PCI DSS compliance is one of the most common reasons card program launches get delayed. Even when the product is technically ready, gaps like incomplete security validation, weak access controls, or missing audit evidence can bring everything to a halt at the final stage. This guide explains how to ensure PCI DSS compliance before go-live, covering required security testing, common audit failures, and a practical checklist to help you pass certification without delays.

In practice, most delays don’t come from broken features. They happen when compliance is treated as a final step instead of a parallel process. Teams often move quickly on engineering and UX, only to face avoidable audit findings that push timelines back by weeks. The difference comes down to preparation structured testing, audit-ready documentation, and continuous validation. When handled correctly, PCI DSS becomes a predictable part of the launch process rather than a bottleneck.

What You’ll Learn in This Guide

- Why PCI DSS compliance matters for card program launches

- What PCI DSS testing actually covers

- Common audit failures that delay go-live

- A practical PCI DSS compliance checklist

- Timeline for PCI readiness before launch

- Implementation strategies for audit success

Why PCI DSS Compliance Is Critical Before Card Program Launch

PCI DSS testing becomes critical before go-live because it’s the last line between a compliant launch and a costly delay. Most failures don’t come from obvious bugs they come from gaps in encryption, access control, or incomplete audit evidence that only surface during formal assessment. Without structured pre-launch testing, these issues remain hidden until a QSA flags them, forcing rework under time pressure. That’s where timelines slip, releases get blocked, and teams realize too late that compliance isn’t a post-check it’s a prerequisite.

Treating PCI DSS testing as part of the release process changes the outcome entirely. When encryption, segmentation, API security, and monitoring are validated early and continuously there’s no last-minute scramble to fix critical findings. Instead of reacting to audit failures, teams enter assessments audit-ready, with clear evidence and zero high-risk gaps. That shift is what separates delayed launches from smooth go-lives.

What Happens When Compliance Fails at Launch (Real Scenarios)

Here's a scenario that plays out more often than people admit: a fintech startup finishes development on a prepaid card program, passes internal QA, and submits for PCI DSS certification a week before their scheduled launch. The Qualified Security Assessor (QSA) finds unencrypted PANs (Primary Account Numbers) cached in application logs and misconfigured network segmentation between the cardholder data environment and a shared dev server.

Launch gets postponed. The fix takes three weeks. The PR hits before the fix is confirmed.

A second, more dangerous version: the launch proceeds anyway, the vulnerability gets exploited, and cardholder data leaks. That's not hypothetical in 2019, a payment processor's breach exposed 100 million card applications because of a misconfigured web application firewall (WAF). The root cause was a cybersecurity vulnerability that a proper pre-launch security testing pass would have caught.

Business Impact: Launch Delays, Penalties, and Reputational Damage

The PCI Security Standards Council doesn't publish a fixed penalty schedule, but card brands do. Visa and Mastercard can levy fines ranging from $5,000 to $100,000 per month for non-compliance, and those costs fall on the acquiring bank, which then passes them downstream to you. Beyond fines, you lose the right to process card payments until remediation is confirmed.

Reputational damage is harder to quantify but easier to understand. Customers don't read audit reports, but they do read breach notifications.

What PCI DSS Testing Actually Covers in Card Programs

Validating Data Protection, Encryption, and Storage Controls

PCI DSS 4.0 tightened requirements around how cardholder data is stored, transmitted, and protected. The core question during testing: where does card data actually live, and is it protected at each point?

This means validating:

- That PANs are rendered unreadable in storage (truncation, tokenisation, or encryption with proper key management)

- TLS 1.2 minimum for data in transit TLS 1.0 and 1.1 are out

- That encryption keys are stored separately from the encrypted data and rotated on a defined schedule

A vulnerability scan here isn't just running a tool. It's tracing the card data flow from the moment a user enters their card number through every system that touches it application layer, database, backup, log files, and third-party integrations.

Access Control, Authentication, and Role-Based Restrictions

PCI DSS covers who can access cardholder data and under what conditions. During testing, I look at whether access is genuinely least-privilege or just labeled that way.

Common failures: a developer account that still has production database read access from a project six months ago, or a shared admin credential used across three services with no audit trail on who used it when.

PCI DSS 4.0 also requires multi-factor authentication for all access into the cardholder data environment (CDE). If you're not testing MFA enforcement before launch, you're going to find it during your QSA assessment.

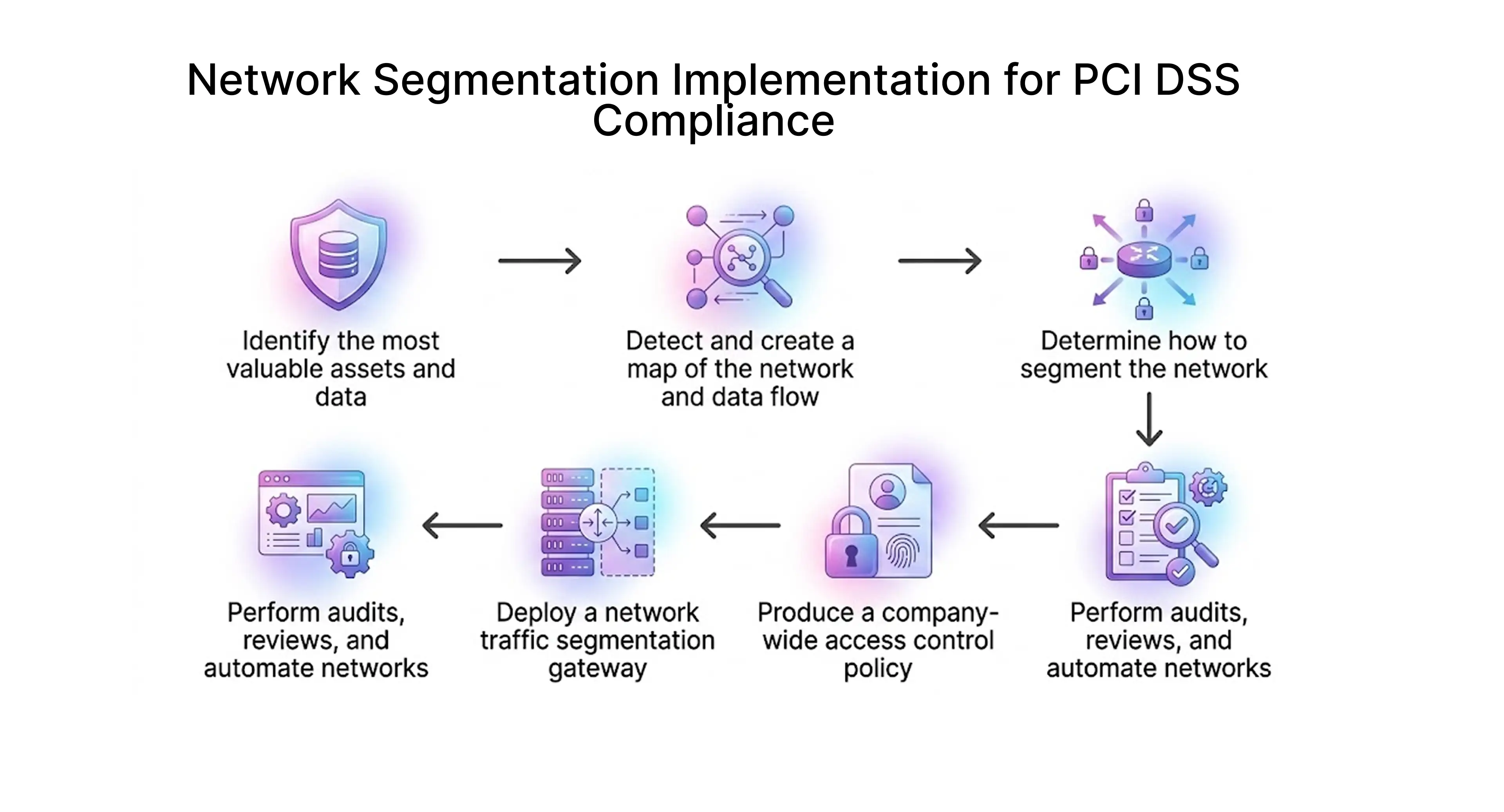

Network Security, Segmentation, and Traffic Monitoring

Network segmentation is one of the most frequently misconfigured areas in card programs. The goal is to isolate the CDE from everything else dev environments, analytics systems, third-party tools so that a breach in one area can't reach cardholder data.

Testing this means confirming that firewall rules across next-generation firewalls like Palo Alto Networks firewalls, Cisco firewalls, or cloud-native security groups actually enforce segmentation as intended. It’s not enough for rules to exist; traffic flows must align with documented segmentation policies.

In real-world environments, organizations often document perfect segmentation but overlook gaps introduced during urgent fixes. A commonly observed issue is an open port added during a late-night hotfix that never gets closed. These small misconfigurations can silently break compliance boundaries.

This is exactly why PCI DSS continuous testing is critical. A one-time validation at launch cannot detect configuration drift that occurs days or weeks later especially in dynamic environments where firewall rules and access controls frequently change.

Network security also covers traffic monitoring. Remote monitoring and alerting on CDE traffic needs to be active and configured to flag anomalies not just enabled in theory. If you're not running PCI DSS compliance automation across your segmentation and monitoring controls, you're relying on humans to manually catch gaps that automated pipelines would surface in minutes.

Mapping PCI DSS Requirements to Test Cases and Validation Layers

Every PCI DSS requirement should map to at least one test case. This sounds obvious. In practice, most teams have application security testing coverage and very little infrastructure or configuration validation coverage.

Build a traceability matrix: PCI DSS requirement → control implemented → test case → test result → evidence collected. That matrix is what your QSA is going to walk through during the audit.

PCI DSS Testing Checklist Before Go-Live

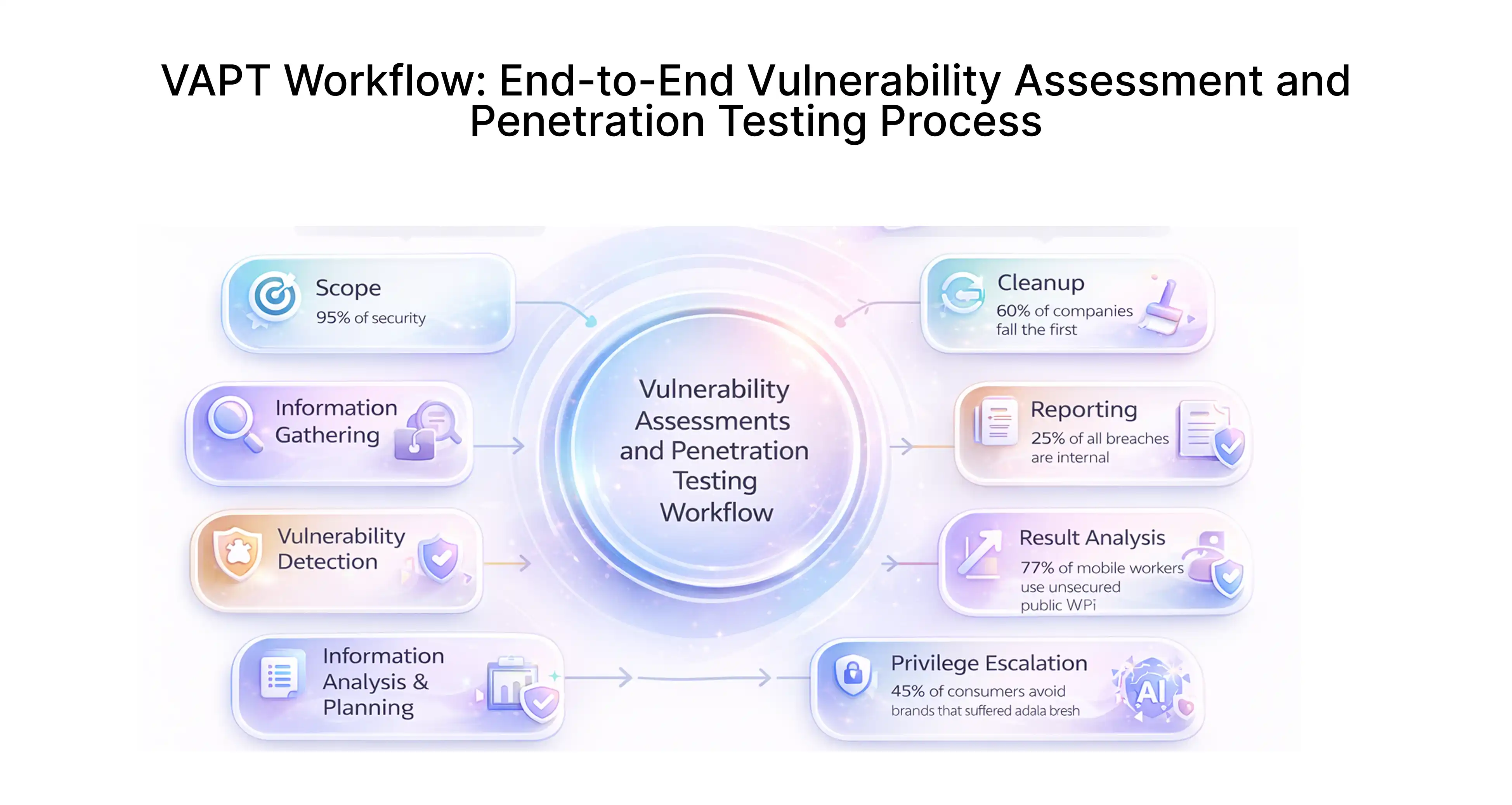

Vulnerability Assessment and Penetration Testing (VAPT)

PCI DSS mandates both internal and external vulnerability scanning (using an Approved Scanning Vendor for external scans) and annual penetration testing. For a card program launch, you want this done before go-live, not scheduled as a post-launch activity.

Vulnerability scanning tools flag known CVEs and misconfigurations. Penetration testing cyber security penetration testing specifically focused on your CDE and card workflows goes further: it's a human (or a team) trying to actually exploit what the scanner found, plus looking for logic flaws the scanner won't catch.

A web vulnerability scanner will catch issues like outdated libraries, open admin interfaces, or headers that expose server details. A penetration tester will take that outdated library and demonstrate whether it's exploitable in your specific environment.

Application and API Security Testing for Card Workflows

Card programs run on APIs. Issuing a card, checking a balance, processing a transaction, disputing a charge all API calls. API security testing needs to cover each of these workflows explicitly.

That means testing for:

- OWASP API Top 10 vulnerabilities (broken object-level authorisation is particularly nasty in card contexts can User A access User B's card data?)

- Input validation on card number fields, expiry, CVV handling

- Rate limiting on sensitive endpoints (how many times can someone try a PIN before you lock them out?)

- Token expiry and refresh handling

An API security testing tool helps automate coverage, but card workflow logic requires manual test cases too. The automated tool won't know that your balance inquiry endpoint shouldn't return the full PAN in the response a human tester will.

Infrastructure and Configuration Validation (Cloud + On-Prem)

Whether your CDE runs on AWS, Azure, GCP, or on-prem, infrastructure configuration needs explicit validation. Cloud environments create a false sense of security the platform is secure, but misconfigured services are your problem, not theirs.

For cloud environments, I check:

- S3 buckets (or equivalent) that might contain card data are they private?

- Security groups: are any production CDE instances reachable from 0.0.0.0/0?

- IAM roles: are any roles over-provisioned?

- Encryption a

- t rest: are EBS volumes, RDS instances, and backups encrypted?

For Kubernetes environments, Kubernetes vulnerability scanning is worth running separately container images, RBAC configurations, and network policies all need review. A misconfigured Kubernetes cluster that allows lateral movement into the CDE is a critical finding.

Logging, Monitoring, and Alert Validation

PCI DSS covers audit logs. Every access to cardholder data, every administrative action, every failed login attempt needs to be logged, stored securely, and reviewed.

Testing this means:

- Confirm that logging is actually enabled and capturing the right events

- Confirm that logs are shipped to a centralized, tamper-evident system

- Confirm that logs are retained for 12 months (3 months immediately available)

- Confirm that security monitoring and alerting is configured and tested trigger a known-bad action and verify an alert fires

Security monitoring that's deployed but never tested is worse than you think. I've seen SIEM dashboards that look active but haven't ingested CDE logs in weeks because a config change broke the pipeline and nobody noticed

Critical PCI Compliance Gaps Found During Testing

Weak Encryption, Key Management, and Data Exposure Risks

The most common finding: encryption is present, but key management is broken. Keys stored in environment variables in plaintext, keys rotated manually on an ad hoc basis, or the same key used for years across multiple environments.

PCI DSS 4.0 requires documented key management procedures, including rotation schedules, split knowledge/dual control for key custodians, and secure key storage. If your testing doesn't specifically validate key management, you'll find this gap in your QSA audit instead.

Misconfigured Access Controls and Excessive Privileges

Access creep is real. An account that needs temporary elevated access for a project gets it, the project ends, the access stays. Testing with a proper access review not just documenting what access should exist, but querying what access actually exists consistently turns up accounts with more privilege than they need.

Missing or Ineffective Logging and Monitoring Mechanisms

Logging is checked during implementation and then forgotten. By the time a card program reaches launch, log pipeline configurations have often drifted from what was originally tested. Remote monitoring tools may be in place but not actively covering the CDE.

I always test logging end-to-end: perform a test action, confirm it appears in logs, confirm the log is in the centralized system, confirm the timestamp and content match. It's tedious. It catches real gaps.

Third-Party and Payment Processor Risks

Your PCI DSS scope includes your payment processor integrations, your card network connections, and any third-party service that touches cardholder data. A misconfigured webhook from your payment processor, or a third-party analytics tool that accidentally captures card numbers in form data, creates a compliance gap that's entirely your problem even though it involves someone else's code.

Test every integration point. Confirm data flows are documented. Confirm third parties are themselves PCI compliant and can provide their Attestation of Compliance (AOC).

PCI DSS Requirements Overview

Key PCI DSS Controls for Card Programs

Before a card program goes live, compliance isn’t about ticking boxes it’s about proving that sensitive data is protected across its entire lifecycle. The most critical control areas include:

Data Protection and Storage

Cardholder data must never be stored in plain text. Encryption, tokenization, and strict data retention policies are essential to ensure that Primary Account Numbers (PAN) remain unreadable even if systems are compromised.

Access Control and Authentication

Only authorized users should have access to cardholder data environments. This involves role-based access, least privilege enforcement, and strong authentication mechanisms such as multi-factor authentication (MFA).

Logging and Monitoring

Every interaction with sensitive systems must be traceable. Centralized logging, real-time monitoring, and tamper-proof audit trails are necessary to detect anomalies and support forensic investigations.

Security Testing and Validation

Continuous validation through VAPT, vulnerability scanning, and configuration reviews ensures that security controls are not just implemented but are actually effective under real-world conditions.

These control areas collectively form the foundation of any PCI DSS compliance checklist and directly influence audit outcomes.

Common PCI DSS Audit Failures Before Launch

Even well-prepared teams fail audits due to gaps in execution, not intent. The most frequent issues seen during PCI DSS audit preparation include:

Unencrypted Card Data in Logs

Sensitive data often leaks into application or server logs due to improper masking or debugging practices one of the fastest ways to fail an audit.

Weak Key Management Practices

Encryption is only as strong as the way keys are handled. Poor rotation policies, insecure storage, or lack of access controls around keys create critical vulnerabilities.

Improper Network Segmentation

If the cardholder data environment (CDE) is not isolated correctly, the scope of compliance expands unnecessarily making audits more complex and failure more likely.

Missing MFA Enforcement

Multi-factor authentication is often inconsistently applied, especially for internal systems, admin panels, or third-party access points.

Incomplete Logging Coverage

Gaps in logging whether from misconfigured tools or unmonitored systems result in blind spots that auditors immediately flag.

Addressing these early through structured card program security testing significantly reduces last-minute compliance risks.

PCI DSS Compliance Timeline Before Go-Live

A structured timeline is what separates reactive teams from audit-ready organizations. A typical PCI DSS compliance checklist for launch readiness follows this sequence:

T–60 Days: Initial Security Testing

Conduct full-scope VAPT and vulnerability assessments across applications, APIs, and infrastructure. This phase identifies foundational security gaps.

T–30 Days: Remediation and Re-Testing

Fix identified vulnerabilities and validate them through targeted re-tests. This is where most compliance risks are actually resolved.

T–15 Days: Final Validation

Perform a final round of PCI DSS testing services to ensure no regressions or overlooked issues remain.

T–7 Days: Evidence Compilation

Prepare audit artifacts logs, test reports, access control records, and policy documents. Evidence quality often determines audit success.

T–1 Day: Final Compliance Check

Run a last-mile verification across all systems to confirm that controls are active, monitored, and properly documented.

This timeline not only improves audit readiness but also aligns teams around a predictable and repeatable compliance process.

Pre-Go-Live PCI Testing Checklist (Audit-Focused)

Environment Readiness and Segregation Validation

- CDE boundary is defined and documented

- Network segmentation confirmed via firewall rule review and penetration test

- Dev/test environments are fully separated from production CDE

- All types of firewalls and network controls are reviewed and confirmed active

- Wireless networks (if any) are isolated from CDE

Test Coverage Across All Card Data Flows

- Card issuance flow tested end-to-end

- Transaction processing flow tested

- Dispute and chargeback flow tested

- Card data storage validated (no unencrypted PANs in logs, databases, or backups)

- All API endpoints included in security testing scope

Evidence Collection for Audit (Logs, Reports, Screenshots)

- Penetration test report (internal and external) with remediation tracking

- Vulnerability scan results from ASV (external) and internal scans

- Access control review documentation

- Encryption and key management procedures

- Log samples demonstrating required event capture

- Third-party AOCs

Remediation Validation and Re-Testing

- All critical and high findings remediated

- Re-test performed and documented for each remediated finding

- No open critical vulnerabilities at go-live

- Risk acceptance (if any) formally documented and signed off

Embedding PCI Compliance Into QA and Release Workflows

Shifting Compliance Validation Left in SDLC

The earlier you find a compliance issue, the cheaper it is to fix. A PAN stored in application logs discovered in development takes a day to fix. The same issue found by a QSA during your certification audit takes weeks and delays your launch.

Shift left means: add security and compliance checks into your development pipeline, not just your pre-launch certification process. That includes code review for data handling patterns, static analysis for security anti-patterns, and developer training on what can and cannot touch cardholder data.

Automating Security and Compliance Test Cases

Some PCI controls lend themselves to automation in a CI/CD pipeline:

- Secrets scanning (confirm no credentials committed to source control)

- Dependency vulnerability scanning (flag known CVEs in libraries)

- Infrastructure-as-code scanning (Terraform/CloudFormation misconfigurations)

- DAST scans triggered on each deployment to staging

Automating these doesn't replace penetration testing or your QSA assessment, but it catches regressions between formal testing cycles.

If you're running Kubernetes, integrate continuous security checks directly into your deployment pipeline. This includes using Kubernetes monitoring tools to track cluster behavior, detect anomalies, and validate policy enforcement in real time. At the same time, embed vulnerability scanning so every new container image is assessed before it reaches production.

This approach ensures that both runtime visibility and pre-deployment security are covered. It reduces the risk of misconfigurations or vulnerable workloads slipping into live environments.

Continuous Validation Across Releases and Updates

PCI DSS compliance isn't a one-time certification. Every release that changes the CDE or affects cardholder data flows requires re-validation of the affected controls. Build that into your release process explicitly not as a retrospective audit, but as a go/no-go gate.

Final Go-Live Readiness for PCI Compliance

Final Validation Across Systems, APIs, and Integrations

The week before launch, run a final sweep:

- Confirm all vulnerability management findings are resolved or formally accepted

- Re-run automated scans and confirm no new issues introduced since last formal test

- Validate all third-party integrations one more time configuration drift happens

Internal Sign-offs and Audit Readiness Checks

Your QSA will ask for evidence. Compile it before launch so you're not scrambling:

- System inventory for CDE scope

- Data flow diagrams showing cardholder data movement

- Network diagrams showing segmentation

- Policy documents (PCI DSS policy, access control policy, incident response plan)

- All test reports with remediation tracking

Ensuring Zero Critical Vulnerabilities Before Launch

This is non-negotiable. No open critical vulnerabilities at go-live. High vulnerabilities require a documented remediation plan with a timeline. Medium and low findings should be tracked but aren't launch blockers if documented.

If your vulnerability management solution shows open criticals at T-24 hours, the launch needs to slip. No exceptions.

Ensuring PCI Compliance with Expert Testing Support

Why Specialized PCI Testing Expertise Matters for Card Programs

PCI DSS testing for a card program is not the same as general application security testing. Card workflows have specific data handling requirements, specific integration patterns with card networks and processors, and a specific compliance framework that your QSA is going to audit against.

A team that's done this before knows what QSAs look for, knows where card programs typically fail, and knows how to structure evidence so your certification process isn't a months-long back-and-forth.

Working with Frugal Testing for PCI compliance testing puts your pre-launch efforts directly in line with actual audit requirements not a generic checklist. That’s what drives a smooth certification and prevents costly launch delays.

How Dedicated QA Teams Accelerate Compliance and Reduce Risk

Specialized PCI testing agencies work faster because they've built the test cases, the checklists, and the evidence templates before they walk in the door. They know which vulnerability scanning tools surface the findings QSAs care about. They know how to scope penetration testing to cover PCI DSS requirements 11.3 and 11.4 without running tests that don't contribute to your compliance posture.

They also reduce risk by catching gaps early not at certification time, when fixing them costs weeks and delays launch revenue.

Reducing Time-to-Launch with Audit-Ready Validation

The goal isn't just to pass the audit. The goal is to pass it fast. That means going into your QSA assessment with clean documentation, zero open criticals, re-tested remediations, and evidence packages that don't require your team to spend two weeks digging through logs and screenshots.

Frugal Testing designs its card program security testing services specifically for PCI DSS audit success not generic security coverage. Unlike standard QA vendors, the team aligns every step with QSA expectations from day one, using compliance-mapped test cases, pre-structured evidence collection, and validation workflows built around real audit scenarios.

What sets it apart is the focus on audit readiness, not just issue detection ensuring every finding is traceable, re-tested, and documented in a format QSAs can immediately verify. This reduces back-and-forth during certification and accelerates time-to-launch.

Conclusion

PCI DSS compliance for a card program is achievable before launch but it requires treating it as a first-class engineering and QA concern from the start, not a final-week certification exercise.

The practical steps: map your cardholder data flows early, build compliance test cases alongside functional test cases, run VAPT with proper scope before you submit for certification, fix what you find, and document everything your QSA is going to ask for.

The gaps that kill card program launches are consistently the same ones: logging configurations that drifted, access that was never cleaned up, encryption that was implemented but key management that wasn't, and segmentation that was documented but not tested.

People Also Ask (FAQs)

Q1.Who is responsible for PCI DSS compliance before go-live?

Ans: The merchant or card program manager is responsible for PCI DSS compliance. Usually, the internal security team works together with a Qualified Security Assessor (QSA) to validate everything before launch.

Q2. Do all card programs need a QSA audit before launch?

Ans: Not always. Smaller programs can complete a Self-Assessment Questionnaire (SAQ). However, as the program grows in size or complexity, a full QSA audit becomes necessary.

Q3. How often should PCI DSS testing be done during development?

Ans: PCI DSS testing should be done regularly during development. Security scans should ideally run with every deployment, and penetration testing should be performed at least once every quarter or before any major release.

Q4. What is the difference between PCI DSS compliance and certification?

Ans: Compliance means continuously following PCI DSS requirements. Certification is a formal validation done by a QSA at a specific point in time.

Q5. Can a card program go live with open PCI issues?

Ans: Critical and high-risk issues must be fixed before going live. Medium and low-risk issues can remain open only if they are properly documented, have a clear plan to fix them, and are formally accepted as risks.