Fintech and Lending Firms

- VPAs power bulk payouts and refunds in fintech payments and digital lending.

- Smooth integration with digital lending software and UPI payment gateway.

4. Regulatory Compliance and Security

- Aligned with Reserve Bank of India (RBI) and ULI protocols.

- Enhances data security with reduced exposure to account credentials.

Multi-Factor Authentication for Transactions

Multi-Factor Authentication (MFA) is critical for secure UPI payment processing and digital transaction authorization. For fintech companies, digital lending platforms, and remittance apps, it ensures only authorized personnel can approve high-value or bulk payments.

1. Strengthens the Authentication Process

- Combines password, OTP, biometrics, or tokens.

- Prevents unauthorized access, reducing data breach risks through continuous security testing.

2. Required for High-Risk Digital Lending Transactions

- Mandatory for sensitive operations in digital banking platforms.

- Enhances trust for B2B users and clients using digital lending software.

3. Regulatory Compliance with RBI

- Aligns with the Reserve Bank of India’s guidelines for strong authentication.

- Essential for fintech solutions handling bulk remittances.

4. Secures UPI Payment Gateway Integrations

- MFA adds a strong security layer to UPI payment gateways.

- Encourages adoption among users seeking secure digital payments.

Real-Time Settlement Systems

Real-Time Settlement Systems ensure funds are transferred instantly, enhancing cash flow visibility and operational efficiency for companies using UPI payment infrastructure.

1. Faster Payment Processing for Transactions

- Enables real-time vendor payments and salary disbursals via UPI payment apps.

- Ideal for high-volume digital payments in fintech ecosystems.

2. Improved Cash Flow Management

- Businesses receive funds instantly, improving liquidity.

- Supports precise reconciliation for digital banking operations.

3. Enhances Fintech and Lending Platforms

- Critical for fintech banks and digital lending platforms to disburse loans or process repayments in real time.

- Reduces friction in remittance cycles.

4. Supports RBI’s ULI-Based Architecture

- Complies with RBI’s Unified Lending Interface (ULI) strategy for faster settlements.

- Drives seamless integration across fintech solutions and mobile digital payments.

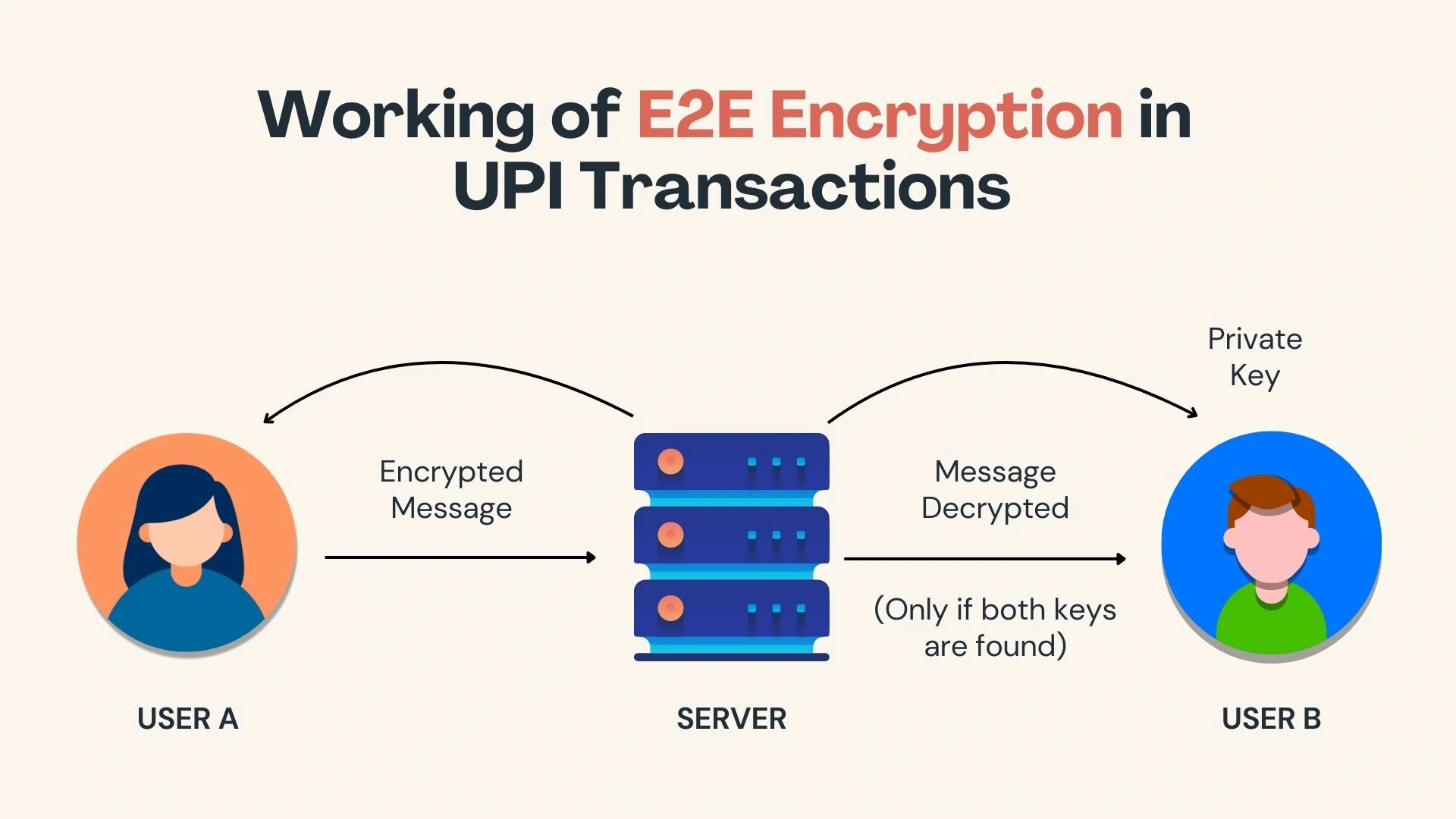

End-to-End Encryption and Data Security

End-to-End Encryption (E2EE) secures every UPI transaction, ensuring sensitive business data stays protected across the digital economy.

1. Secures Sensitive Financial Data

- Transaction details are encrypted using E2EE, preventing breaches in QR payments and UPI transactions.

- Essential for digital lending and fintech security amid rising transaction volume.

2. Ensures Trust in Remittance Apps

- Encrypts payment data and metadata in bank wires and UPI payment apps.

- Boosts client trust through seamless transaction experiences.

3. Reduces Risk of Data Security Breach

- Protects against fraud and man-in-the-middle attacks with transaction limits and financial savings.

- Multi-factor authentication adds another security layer.

4. Compliance with RBI and Global Data Standards

- Aligns with RBI and global data rules, meeting facilitating conditions.

- Required for fintech and digital banking platforms, ensuring payment efficiency.

Real-World UPI Use Cases for Global Transfers

Driven by the Reserve Bank of India and rising fintech companies, UPI payments are streamlining digital payments across borders. With secure UPI payment gateways, remittance apps, and robust data security solutions like multi-factor authentication, global users benefit from faster and safer mobile digital payments.

This marks a major step in the digital transformation in banking through innovative digital lending platforms and digital banking solutions.

1. India - Singapore UPI - PayNow Link

The India-Singapore UPI payment and PayNow linkage marks a milestone in real-time global UPI transactions and financial transactions. This partnership, backed by the Reserve Bank of India and the Monetary Authority of Singapore, strengthens the digital economy and supports cashless transactions for individuals and businesses through reliable payment platforms.

How It Works:

- Users in India send money to Singapore using a UPI application and just the recipient’s mobile number or UPI ID.

- Transactions are instant, 24/7, settled in local currencies via secure APIs and mobile wallets.

- Security features include two-factor authentication, UPI PIN, and data security using RBI’s Unified Lending Interface (ULI).

2. UPI Acceptance in UAE & France

To simplify cross-border travel and shopping, India has enabled UPI cross-border payments in countries like the UAE and France. This improves financial savings and supports the banking system through global mobile payment integration and user-friendly design.

How It Works:

- Indian tourists use QR code-based payments by scanning merchant codes abroad via UPI apps like PhonePe or Google Pay.

- Merchant networks such as NeoPay (UAE) and Lyra (France) serve as payment facilitators in QR payment systems.

- Ensures seamless transaction experiences with biometric verification, fraud risk monitoring, and IFSC codes for tracking.

3. Project Nexus - Global Interoperability

Project Nexus is a multilateral effort interlinking real-time systems like UPI, ensuring global wire transfers, credit card alternatives, and reduced transaction limit stress. It enables international financial management and boosts mobile banking adoption.

How It Works:

- Offers a single interoperable banking platform for multi-country settlements using Application Programming Interfaces.

- Integrates one-time passwords, Artificial Intelligence, Machine Learning, and customer support systems.

- Lowers costs, improves UPI app reliability, and promotes consumer adoption with support for bill payment services and enhanced security measures.

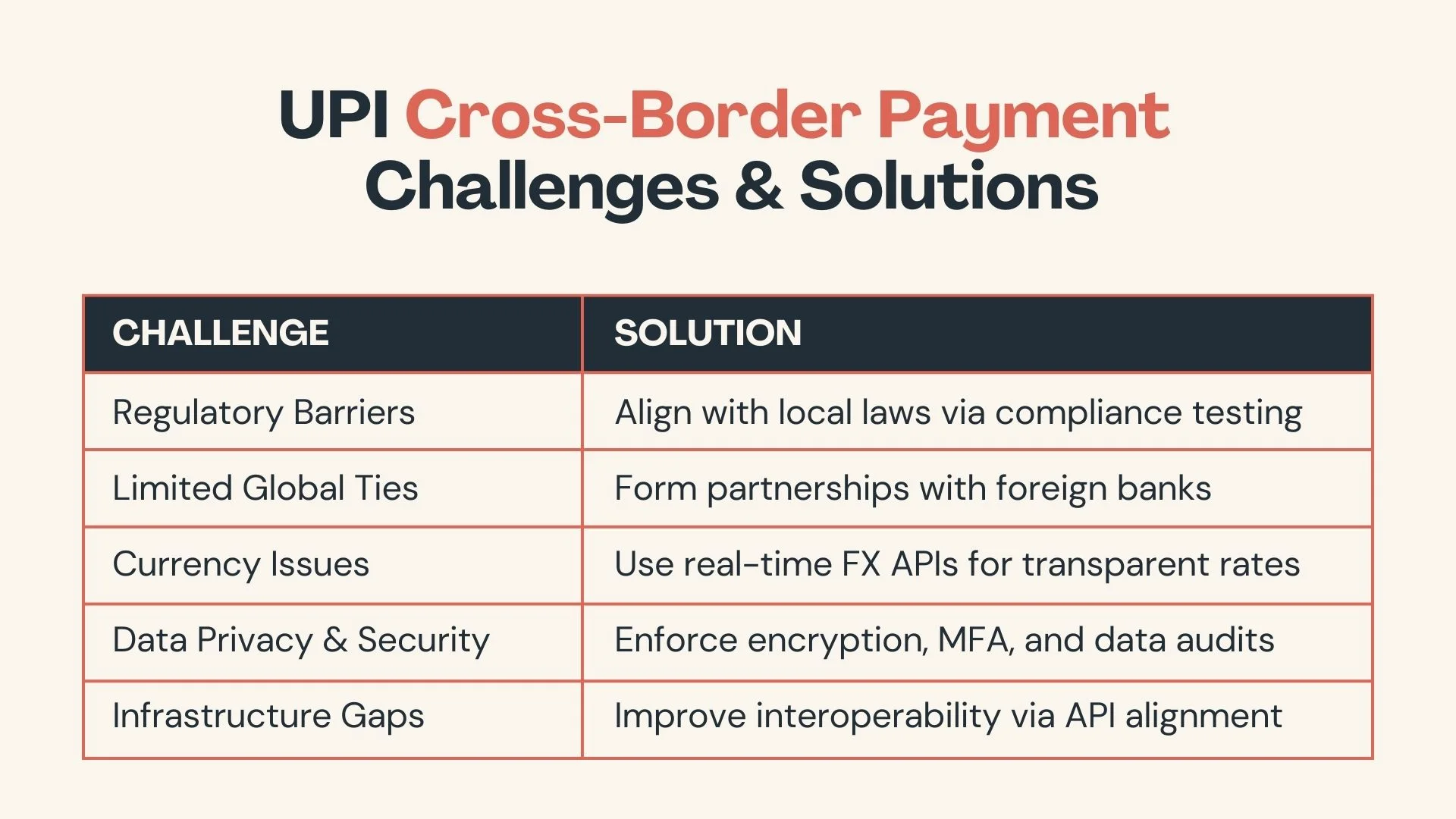

Challenges of Using UPI for International Transfers

While UPI cross-border payments are gaining momentum, extending their usage for global money transfers presents several challenges. These issues affect users, fintech providers, and digital banking platforms aiming to scale internationally.

- Regulatory and Compliance Barriers

Each country follows its regulatory framework for digital banking platforms, foreign exchange, and transaction monitoring. Aligning UPI with these diverse rules and the RBI Unified Lending Interface is a complex process. - Limited Global Partnerships

UPI’s expansion depends heavily on partnerships with international banks and regulators. Without widespread adoption or bilateral integration, UPI cross-border payments remain limited. - Currency Conversion Issues

Global money transfers often face exchange rate fluctuations and additional conversion fees, reducing the transparency and speed of UPI-based international transactions. - Security and Data Privacy Risks

Digital payments across borders raise concerns around data handling and fraud prevention. Ensuring international compliance with data protection rules is critical when using UPI cross-border. - Lack of Unified Global Infrastructure

In the absence of a standardized global payment system, syncing UPI with other countries platforms is difficult. Interoperability gaps slow down the adoption of the RBI Unified Lending Interface for global money transfers.

Conclusion: UPI and ULI Power Global Payments

UPI and ULI are simplifying international payments by offering fast, secure, and user-friendly transactions. Their integration is making cross-border money transfers more efficient, benefiting individuals, businesses, and financial institutions through greater transparency, lower processing times, and access to add-on services.

As adoption grows across countries, UPI and ULI are paving the way for a more inclusive and connected digital payment ecosystem. This progress supports global financial accessibility and boosts the growth rate of seamless international trade, travel, and remittances for users worldwide.

Frugal Testing, a leading SaaS application testing company, is renowned for its specialized AI-driven test automation services tailored to meet the evolving needs of modern businesses. Among the comprehensive services offered by Frugal Testing are advanced Fintech Software Testing Services, designed to ensure security, performance, and compliance in financial applications. The company also provides cloud-based test automation services, enabling scalable, efficient, and cost-effective testing solutions.

People Also Ask

👉 Can we register on UPI with an international number?

No, currently UPI registration requires an Indian mobile number linked to an Indian bank account. International numbers are not supported yet.

👉How does UPI integrate with foreign banking APIs for remittances?

UPI integrates with global banking systems through the Unified Lending Interface (ULI) and secure APIs that enable cross-border remittance flows efficiently.

👉How is the exchange rate calculated for UPI-based international transfers?

Exchange rates are calculated using real-time currency conversion data provided by partner banks or remittance platforms, often including nominal service fees.

👉What encryption protocols are used in UPI transactions?

UPI uses robust end-to-end encryption (E2EE), Transport Layer Security (TLS), and secure authentication tokens to ensure safe and encrypted data transfers.

👉Are there any limits on international remittances using UPI and ULI?

Yes, UPI and ULI transactions are subject to RBI regulations and partner bank limits, which define daily and per-transaction caps for remittances.